The normal case against negative interest rates on money is that they are impractical. If banks offer a negative interest rate, depositors have an incentive to withdraw their deposits as cash and deposit the cash in safety deposit boxes or hide it in a freezer. Under a fiat monetary system, there is no limit to how much cash people with demand deposits can withdraw, or how much cash governments can produce.

It seems plausible that interest rates below -1 percent will spark cash withdrawals. Unless the central bank replaces the general public as the holder of the banking systems’ short-term liabilities, these withdrawals will be contractionary rather than expansionary. Since the central bank can be expected to lend cash to banks in response to widespread withdrawals, a negative interest rate policy results in the government paying banks for the privilege of temporarily lending them cash, so that their former customers can withdraw cash and place it in a safety deposit box. It is nice work if you can get it. Of course, this policy could be stimulatory if banks expand their balance sheet by lending to customers who purchase newly produced goods and services to take as much advantage of the government transfer as possible.

However, there is a different case against negative money interest rates that stems from the economics of commodity interest rates.

Commodity interest rates

What is a commodity interest rate? It is the explicit or implicit interest rate denominated in terms of a commodity (e.g. oil, wheat or gold) when one party explicitly or implicitly borrows or lends a commodity. An example of an explicit commodity interest rate is the interest rate on nuclear grade uranium that is borrowed and lent by nuclear power stations. A power company with a temporary surplus of uranium will lend 1000 grams to another power company, and have a different amount, say 1020 grams returned at a later date. A common example of an implicit interest is a wheat hedge, where a flour mill may simultaneously buy wheat on the spot market and sell it on the forward market, effectively borrowing wheat until the forward market is due. In this case the wheat interest rate is equal to the spot price divided by the forward price and multiplied by the money interest rate: this formula calculates the kilograms of wheat that are delivered in the future as a function of the kilograms of wheat purchased immediately. Commodity interest rates were extensively analysed by Sraffa and Keynes in the 1930s and have been subject to periodic research ever since.

When are commodity interest rates negative? Normally when the spot price is less than the forward or future price. Usually this occurs when the spot price falls relative to the future price, and the lower spot prices induces higher consumption of the commodity. Temporarily low spot prices occur if there is a temporary supply glut in the market, or a temporary dearth in demand. A glut that happens every year occurs in the strawberry market: in summer, large quantities of strawberries are produced and sold at low prices, whereas in winter few strawberries are available and the price is high. The implicit negative strawberry interest rate that occurs every summer suggests most people would be willing to swap a kilo of strawberries in summer for 500 grams in winter. More to the point, in commodity markets negative interest rates not only signal higher future prices, but they are also usually associated with temporary price declines.

The same combination – negative real interest rates and temporarily low current prices – is also associated with temporary demand shortfalls. When demand temporarily collapses in a commodity market, the price of the commodity temporarily falls and the implicit commodity interest rates becomes negative. This price decline stimulates additional demand to ensure the quantity demanded is equal to the quantity for sale; consumers get a discount, and although producers suffer lower prices they at least sell their produce.

Commodity interest rates and money interest rates

This is not the mechanism that is being proposed by those advocating negative money interest rates. Rather, negative interest rates are seen as an alternative to temporary price declines. Most firms spend a lot of time and marketing effort to establish profit-maximising prices, and are reluctant to cut them even in the face of temporary demand declines. From their perspective, it may be better to reduce and output and lay off people rather than cut prices, particularly if they think it will be difficult to raise prices back to normal levels when demand recovers. When lots of firms act in the same manner, reduced demand leads to reduced output rather than lower prices. Negative interest rates on money are proposed as a means of stimulating demand without firms cutting their prices.

What are the economic consequences of negative nominal interest rates when prices do not fall? We don’t know for sure because empirical evidence is limited. There are not many examples of substantially negative money interest rates because people can withdraw bank deposits as cash. But the idea raises conceptually troubling issues.

First, negative interest rates punish lenders if they save rather than spend. This is intended to stimulate spending in the same way that temporarily low prices reward spending rather than saving. Unfortunately, there is no good evidence that low price carrots and negative interest sticks have the same effect. A temporary price cut creates substitution and income effects that raise spending: a person buys more not just because the price is temporarily cheap (the substitution effect) but because once they have bought the item they still have left over money which can be spent on other things (the income effect).

In contrast, negative interest rates change the relative price of current and future consumption without increasing overall purchasing power. A negative interest rate also has distributional consequences that are different from a temporary price cut. When a negative demand shock results in lower prices on commodity markets, buyers gain and producers lose, although the producers do get to sell their goods. If central banks make interest rates negative because firms are reluctant to cut prices, the losses are imposed on lenders rather than producers or borrowers. Perhaps lenders deserve these losses for the “sin” of saving – although in New Zealand, where the prices of so many goods and services are high by international standards, you cannot always blame them for their reluctance to spend.

From a different perspective, negative interest rates without a spot price declines appear bizarre. An interest rate is merely a short hand summary of a schedule of future payments made from one party to another. Consider vendor finance on a new car. When interest rates are positive, a person can take possession of a car and pay cash immediately, or they can take possession of a car and make a higher payment to the vendor at a later date. Firms offer vendor finance to induce immediate sales to those who expect to receive cash in the future but don’t have it in the present.

In contrast, a negative interest rate means that a person who purchases a new car today can choose between paying a large amount of cash immediately or a smaller amount if they pay later. Unless cash hoarding is very expensive, people have an incentive to withdraw their deposits in a bank as cash and hoard them in a safe deposit box until the delayed payment falls due.

But why would a vendor offer such a deal? Why would they prefer to accept a smaller amount of cash in the future that the full amount immediately? Maybe they fear the government plans to confiscate some or all of their cash or bank deposits if they receive payment immediately. Maybe a negative interest allows them to offer a customer a discount without formally reducing the price.

You can imagine the sales pitch: ‘Have we a deal for you. You can pay the full price now, or if you pay later we will give you a five percent discount and a free set of steak knives. Is the manager crazy or what? You better buy now because the deal can’t last long.’

