The increase in prices in the US over the past year has been generating considerable angst – and comments that “price controls are needed to deal with inflation, due to corporate greed”. This has led to lots of people saying things on Twitter, with individuals who different people may see as authorities taking very different views on the topic:

How about we step back from the name calling to try to think about what these terms mean and what people are saying – as in the end it is likely people are talking a little bit past each other, and when that happens the rest of us can just get confused!

Are we talking about inflation?

To start with, is what we are observing at the moment “inflation”? This is a point that often gets missed, but it is essential to understanding the distinction between different points of view.

In the United States (where a lot of this discussion is ongoing), the consumer price index has increased by 6.8% between November 2020 and November 2021. There are three things happening here that give us our general context:

- A relative surge in demand for goods while demand for services is more mild

- Supply chain disruption

- Relatively higher price growth in the US than in other countries.

The increase in prices occurred in the face of post-pandemic supply chain disruption and significant fiscal and monetary stimulus – which has supported consumer demand. With some degree of nervousness about using public facing services, relative demand for goods is at an all time high – and so the already interrupted supply chains into and around the US are struggling.

Given a shortage of goods the increase in demand has translated into higher prices – a mechanism that is common for any type of rationing.

Furthermore, looking through the price categories, pricing pressures exist all across the set of goods and services for sale – yes energy and used car prices have risen by more, but price increases appear to be quite widespread.

This tells us that there has been a generalised increase in prices rather than just an increase “specific key sectors” as the article suggests. So this indicates that there is likely something increasing “all prices” rather than just the selected prices the article suggests targeting.

Furthermore, the lift in the US is higher than other countries have experienced – suggesting that there is an element of this that is US specific:

So that general lift is inflation right? Well not necessarily – and that is where everyone has been a bit slack. Inflation is “persistent growth in the level of prices”. If the supply chain interruption is temporary then this is a one-off price level change – which isn’t what we normally think of when talking about “inflation”.

This distinction often gets muddied as we care about the change in our ability to purchase goods and services – but the distinction is central if we are to think about the nature and role of monetary policy.

You may have heard of team transitory who are the individuals who believe it is supply chain interruption that is the primary cause of higher prices. This team does not anticipate future inflation once supply chains begin to function “normally” and in that context, a period of weaker price growth would be likely in the future once that occurs.

However, Elizabeth Warren recently took part of team transitory in another direction – by pointing out that measures of corporate profitability have increased. How is this relevant – we will get back to this soon I promise – but for now just remember that the view of imposing price controls is partially from this team.

Furthermore, even those in team transitory that do not believe in price controls are more sympathetic to leaving monetary conditions stimulatory (i.e. bond purchases and lower interest rates) and further government borrowing and stimulus payments. Why – because it is a temporary supply shock that has pushed up prices, and so allowing higher prices temporarily to prevent a decline in output/unemployment is seen as appropriate. At the very start of COVID, this was consistent with how Gulnara described the role of monetary policy in the face of such a shock – and a related lift in prices due to the Fed looking through supply chain disruption can be seen as consistent and reasonable.

A supply shock reduces income, and looking through the shock and allowing a one-off increase in prices (as opposed to trying to reduce demand to bring prices down) is seen as a fair way of distributing the shock – at least as far as monetary authorities are responsible for such things.

There is a different team of economists out there who see matters quite differently. Noting that the quantity of goods sold far exceeds anything seen in the past, this group views the focus on “supply chain disruption” as overstated – instead supply chains are overwhelmed because there is excessive demand. I see the article uses “team stagnation” which is a dumb name trying to discredit the idea – it is “team permanent”.

If monetary and fiscal conditions remain expansionary in the face of excessive demand, then prices will continue to grow – leading to expectations of future price growth among individuals and firms. These expectations then filter into price and wage setting behaviour, and become self-fulfilling – generating persistent growth in all prices. This is inflation.

