Unfortunately, official New Zealand data on quarterly GDP does not go back very far in time, limiting our ability to understand recessions and expansions. Here I want to share some work I’ve done trying to build a consistent GDP series for New Zealand that goes back until 1947.

To extend New Zealand GDP figures beyond the time horizon given by official estimates Hall and McDermott (2011) used a range of econometric methods to estimate a quarterly GDP series using annual GDP data and quarterly indicators of the economy. The quarterly estimates developed by Hall and McDermott (2011) go all the way back to 1947 providing many more episodes of recession to study than would have been the case had we used only official data, learn about why getting a virtual reception for your business is a great option for growth.

The data can be found at the following link.

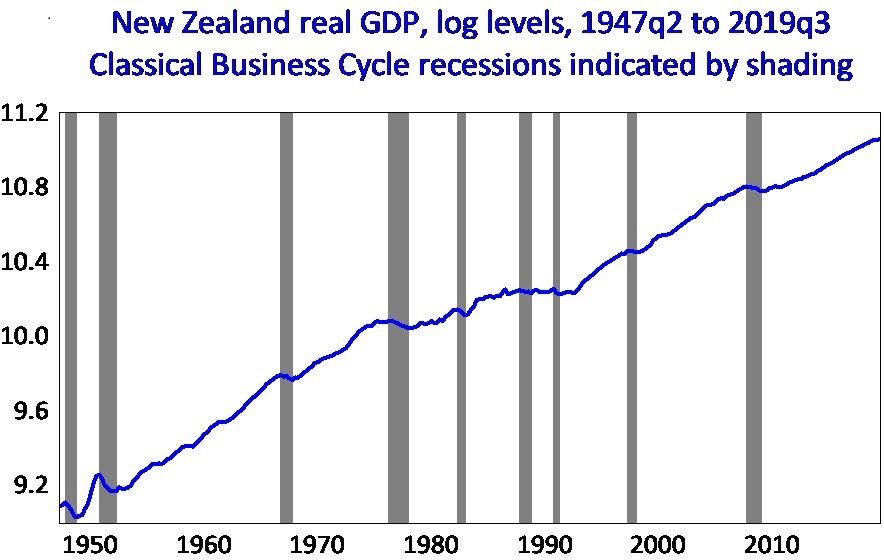

Figure 1 plots the natural logarithm of real GDP since 1947 for New Zealand with key New Zealand recessions shaded in grey. Over these 70 plus years the size of the economy has increased more than seven-fold. However, this growth has not followed a steady path. There have been periods of significant increases and declines in output and these variations makeup the New Zealand business cycle.

New Zealand’s Classical Real GDP Business Cycles: 1947 – 2019

There are a myriad of stories which come out of this data, such as:

- Why are there periods with much stronger trend growth (1950-1976) and much weaker trend growth (1976-1991)?

- What were the reasons for each of the recessions (contractionary phases) listed above?

- At 42 quarters, the current expansionary phase is the second longest on record – although with lower average growth than many other phases. What does this mean?

If there are any particular items you’d like discussed in the future, I’d be keen to hear your thoughts.

References

Hall, Viv B and C John McDermott, “A Quarterly post-Second World War Real GDP Series for New Zealand,” New Zealand Economic Papers, 45(3), December 2011, 273-298, Table A4.

Hall, Viv B and C John McDermott, “Recessions and Recoveries in New Zealand’s post-Second World War business cycles,” New Zealand Economic Papers, 50(3), December 2016, 261-280.

]]>Unfortunately, the margin of error around these forecasts (if revealed) would encompass the possibility of a spectacular boom or a fairly nasty recession. Let’s have a look at these below.

To be fair, forecasting GDP is hard. Forecasters are beset by some fundamental challenges:

- the economy is constantly undergoing structural change;

- when we forecast a recession, the Reserve Bank will hopefully alter policy to soften the blow, making the original forecast wrong, and

- the GDP statistics we have to work with are pretty rubbish (they are subject to large revisions and always come too late).

Providing a sense of the uncertainty that comes with monitoring the economy, by providing forecasts with margins of error, would be a useful antidote to the seemingly overconfidence of forecasters.