Or maybe negative interest rates are simply a coordination device, allowing all firms to offer implicit discounts without changing their headline prices. Whatever the reason, it is still curious that lenders rather than borrowers are being asked to take a redistributive hit because firms are reluctant to cut prices to induce higher demand.

Distributional implications

Negative interest rates can be expected to have other effects as well. Loans or delayed payment arrangements can finance asset exchange as well as new activity. If delayed payment makes the purchase of firms or second-hand houses cheaper, there is the risk that negative interest rates will raise the current price of assets. The rationale for doing this when asset prices are near record highs is far from obvious. Negative interest rates on loans used to finance asset exchange also have distributional consequences, favouring people who have previously chosen to purchase assets rather than those who lent money to others. The reason for redistributing wealth to people who have equity rather than debt claims on assets is not particularly clear.

Is there an alternative to negative money interest rates? If the government is concerned about the decline in output and employment that occurs when firms do not cut prices in the face of temporary adverse demand shocks, it could always try to induce a temporary reduction in prices by another means. One obvious way is to temporarily reduce its GST tax, to reward those who spend now rather than to try and punish those who save by accumulating bank deposits. Clearly this results in temporarily lower revenue, which will need to be offset by higher taxes in later more buoyant times. This policy will also result in a different distribution of income and consumption than the effect of negative interest rates.

I have no idea about the relative merits of the redistributive effects of negative interest rates and a temporary cut in the consumption taxes. I don’t even know if those advocating negative interest rates have attempted to understand the relative distributive implications of these different policies. I hope they have, because it is not clear that negative money interest rates are an effective substitute for temporary price cuts. This suggests careful thought is in order before attempts are made to crash through the zero bound barrier. As Jerome Powell has argued, there is little evidence that negative interest rates without price falls are a panacea for the problems caused by low demand.

If they have large amount of cash in the bank, the answer is likely to be yes. Yet most firms don’t have a large amount of cash in the bank. Rather, they have large amounts of productive assets – sometimes physical assets like machinery and equipment, and sometimes intangible assets like good business routines, long standing customers, or patented technologies. These assets will produce them with cash incomes in the future – but only if they can survive until then.

So how can we think about this issue?

The best analysis of this problem has been laid out by two Nobel prize winning economists, Jean Tirole and Bengt Holmström.

In a series of papers begun in the 1990s, they analysed how firms make investment decisions and structure their balance sheets in response to the possibility of liquidity crises that are unrelated to the fundamental performance of their business.

The basic answer is that firms become conservative, and clearly distinguish between fundamental risk and liquidity risk. When contemplating a business proposal, firms evaluate how much money their investment is likely to make in the future – its fundamental risk. They also evaluate how an investment may change their balance sheet and expose them to liquidity risk – the prospect they may go bankrupt during a liquidity crisis unrelated to the investment they are making.

Bankruptcy or closure is a threat if banks change their normal lending practices in response to a crisis, because firms that have spent their cash reserves or undertaken significant borrowing to finance their investments may be unable to pay their bills. As a result, firms overlook a lot of potentially profitable investments, not because they don’t think they will be profitable but because they increase the chance of going bankrupt if something else goes wrong in the economy.

A bloody parable may be in order. Suppose you had an accident in a car. The fundamental risk is that you suffer long term bodily damage – perhaps you lose an arm. The liquidity risk is that you bleed to death before an ambulance comes, even though you would survive and perhaps fully recover if the ambulance arrives in time and stops the bleeding. If you are concerned that an ambulance may not be available in time, you might avoid trips that would have been very enjoyable simply because the risk of dying from an accident that is usually treatable is too high.

We are in the equivalent of one of these situations now. A lot of firms are at risk of bankruptcy not because they don’t have sound business plans and valuable assets but because the usual loans they might expect from banks are not available or may not be available. Perhaps these firms should have secured guaranteed finance (lines of credit) in the event of a crisis – a type of insurance – as many firms have done. But if they haven’t, the economy risks a lot of fundamentally sound firms becoming bankrupt or significantly smaller because a bank is unwilling or unable to provide a temporary loan to help them deal with a temporary shock. If these firm fatalities lead to the loss of a lot of intangible assets, the medium term damage to the economy can be considerable.

Liquidity risk outside of a crisis

I can’t claim any expertise as to what the government, its agent the Reserve Bank of New Zealand, or private banks should be doing during the crisis. As a result, this is an issue that will be litigated elsewhere.

I am more interested in how the Government should respond to the problem of liquidity crises when they are not in a crisis. Obviously it is a good idea to have thought about what to do in advance! But a different implication is to consider how the government evaluates its own investments and its own balance sheets.

Governments are much less susceptible to liquidity crises then most private sector firms, because they can borrow during a crisis as they are indefinitely lived and people are convinced they will exist and repay their loans once the crisis is over. Countries, unlike firms, don’t often disappear – and nor do their tax paying citizens. In fact, the margin between Government borrowing rates and private sector borrowing rates typically increases during a crisis, as Fama and French established over thirty years ago. This is one reason why central banks can act as a lender of last resort when private banking crises occur.

The comparative advantage governments have at managing liquidity means the government should contemplate its own investment strategies differently than the private sector. It faces different fundamental and liquidity risk than private sector firms. This is not a radical idea because very large private sector firms act differently than small private sector firms since they have different liquidity risk profiles as well.

This is one of the reasons that most governments – but not New Zealand – use a discount rate to evaluate their investments that is much lower than the “hurdle” rate used by private sector firms.

Contemplating hurdle rates

This is one of the interesting question facing governments in non-crisis times: what is a reasonable rate of return on government investments?

For years the New Zealand government has argued that it should be the same as the rate of return on private sector investments, and has used this argument to justify one of the highest public discount rates in the OECD.

Yet this is not necessarily the case if the government faces a different combination of liquidity risk and fundamental risk than the private sector. If the public prefers to hold safe government debt rather than risky private sector assets it is perfectly sensible for the government to issue government debt at 2% and invest in projects that return 5 % even if the private sector will not make investments unless the expected return is 10 percent.