The feather in team permanents hat is the differential change in inflationary pressures in the US relative to other “similar” countries. If prices are rising more quickly in the US than in other countries with similar supply chain disruption, then the additional price increase may well be due to greater domestic demand – and may be expected to persist generating true inflation and higher inflation expectations.

To this group a portion of the current increase in prices is inflation – as it is the start of a persistent process of rising prices.

Price controls, margins, and the price level

If we are experiencing genuine inflation then price controls are, to be frank, an incredibly dumb suggestion. Even when Tobin spoke in favour of such controls in 1981 (Economist Tobin on Inflation: How It Started, How to Stop It – The Washington Post) this was based on the view that it was not excessive demand generating the inflation – but the interruption of the oil price shocks.

<iframe src=’https://d3fy651gv2fhd3.cloudfront.net/embed/?s=cpi+yoy&v=202112101416V20200908&d1=19700103&d2=20220103&h=300&w=600′ height=’300′ width=’600′ frameborder=’0′ scrolling=’no’></iframe><br />source: <a href=’https://tradingeconomics.com/united-states/inflation-cpi‘>tradingeconomics.com</a>

There is a point here. Both of the teams noted above agree that the underlying supply shocks have consequently reduced incomes – and that higher prices are a part of determining who bears the reduction in “productivity” in some sense due to this shock.

A desire to then “control prices” is a wish to avoid the current distributional consequences. However, it is not costless.

If prices are not allowed to rise to ration the increase in demand, then something else will have to give – fewer goods and services will be available, the relative price anything without a rationed price (i.e. black market sales) will change, the intervention will create uncertainty about voluntary exchange, and finally once the controls are removed prices will simply rebound. The suggestion that selected prices are frozen is especially disconcerting as it will incentivise firms trying to reclassify products out of scope and lead to pricing pressure leaking out to other products while these products are arbitrarily rationed.

Contrary to the related articles that appear to suggest this isn’t true, we have endless examples of this occurred across the world – Venezuela, Argentina, the United States through the 1970s, New Zealand under Muldoon with freezes occurring between 1976 and 1984 (The wage and price freeze, 1982–1984 – Law and the economy – Te Ara Encyclopedia of New Zealand).

If instead we are viewing this as a one-off price change, then is the argument different?

If it was, it wouldn’t be the argument in the article linked above – which seemed to ignore the rationing that occurred for years following WWII as a natural part of the same issue, where the supply chain was shifting from significant central direction (to produce war equipment) to the private provision of consumer goods. The supply chain in the current situation has not had to change what it produced, or have been destroyed by a disaster, it is instead struggling under a mixture of higher costs and high demand.

Higher prices are the rationing mechanism at play given where the balance of supply and demand is – if we fix prices de facto lower the quantity of purchases further, then some individuals who value the goods at a very high price now would not be able to receive them. So far, no rationale. Furthermore, as the suggestion is to target specific “selected prices” – this will lead to increased demand for substitute products, leading to the pricing pressure leaking to other items. Given the rationale of targeting products who experience a price increase this is likely to lead to a poorly timed game of whack-a-mole with prices, all while the proximate cause of inflation – excessive aggregate demand – is ignored.

Such price fixing exacerbates the issue at hand – which is that households cannot get the goods and services they want given their real incomes. If instead of fixing prices we ensure that underlying fiscal policy is appropriately set to set a floor on individuals incomes, and that competitive issues are sufficiently dealt with to allow individuals to have sufficient power when they consume or go to work, then the distributional consequences are likely to be less severe.

If it is demand that is driving up prices, then the rationing functions over time – the high prices now push people who can wait to delay purchases, internalising the fact that supply chains are currently struggling. If prices do not reflect that, then in a rationed environment such products start to be allocated on the basis of luck and other forms of power – it will not reverse out the supply shock, and for some who complain goods are two expensive now it will simply make the goods unavailable.

Power dynamics and corporate profit

The concern about power dynamics is highlighted by the focus on corporate profit and “price gouging”. The idea here may be that producers are using this as a way to collude on higher prices and margins. As a result, there may be a way to undermine this collusion and increase quantity and reduce prices – solely benefiting households.