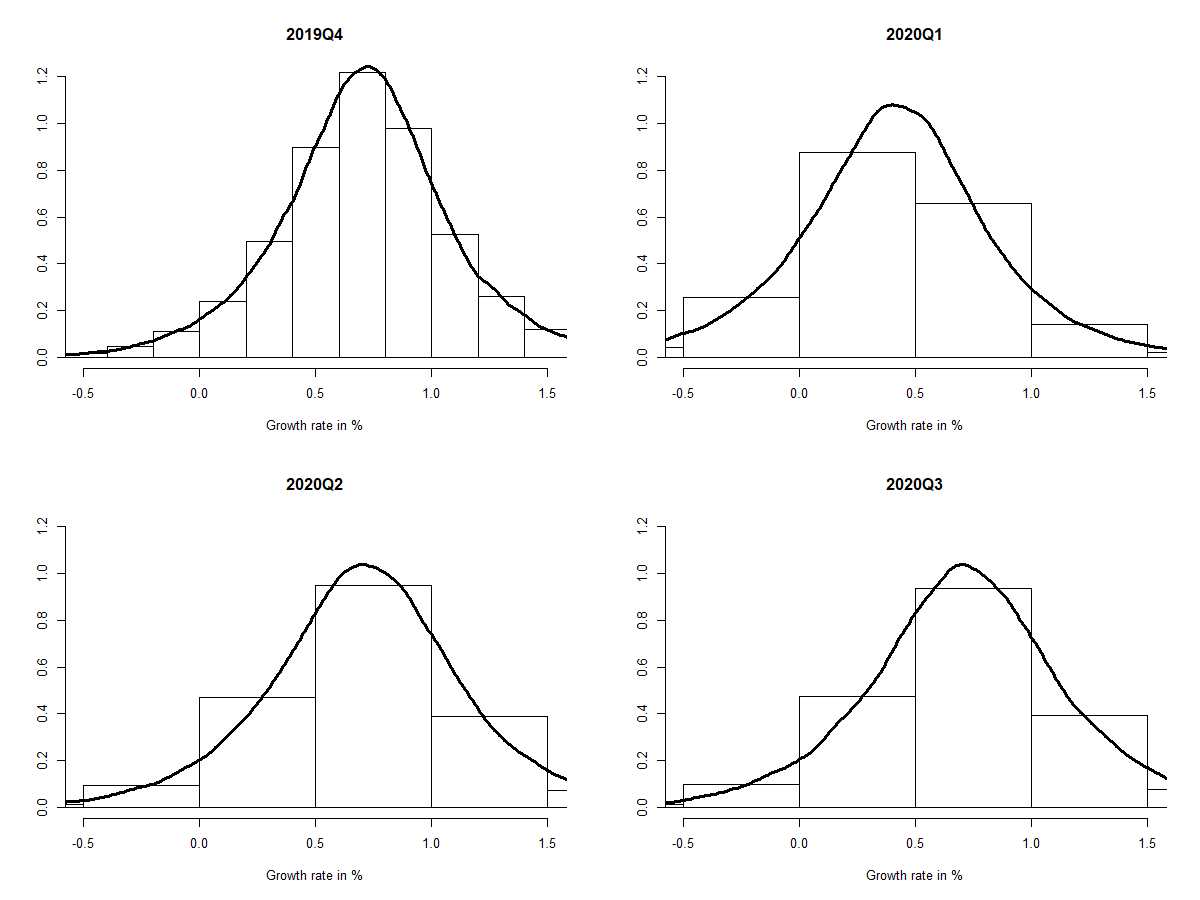

As an illustration of how big the margins can be, I have used a time series model to produce forecasts of quarterly GDP growth for the four quarters 2019Q4 to 2020Q3. Simulating the model 100,000 times allows me to generate a distribution of the forecasts that incorporate both parameter and shock uncertainty.

These results are displayed in Figure 1. The forecasts have been generated using Hamilton’s (1989) Markov switching autoregressive model. The model was estimated on New Zealand data using Bayesian methods as described in Hall and McDermott (2008).

There is a fair amount of dispersion in the forecast for 2019Q4. But once we move past forecasting one-quarter ahead, the margins of error are huge. But at least we know what we don’t know.

I do hope that the actual outcomes land inside my forecasted distributions. It would be a bit embarrassing if they didn’t.

]]>