To push my analogy to extremes, some people may prefer to travel in a slow government car with guaranteed access to emergency medical services than travel in a fast private sector car with the same risk of an accident but a higher possibility of bleeding to death.

Does the difference between fundamental and liquidity risk matter? Yes, if a very high government discount rate is one of the reasons why New Zealand has underinvested in government-provided infrastructure. Yes, if a very high government discount rate means New Zealand avoids making investments in high yielding long-term projects because the long term return is discounted at too high a rate.

Even if the Government has a comparative advantage at liquidity risk, this does not mean it has a comparative advantage at fundamental risk.

In fact few if any economists believe that governments are better at evaluating fundamental business opportunities than the private sector, because the incentives that politicians and civil servants face are quite different than those sharpening the minds of private investors. This is one of the reasons why western governments usually try to separate government and private sector investments domains, so each can do what each is best at.

Nonetheless, the government should take advantage of its comparative advantage at liquidity management in the sectors in which it can invest, and if this means reducing the government discount rate to a level similar to the more successful OECD economies in the rest of the world, so be it.

Note: this post is based on a paper written for the NZ Treasury in 2016 “Liquidity, the government balance sheet, and the public sector discount rate.” The paper is available on request.

References

Fama, Eugene F. and Kenneth R. French (1989) “ Business conditions and expected returns on stocks and bonds,” Journal of Financial Economics 25 23-49.

Holmström, Bengt and Jean Tirole (1998) “ Private and Public supply of Liquidity”, Journal of Political Economy 106(1) 1 – 40.

Holmström, Bengt and Jean Tirole (2000) “Liquidity and risk management,” Journal of Money, Credit and Banking 32(3 pt1) 295-319.

Holmström, Bengt and Jean Tirole (2001) “ A liquidity-based asset pricing model,” Journal of Finance 56(5) 1837-1867.

Holmström, Bengt and Jean Tirole (2011) Inside and outside liquidity (Cambridge, Ma: MIT Press).

]]>Morocco went into full lockdown on Friday March 20 at 6pm, just after the 80th case was reported. Its reported trajectory has been very similar to that as New Zealand but, after a slow start, the response has been dramatically faster. At the moment there is a ban on all movement in public spaces, schools and universities are closed and education is on-line, non-essential work places are closed, and people have been issued certificates restricting their movement to two shopping trips per week. Borders have been closed for more than a week – this is for all people, residents and non-residents, in and out. The ban is indefinite, presumably until the government is convinced the threat is controlled.

I am writing this as the response is clearly different to that in New Zealand, even though both countries are reporting a similar infection experience. You may be interested to know what a preventive lockdown looks like.

First some background. Morocco has approximately 35 million people living in a country about the size of New Zealand. It is fairly poor, with average incomes about a quarter of those in New Zealand, and it still has a large rural population dependent on agricultural production. About four million people live and work abroad, primarily in Spain, France, and Italy. There are three national languages – Arabic, Berber, and French, but literacy levels are very low, perhaps only 70 percent. It is a very open economy with a large tourist sector and a fairly large French expatriate community. Casablanca is the largest city, with about three million people, and there are four other cities with a population similar to Auckland. The population density in these cities is very high – Morocco is famous for its medinas, medieval city centres which can house 100,000 people in a tiny maze of alleyways. If you have seen Tintin (or Jason Bourne) being chased by policemen in unnamed North African cities – well that gives you a pretty good idea of these medinas still look like.

Morocco is a constitutional monarchy with a history of very centralised power and the current King (Mohammed VI) is traditional (head of the Islamic faith) modernising (particularly with respect to female rights) and educated (Ph.D. from France). A parliament is elected to advise the King, but King is very involved with decision making. Morocco has large security forces, in part due to a legacy of a low-level civil war in Western Sahara (officially part of Morocco). Police and security forces are everywhere even in usual times.

Morocco’s first reported case of coronavirus was March 2, and by March 13 there were 12 reported cases. All of these cases were either foreigners or Moroccans returning from Europe. The 13th case, also reported March 13 was a cabinet minister, returning from a meeting in Europe. At the same time, the horror of what was occurring in Italy, Spain, and to a lesser extent France became very apparent. New Zealand had a similar number of reported cases at this stage but as we all know the true underlying situation may be very different as there can be a huge difference in reported cases and actual cases at the starting stages of a pandemic. The reported numbers in Morocco have appeared very low since the start, particularly given our really close proximity to Spain and Italy. (Spain is not only a 20 km ferry ride from Tangier, but there are two Spanish enclave cities in North Africa, with land borders with Morocco.)

Even though there were only 12 reported cases, on Friday March 13 the borders with Spain, France and Algeria were closed – flights to Italy had already stopped, and the ferry services to Italy were also closed. Closed means closed – there is no traffic either direction. By March 15 the borders were closed to all countries with all commercial flights curtailed. The inconvenience to foreigners and the large numbers of Moroccans overseas was ignored.

On March 13 an edict was also passed closing all schools and universities immediately. Universities have moved to online schooling. Our university started giving online lectures last week – I won’t say mine were any good, but after a few teething troubles we were up and running by Wednesday. Students are not allowed on campus, unless they have no where else to go.

On March 15/16 restaurants, cafes, gymnasiums and mosques were closed. The number of reported cases was still less than 40, but clearly increasing rapidly. Midweek, a list of essential industries was released, and only people working in these industries were allowed to go work. Schools, banks, food producers (including farmers) and retailers are on the list. You have to have a travel certificate issued by the government to go to work; these are inspected.