Now this is likely not an argument about monopoly or heavy concentration itself. The argument that a monopoly is taking this as an opportunity to charge customers more has to contend with the counter argument – if they could normally charge customers more why don’t they? Arguments that rely on “gouging” need to explain why this gouging doesn’t normally occur, and if it is a result of current scarcity why the price signal itself isn’t appropriate – after all, not having access to the product is the same as it having an infinite price to the consumer.

If the argument is just that demand is “currently high” then how is that different to stating that we should reduce aggregate demand which is what team permanent is saying? There is a distinction between their being demand for a specific product due to a crisis – and there being general high demand. And this article appears to confuse the two.

To try to make the best argument for this view about price fixing we need a coordination issue, we need some idea of oligopolistic firms and price setting.

The Green and Porter (1984) model of price setting among oligopolists may give us a solution here – during states of “high demand” oligopolists may collude and hold up profits, but when general demand falls they are unsure if they are being betrayed or if the economy is slowing. Given this they are more likely to “punish” by cutting prices when the economy slows. Here we have clear information of a “high demand” state, and so firms have agreed to collude.

The issue with this model is that is just doesn’t fit the data – rather than being pro-cyclical prices are often found to be counter-cyclical (i.e. Why Don’t Prices Rise During Periods of Peak Demand? Evidence from Scanner Data – American Economic Association (aeaweb.org)).

This result isn’t just in the annals of economic estimates – it is something you can see all the time by going to the supermarket. I’ve seen it for Nurofen (Why do supermarkets cut the price of medicine when people are getting ill? – TVHE), during COVID I saw it for toilet paper (Understanding Wellington and toilet paper – TVHE). Why?

That is where an alternative theory comes in, Rotemberg and Saloner (1986). If there are “high” demand and “low” demand states then the benefit associated with defecting from collusion is greater when demand is high – as a result, when demand is high and people are fully informed it is high, a price war and lower profitability is likely.

So why are corporate profits high, if our view of an observable demand shock would lead to lower profitability?

One way to do this would be to go back to view this predominantly as a supply shock rather than a demand shock, implying that post-COVID can be viewed as a low demand state. But that just isn’t consistent with the evidence relating to the quantity of goods being sold.

And that tells me that this IS an interesting puzzle – it isn’t about inflation itself, it is about the magnitude of the increase in corporate profits coming out of a pandemic during a period of elevated demand.

When I see a puzzle the first thing I want to do is look at the data more carefully.

Profit and the national accounts

In such a case the first thing I’d want to look at is what the data is – we are being told this is profit, but I know that national accounts don’t always match up with what we think. The key item I see here that interests me is the “Expenses exclude deductions for bad debt, depletion, and amortization“ – so bad debts that were written off, and assets and stock that was lost, are not included in expenses … and so form part of profit!

Inventory valuation adjustment (the IVA mentioned in the profits title) should have captured the majority of this loss as shown in the IVA figures:

Corporate Inventory Valuation Adjustment (CIVA) | FRED | St. Louis Fed (stlouisfed.org)

However, such revaluations tend to be fairly conservative. When combined with non-inventory write-offs in the period, this suggests that some of the increase in profit will only represent these costs to the business. As these are largely fixed costs we may still be surprised that firms have passed them on – however, if the costs were necessary to crystalise in order to being operating in a post-lockdown environment and businesses were liquidity constrained such pass-through may seem plausible.

Furthermore, if the current environment is very risky businesses may be unwilling to take on investment unless they are sufficiently rewarded for taking on the risk of their investment being sunk – which would also lead to higher profit levels.

A disaster that interrupted supply chains and destroyed inventories, and in the aftermath saw corporate profit rise when such losses are not recognised feels as if a major cost and risk parts of the cost shock is not being counted in the corporate profit figures. In an uncertain environment firms will want certainty about cash-flow, and will want to hold liquid assets in case they are faced with another shock – exactly the same way households function in such an uncertain environment.