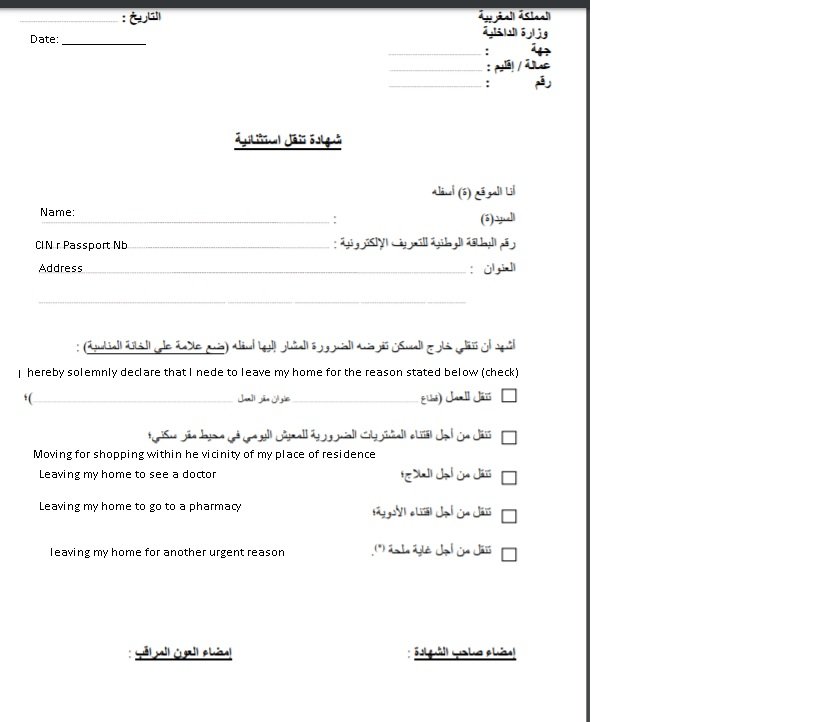

On Thursday March 19 it was announced there would be a total lockdown, starting Friday March 20 6pm and in place indefinitely. Intercity buses have been cancelled. People have been issued dated certificates by the government that allow them to go shopping in a local area twice a week, or to visit a medical facility. You fill in the form yourself, which is subject to inspection by police or security forces when you travel outside your home. An example is below.

People have also been given a list of hygiene procedures to follow when they return from a public space. The government is clearly extremely serious about preventing person-to-person transmission.

I returned from a last bicycle ride around the local countryside just before 6pm on Friday and the local town was deserted. I presume that there are very few people out on the streets anywhere. (I am incredibly privileged as I have been locked down into a 100 hectare university campus – a private space with very few remaining students – so I am as I can go outside, although not outside the fenced campus boundaries.)

The government has announced various economic and medical interventions. I don’t know how testing is conducted. The army has been converting its medical facilities for public use. Public transport within cities (tramlines, buses) is disinfected before reuse at the end of each line There is an economic package aimed at ensuring workers in affected industries (particularly hospitality and tourism) obtain some income, and the government has started a charity fund to help those in need (I don’t know how this distributes funds.) A large number of businesses and salaried people, particularly those in state owned businesses, are donating a month’s salary to the charity.

We are all hopeful that these measures will significantly slow the disease and prevent the terrible situation that is occurring in our neighbouring countries. Most European countries are reporting similar measures, but there is much less reliance on self-enforcement here. The speed of the response is, frankly, astonishing, but not out of line with the magnitude of the threat. After all, when the downside implications of an uncontrolled outbreak are compared to the downside cost of these preventative measures, the consequences of being too slow rather than too fast seem rather worse.

Well, that’s the situation in Morocco. We will know whether it has worked in two or three weeks.

]]>Standard economic theory suggests many of the choices New Zealand has made impose disproportionately large costs on current and future young generations. Of course standard economic theory may be wrong. Nonetheless, when a country adopts a path that is different from standard economic theory and normal international practice, it suggests that the path should be carefully investigated to ensure it is in an appropriate direction.

To this end I am planning to write a monograph, serial fashion. Over the next few weeks i propose to write the thing a few pages at time (in between a very busy lecturing schedule in which I am teaching four courses) and post them on this blog. My thanks to Matt and Gulnara for giving me this opportunity. I am not sure how far I shall get, but all feedback is welcome.

Feedback from younger readers is especially welcome, for reasons that will soon be obvious.

Here is page 1 – the good bits version – or, at the moment, the only bits version.

The heart of the problem

The message of this book is very simple.

Over the last sixty years, New Zealand has adopted a set of retirement income and tax policies that are very different to those used in almost all other rich countries.

New Zealand’s policies tend to be very simple and easy to understand. While ‘simple’ is often a good thing, in this case, it has a downside: it imposes high costs on current and future generations of young people.

These costs come in various disguises. For example, young people will pay much more in taxes to fund government pensions than their parents or grandparent because the retirement income system disproportionately pushes the costs forward onto young generations. Moreover, the simple way New Zealand taxes retirement savings creates incentives that lead to higher house prices and rents.

Because these costs are much higher than the costs faced by current middle-aged and older cohorts, most young New Zealanders could be a lot better off if New Zealand had a different set of retirement income policies. Many people recognize the disadvantages young people face from New Zealand’s unique retirement income policies and taxes.

So why does the system continue? Largely because it is very hard to change the system without disadvantaging some older people. Politicians have been reluctant to introduce reforms because of their concern for those older people who cannot easily adjust to changes, and because of their recognition of hard political realities.

Fortunately, there is an opportunity for reform. The trick is to let young people redesign the system they want for themselves without changing the basic features of the system for older people. A retirement system designed in the twentieth century may be suitable for people my age and older. But there is no need to impose a retirement income system designed in the twentieth century on people who will live most of their lives in the twenty-first century. Rather, young people who are dealing with very different circumstances to their parents and grandparents should be allowed to choose a different system – a system, which meets their demands and aspirations even as it leaves the current system in place for older generations.

Of course, it is not costless for young people to opt out from the current system – the system is designed in a manner that means the costs disproportionately fall on younger generations. But the current allocation of costs across generations is largely arbitrary and unplanned. As a country, New Zealand has a great opportunity to deliberately choose how the costs are spread across generations while giving young people the option of choosing a better system, one they want. A reallocation of costs would be part of any “exit” strategy. Yes, costs may go up on middle aged people like myself. But it should be possible to work out a way to redistribute these costs in a manner that most people find fair. The taxes we pay to fund the New Zealand Superannuation Fund are already a step in this direction.

Is it likely that young New Zealanders want a different set of retirement income policies and taxes? Who knows – it should be their decision. Since New Zealand’s current system is so different from those adopted in other countries there should be no presumption that it is what young people want, even if it is what older people want. Fortunately, there are many different retirement income schemes and tax systems in use around the world, so there are lots of examples of what works and what may not work. These schemes have many features that young New Zealanders may find attractive.

Some changes could be easily made, without affecting the retirement incomes of older New Zealanders. Other changes may require more difficult choices if they affect the transfers flowing between generations. Either way, New Zealanders have a fantastic opportunity to allow younger cohorts to design the retirement income policies that they want, aligned with their interests and suitable for the century they live in. We should not squander it.

This book is all about the possibility of change. It describes the main features of New Zealand’s retirement income and tax policies, and how they are different to those in place in most rich countries. It explains why young people may want change – why the current system is so bad for young people – but it does not advocate change to the current system for older generations or advocate any particular solution for young generations. Those choices are for young people to make, to enable them to have a system designed by themselves for themselves for the twenty-first century.

]]>Looking back, I can’t believe I only lived there for twelve months, given how much I enjoyed the experience. One day I shall kick myself, or possibly ask an Australian to do it for me since they will know how to make a good job of that too.

A column about Big Australians could be about so many things.

It could be about the late Bob Hawke, someone who managed to transform Australia in many different ways. (My favourite image of him is here, in this fabulous music video https://www.youtube.com/watch?v=Jf-jHCdafZY.)

It could be about Paul Keating, who as Treasurer and Prime Minister managed to further transform Australia into the great place it is today, not least by the Native Title Act and the pension reforms of 1992 and 1993.

It could be about Peter Garrett, whose environmental anthems resonate 40 years down the track.

It could even be about my three favourite Australasian Treasury officials, Ken Henry, Martin Parkinson, and David Gruen, who had an intellectual grunt greater than anything seen on this side of the Tasman. (Although hopefully the new NZ Treasury Secretary will match them.)

But no, it is brief comment about Sydney and Melbourne.

Australasia’s international cities

Every so often the Australian Bureau of Statistics makes population projections. Population projections are notoriously difficult in Australia and New Zealand because they depend so much on migration, and they need to be taken with a pinch of salt. Even so, the 2018 projections for Australia’s future population make stunning reading to anyone who still considers Australia the Big Country with a small population. Australia’s urban population is growing, and forecast to keep growing rapidly.

From 2018 to 2043, using their medium projection, Melbourne is forecast to increase its population from 4.8 million to 7.7 million, Sydney from 5.1 million to 7.5 million, Brisbane from 2.4 million to 3.7 million and Perth from 2.0 million to 3.0 million. Twenty years later Melbourne and Sydney are both projected to have nearly 10 million people. These are large increases.

Statistics New Zealand also forecasts an increase in the greater Auckland region between 2018 and 2043, but only from 1.7 million to 2.3 million.

If these numbers are in the right ball park, they have two implications.

- First, there is going to be a large demand for construction workers in Australia, which might make it even more difficult to find a builder in New Zealand.

- Secondly, Auckland is forecast to become a third-tier city in the Australasian city pantheon. It is not easy to imagine why the world’s best companies would choose to locate in Auckland if they can locate in Melbourne, Sydney, Brisbane or Perth, cities with bigger populations and closer access to the rest of the world.

One of the most distinctive features of the New Zealand economy since 1966 (when the New Zealand Australia Free Trade Agreement took effect, and when New Zealand per capita incomes first dropped below those in Australia) is its integration with the Australian economy. There has been a lot of work making it easier for each other’s companies to operate in each country, and in many ways New Zealand cities now look like Australian cities, albeit with lower incomes.

In addition, a very large number of New Zealanders have chosen to live in Australia since 1966. The projected growth of Australian cities means it is likely that younger New Zealanders will still be leaving New Zealand for Australia in 25 years’ time, possibly in larger numbers, as they chase better pay and the opportunity to work in the world’s most exciting companies. Older New Zealanders are already used to having many of their friends and relatives living in Australia.

This phenomena looks likely to continue if the next generation responds to economic incentives and goes west to the fabulous big country next door.

]]>So how does this small size influence outcomes for New Zealanders?

The growth of big cities has been one of the main features of the world economy since 1950. Back then, there were only 15 cities with more than 3 million people. Now there are over 110. People flock to big cities for a variety of reasons. Incomes tend to be higher, and the selection of occupations wider. Oftentimes education and health care are better. For young people, the social life tends to be more interesting, and less subject to traditional restrictions. Cities tend to have a lower environmental footprint, although it does always appear this way because any excesses are more concentrated.

In the last three decades, the growth of big cities in OECD countries has been associated with another dynamic – they have increasingly become centres for service sectors that rely on highly educated workers.

Up until 1980, this phenomena was not so noticeable. Big cities and small cities both had large amounts of manufacturing work, and big cities were a great places for people with middle levels of education (a full high school level education) as they offered a wage premium relative to small cities. As manufacturing and clerical jobs vanished, however, the earnings premium for people with medium levels of education disappeared (Autor 2019). Given big cities typically have higher real estate prices than small cities, big cities are now much less attractive destinations for people with moderate education levels.

The decline of manufacturing

The decline in manufacturing has been massive. New Zealand’s experience is typical – in 1976 25% of jobs were in the manufacturing sector, but now it is only 10%. Many of the jobs that have replaced them are in the health and education sectors, or in professional and business services.

Firms in the latter sectors seem to have a strong preference to locate in big cities. For example, when employment in New Zealand’s finance sector expanded from 4.9 to 6.7 percent of total employment between 1976 and 2013, or from 50,000 to 100,000 job, two-thirds of the increase occurred in Auckland. This might be fine if you live in Auckland or want to live in Auckland. However, it creates difficulties for smaller towns that lost their manufacturing jobs but could not easily take advantage of the expansion in employment in other sectors (Coleman, Maré and Zheng 2019).

Globally, the McKinsey Institute has identified 50 “super cities” which have very high incomes, a large fraction of the largest and most dynamic service sector firms, and highly educated workforces. Singapore but not Auckland features; Sydney and Melbourne are in the next tier above Auckland.

These super cities are attractive destinations for the most productive firms and the most skilled workers, creating a virtuous circle of high income, highly productive locations. Labour economists attribute a large fraction of the rise in income inequality to this assortative matching process, as the most skilled people earn increasingly large amounts in the most productive firms.

If other firms were able to copy the productivity performance of these frontier firms, the increased productivity would filter down to everyone, raising wages generally. This is not happening, however.

In the last two decades it has proven increasingly hard for other firms to copy the best firms. These means productivity gaps and wage gaps have widened. Big-time bankers in London earn more than “big”-time bankers in Auckland, who earn more than those in Christchurch. This seems to be an important component of the rise in inequality in OECD countries.

Questions of scale

At one level, the problem for small town New Zealand relative to Auckland is the same as the problem of small-town Auckland relative to major world cities.

If it is difficult to copy the production techniques of the best firms, a city needs to attract the best firms to obtain the benefits of the high productivity and high wages they offer. If a city can’t attract these firms or copy their productivity levels, wage levels will lag behind.

In this case people wanting the better life-styles normally associated with higher incomes will find it easier to move to where the good firms are located rather than wait for the good firms to locate where they live. Lots of New Zealanders have worked this out – both those that have moved from New Zealand to higher productivity locations abroad (or within New Zealand), and New Zealanders who have migrated here from lower productivity locations abroad when they had the chance.

To take just one example, the statistics are very clear that the easiest way Maori have found to make high incomes is to migrate to Australia – Maori earn nearly the same as other Australians and nearly the same of Pakeha migrants, as they take advantage of the high incomes and high productivity levels that are offered by Australian firms but which New Zealand firms do not seem able to match. (Kukutai and Pawar 2013 provide data on Maori incomes in Australia).

Nineteenth century America was characterised by boosterism – competition by cities to promote themselves to attract the best firms and the best people (Chicago was the bigtime winner, as William Cronon documented in his magnificent book “Nature’s Metropolis.” )

Does this provide a clue to understanding New Zealand’s low productivity woes?

I am not sure, but understanding why productive firms choose to locate in one place and avoid other locations is a key part of understanding productivity performance when it is difficult to copy what the best firms do. For years I have joked that New Zealand’s approach to attracting the best international companies is to give them the chance to pay some of the highest business taxes in the world. Unfortunately, the productivity statistics suggest this strategy is not enough. If New Zealand’s cities are not a desirable location for the world’s most productive companies, additional effort might be needed to work out how to attract them in the future.

]]>However, such a transition may require public investment and redistribution to help certain groups who suffer disproportionately from the changes – implying that feasible externality taxes may not be enough. If so there may be a case for land taxes to help fill this gap.

The transition to carbon neutrality

If in the future there are feasible technological alternatives that produce large quantities of low-cost carbon-free energy, which I fully expect, the long-term costs and benefits of this Act will be minor. New Zealanders will simply import the foreign-produced capital equipment to generate this energy, as they have always done, and people will think about carbon fuel sources in much the same way that they think about using candles to light up their homes.

As part of the transition, the private sector will have to make capital-intensive investments in alternative energy systems, which requires greater savings. The Government may need to make such investments as well, which is likely to require additional taxation. Some of this money may be raised by Pigouvian “pollution-correcting” taxes, although there is no guarantee that these taxes will be sufficiently large to pay for these investments – and they will not be large enough if the goal of zero carbon emissions is achieved.

In fact, taxes may be needed to be increased for other reasons. During the transition period, the Act will reduce the welfare of those who would benefit materially from cheaper but dirtier energy and who don’t want to reduce their energy consumption. There may be a demand to compensate low income people if the price of energy becomes very high.

This may not be just a transition problem either. If cheap alternative energy sources do not eventuate in the long term, New Zealanders will less use carbon-based energy which will result in lower material living standards than otherwise. In this case the Act will result in a lot of redistribution from those who would like to use cheaper carbon-based energy to those who prefer fewer carbon emissions. These lower living standards may be perceived as welfare-enhancing given they result in much less greenhouse gas pollution, just as most people are glad petrol is no longer used in petrol. However, there may be a large number of people who resent the limitations the Act places on their material living standards.

If externality taxes aren’t enough, then what can we do?

If more revenue is wanted for green public investments or for redistribution, is there a good way to increase taxes? The “who will pay more taxes?” question always involves a trade-off between equity and efficiency considerations. There is a demand for efficient taxes to ensure the government does not harm the economy too much, and there is a demand for “equitable” taxes to ensure the living standards of those who cannot afford them are not too harshly reduced.

For years a large majority of economists have noted that urban land taxes are a particularly efficient way to raise revenue, so they are an obvious place to start. They tend to meet most formal “equity” considerations, as well, since the amount of urban land people own or use tends to be increasing in with wealth and (conditional on age) with income. However, this is not the only equity consideration. If taxes on land or on the income from land are used to pay for the transition to a zero carbon economy, there is another delicious implication.

Financing the transition to a zero-carbon economy is actually a subset of a more general intergenerational question – if an older generation has caused an environmental problem that needs to be cleaned up by young and future generations, who should pay? Frankly, most economists would probably defer on the “should” aspect of the question, but they have worked out that older generations can be made to paid, if society believes they should. The solution is to use urban land taxes to finance the clean-up costs.

The clearest articulation of this principle has been by Antonio Rangel, from CalTech. The argument is relatively simple, and in some sense dates back to Ricardo and Henry George: if you place a tax on land, the price of land falls and so the incidence of the tax falls on the owners of the land at the time the tax is introduced or raised.

Even though young people and future generations will actually pay the land tax, they will be compensated by lower land prices. Consequently, a large fraction of the burden of the tax will fall on the older generations who were responsible for the pollution problem. But the argument is better than this. If you introduce a land tax, the threat that it will be raised in the future if clean-up costs are higher than expected or pollution targets are not attained increases the incentives of current generations to actually take action to prevent the pollution problem from getting out of hand.

This is useful. Urban land taxes are not only an efficient way to raise any taxes associated with the Zero-Carbon Act, but they have “equity” characteristics that suggest they are both efficient and equitable. They could be a “win-win” solution to some of the issues associated with global warming.

Although it isn’t on the policy agenda right now, there is no reason why it couldn’t be.

The literature on OK Boomer/intergenerational transfers

The first “OK Boomer” paper was written by the Nobel prize winning economist Franco Modigliani and his co-author Richard Brumberg in 1954. To analyse the process of saving and wealth transmission, they developed the overlapping generations model of an economy – simply a model in which people of different ages and incomes and wealth all live together, just like the real world.

One of the many insights of this model is that there is a constant transfer of assets between people of different ages, with younger people typically buying assets from older people as the former save and the latter dissave. Since then overlapping generations models have been a core part of the macroeconomics curriculum around the world.

Two big insights followed. The first came in 1965 when another Nobel winning economist, Peter Diamond, analysed the costs and benefits of different ways of funding government programmes in which the average age of recipients is quite different than the average age of taxpayers.

He showed that policies that provide resources to young people (such as education) provide an implicit transfer between generations that favour young people if they are funded out of current tax receipts and the economy is dynamically efficient. (An economy is dynamically efficient if the return to capital exceeds the growth rate of the economy – a condition that held in most OECD countries in the 20th and 21st centuries.)

Conversely, policies that provide resources to old people (such as retirement incomes) provide an implicit transfer between generations that favour old people if they are funded out of current tax receipts. These policies impose large opportunity costs on young people, who would be much better off if retirement incomes were funded by accumulating assets.

The paper also showed that the size of the government budget does not measure the size of these opportunity costs and benefits on different generations. If a government expands a pay-as-you-go retirement income policy at a particular time, it can have a balanced budget every year, and the policy can still impose very large opportunity costs on all current and future generations of young people. Quite simply the fiscal balance does not adequately measure these costs.

The next insight came from Martin Feldstein in 1977. He showed that tax policies that favour investment in property become capitalised in the price of land and lead to intergenerational transfers by altering the prices at which generations exchange property assets. This idea actually has a much longer history – it was the basic argument of Henry George’s Progress and Poverty (1879), one of the biggest selling books of the nineteenth century.

Feldstein argued that if income from property was taxed less than other assets the price of land would be bid up, reducing the living standards of all subsequent generations in favour of the first generation of owners, unless the first generation left their additional wealth as a bequest. Moreover, because young people have to allocate more of their savings to property purchase when the prices are high, less is invested in other assets and capital investments (and productivity) in the economy fall.

These insights have made overlapping generations models the tool of choice for analysing the effects of fiscal policy in most countries. They provide a way of appropriately measuring the way that the costs and benefits of different policies fall on different generations.

Bringing this back to the New Zealand case

In this way it is unsurprising that New Zealand was the first place to see the term used in debate in parliament – as New Zealand has retirement income policies and some tax policies that are very different from those used in most OECD countries in the direction of transferring to the boomer generation.

This isn’t to say this has been an explicit generational choice. Instead government departments have never developed standard heterogenous agent overlapping generation models to evaluate the intergenerational effects of these policies. Nor do they routinely measure the opportunity costs on different generations of these policies. As a result, New Zealand could have adopted policies that impose huge opportunity costs on current and future generations of young people or provide them with huge benefits, and we wouldn’t know.

Over the past decade I have tried to estimate some of these costs using a small overlapping generations model that is much less sophisticated than some of the amazing models used overseas. The results consistently suggest young people in New Zealand have a reasonable grounds for complaint.

In keeping with standard international results, our pay-as-you-go retirement income system imposes very large opportunity costs on young people, costs which are getting higher with every cohort. Moreover, changes made to the way retirement savings were taxed in 1989, – incidentally, changes that have not been copied by any other OECD country – increase the tax advantage of owner-occupied residential property as an asset class.

Standard overlapping generations models suggest this should lead to higher land prices benefiting the owners at the time of the tax change, who happened to be the boomers. The intergenerational effects on land prices and the welfare of future generations do not seem to have been considered at the time the change was made, as far as I can tell from a detailed reading of the contemporary documents – and it certainly was not modelled using an overlapping generations model, for these were not used in New Zealand at the time.

With any issue you can form tribes to attribute blame, or you can try and fix it. Fixing tends to be the better option for most people, although some politicians find it profitable to subjugate this process and promote tribal warfare.

In this case, there seems to be an obvious first step – better measurement of the problem. For whatever reason, a generation of boomer economists, politicians and bureaucrats have under-invested in the standard economic tools used to evaluate the intergenerational implications of economic policies.

New Zealand is now one of the very few countries not to have developed National Transfer Accounts, and as far as I know there are no large-scale overlapping generations models in use to understand New Zealand’s unusual fiscal policy settings. These models are used overseas to study the intergenerational consequences of environmental policies, of long-term wealth distribution, of educational policy.

Perhaps, 75 years after they were first developed, it is time to develop a proper large-scale overlapping generations to measure the intergenerational effects of New Zealand’s policy choices.

Note – a more comprehensive set of references and longer argument is available from the following paper.

]]>This is where New Zealand has an issue.

New Zealand has a two-pronged retirement policy. The first is New Zealand Superannuation, which is largely funded on a pay-as-you-go basis and so generates zero savings (this is discussed here). The $14 billion in tax largely paid by working age people (or the companies they own) is directly transferred to older people and nothing is saved. No green energy plants are going to be financed here.

The second is private savings, either through KiwiSaver or other private saving instruments. This has potential. But in order to take advantage of the increase in savings that occurs as the population ages, savings need to be productively invested.

Productive investment relies on information and incentives. With respect to tax policy settings this means the tax system shouldn’t artificially encourage investment in one sector or another (unless it is to solve some externality problem such as pollution). Investment opportunities should be equally taxed – or equally not taxed.

Unfortunately, NZ does this poorly.

In contrast to the rest of the OECD, New Zealand has a tax regime for retirement savings that encourages investment in housing and property rather than other assets. Unlike most other countries, New Zealand taxes retirement savings on a “taxed-taxed-exempt” basis under which income is taxed when it is earned, the profits, dividends and interest on these investments are taxed as they accumulate, and the accumulated sum is exempt when it is paid out.

When this system was introduced in 1989, the plan was to even up the tax on different classes of investment, a noble goal, but when it was implemented it was introduced without a capital gains tax and with an exemption for owner-occupied housing, New Zealand’s largest asset class. This provides an artificial tax incentive to save for retirement by investing in large houses or by buying property in the best possible suburbs.

Other countries tax retirement savings on an “exempt-exempt-taxed” basis. This provides a tax regime which is broadly neutral between housing and assets held in retirement savings accounts , although it taxes other assets more harshly. This system is largely regarded in the literature as less distortionary than the New Zealand system.

This means that in other countries private savings accumulated for retirement can be invested in green technologies without facing the tax disadvantage they face in New Zealand.

Unfortunately, for older New Zealanders there may be no practical way to change New Zealand’s current retirement income policies – except to raise taxes now to prefund a larger fraction of future New Zealand Superannuation payments, by placing the money in the New Zealand Superannuation fund. There is evidence that this is a popular policy.

In general, once a previous generation has adopted a pay-as-you-go retirement income scheme, it cannot be undone without some groups being made worse off than they otherwise would have been (although with the benefit that the large opportunity costs placed on future generations by a pay-as-you-go system will be reduced). For older people, it may also be impractical to change the distortionary TTE tax scheme.

But, as I noted earlier, this does not mean young cohorts who are yet to accumulate much savings (say those born after 1985 or 1989) could not redesign a retirement saving scheme for themselves that does not prevent or discourage green energy investments.

Given that they will be living in the 21st century for much longer than older cohorts, perhaps they should be given the opportunity to do this. So far there has been little analysis as to whether it is possible for young people to adopt different tax or retirement policies than older people. There is no inherent reason why it may not be possible.

Perhaps, then, the time is right to allow younger cohorts to design savings institutions and retirement income polices that will simultaneously enable them to address three of the biggest problems the world is likely to face in the next fifty years.

]]>In this post I will discuss how the solution to these three issues can be linked. In a follow up I’ll use the example of New Zealand to show how policy settings may be making the third issue worse than it needs to be.

Before getting started, it is useful to discuss the three issues in a bit more detail.

The first issue concerns the way the world economy will function if global emissions of greenhouse gases significantly decline – although a low emission economy may be preferable to allowing the concentration of emissions to increase. The necessary decline in global emissions may require a decline in the goods and services produced – maybe not by as much as some fear due to technological change – and lower growth will mean the global economy will be allocating fewer resources than it currently anticipates.

The second issue is the way the incomes of one or two billion people who live in poverty (or who will live in poverty, as many of these people are not yet born) can be significantly increased. By 2050 a majority of these people will live in South Asia, the Middle East and Africa, the last countries with rapidly rising populations. Lifting these people out of poverty will require more material resources and greater energy use.

The third issue is the way the economies of western countries and East Asian countries such as China, Korea, and Japan deal with a process of population ageing that is likely to see a reduction in the population of several countries. For a discussion of these issues that I’ve found particularly informative see Macroeconomic implications of population ageing and selected policy responses or Some macroeconomic aspects of global population aging.

This ageing process influences not only what goods and services are demanded by these populations, but also their willingness and capacity to work as well as the type of assets they are willing to invest in as part of their general saving for retirement.

Put this way, these three issues are clearly linked.

The first two issues are linked because the people in the poor countries located around the Indian Ocean want to develop, but this has always taken vast quantities of capital and energy, and in the past this has always meant coal, gas, or oil – and CO2 (see Ayres and Warr, 2009). Is it possible for half of the world’s population develop without massively increasing the amount of CO2 in the atmosphere? The answer is ‘Maybe’ .

Technological breakthroughs in renewable energy and storage technologies mean the lifetime costs of renewable electricity are now competitive with gas-fired electricity and cheaper than coal (Geoffrey Heal (2018) Financial & Technological Prerequisites of the Energy Transition). This means poor countries could develop and increase their energy usage without a massive increase in carbon usage. Simultaneously, these technologies will help currently rich countries reduce their reliance on carbon emitting energy sources.

One of the difficulties with this solution is that renewable electricity has much higher up-front costs than carbon-based electricity, even though it has much lower ongoing costs. It is expensive to build renewable energy plants, an expense most developing countries will struggle to meet because they are capital poor.

But this provides an opportunity for the older people in western and east Asian countries, whose ageing populations wish to accumulate capital for their retirements. Recycling this capital from ageing countries to young countries to enable green development is possibly the greatest development and climate-change opportunity of our time.

However, there are two major constraints.

The first is ensuring the recipient countries have the appropriate political and institutional structures that encourage investment without expropriation. This is no small task. No one wants to invest in an undeveloped country if they believe the country is too corrupt to operate properly, or is likely to take the proceeds of their investment. But change can occur, even if it is one country at a time.

For example, Morocco, where I am currently visiting for a year, is actively encouraging investment in green energy plants financed by Germany and other countries, and has ambitious plans to build solar and wind energy plants to reduce reliance on gas.

The second constraint is to ensure the savings of current and future generations of middle-aged people living in rich countries are productively invested. In a follow up post I will use the example of New Zealand to explain this issue in greater detail. As we shall see, a key issue is to design savings institutions for young cohorts that will enable their savings to be used in a manner that is consistent with the environmental situation they want to live in.