Now it is useful to ask what else we would see in the data if this was an explanation. We would expect dividends to not change, while undistributed income and net private savings surges – as the undistributed income is essentially “invested” to pay for the costs noted above. Sure enough, this is exactly how the data looks:

Net private saving: Domestic business (A127RC1Q027SBEA) | FRED | St. Louis Fed (stlouisfed.org)

However, this does tell us that corporate firms were able to pass on these costs – which itself suggests that there is more going on. To understand this further we need to recognise that it is a bit strange to focus only on corporate profits and not the income of other capital and labour owners. So let’s take a look at that.

From September 2019 (pre-COVID) corporate profits have risen 29%. Over the same period compensation of employees rose 12%. These are all in current prices (Q3 2021, Table 1.14. Gross Value Added of Domestic Corporate Business in Current Dollars and Gross Value Added of Nonfinancial Domestic Corporate Business in Current and Chained Dollars: Quarterly | FRED | St. Louis Fed (stlouisfed.org)). With all incomes increasing and limited capacity to make goods and services this sounds a lot like a general “demand” shock driving up prices – a focus on only one income measure was hiding that!

The 17% percentage point gap between corporate profit growth and compensation of employee growth could plausibly be explained by increased risk in the trading environment, and “missed costs on business” in the national accounts figures that are being investigated. In this way, when we look at all the numbers as a whole it looks like a smaller puzzle – and more like there is a surge in domestic demand in the United States.

Ok why do I care

The distinction between this being a “supply shock” and a “demand shock” matters for what we would see as appropriate central bank action. If there is truly excess demand then tighter conditions are warranted – if it is mainly about supply disruption and a “price level shock” then there is less need for tighter monetary policy, and more of a need to communicate to manage inflation expectations.

Working through the data, the higher level of corporate profitability – and all incomes – makes the argument that this is a demand shock relatively stronger, rather than weaker. The argument given for price freezes does not support price freezes, but instead supports the tightening of monetary and fiscal policy the author says is inappropriate.

This is the key with economics – the author recognises this but there are other, unsaid, arguments in the background.

It appears the author is pushing for price freezes believes that there should be more government spending and investment in specific sectors, that the size of government should be larger, and that more resources should be directed by the state – and this is a legitimate position that they can take, and a legitimate position for people to strongly agree or disagree with. They are not thinking about inflation vs no inflation, but are instead worried about the political economy associated with reducing demand – and it occurring through reduced government spending.

In this world underlying “true” inflation is a tax, and this is a politically expedient way to have a greater tax burden to fund underlying expenditure. I would prefer the author was instead transparent and stated that they want more spending and taxation, rather than arbitrary calls to freeze prices based on corporate greed – but by obfuscating trade-offs they may feel that the world they desire is more likely to happen.

]]>About the author: Byte Size Story connects everyday economic issues with the big picture. The views expressed here are the authors. If you have any questions about the post please email bytesizestory@gmail.com.

One of the great debates of COVID-19 is whether governments should implement strict containment measures. Does the health benefit of containment outweigh the economic cost? What ‘type’ of containment is best? Globally there has been a broad spectrum of responses varying in length and strictness.

But there is more at play here than government policy. This post will explore the different responses to COVID-19 – government, population and global, and consider the extent to which the economic crash is driven by domestic containment measures. Remember the alternative is not ‘no containment measures and business as usual’ – it’s living with COVID-19.

Yes, the Government shut down the economy…

In late March 2020, NZ went into L4. Containment trades population health for the economy. They reduce the length and severity of transmission, but introduce highly concentrated economic suffering. Government stimulus, such as the wage subsidy, attempts to address this suffering. As the RBNZ measures it L4 shutdown 37% of the economy. More limited containment would have cost less, but with higher rates of transmission. It’s a trade-off.

OECD estimates of lockdowns globally tell a similar tale with countries like Japan and Germany shutting down about 30% of their economy. NZ’s lockdown was on the stricter end of the spectrum of containment measures.

Introducing containment measures means in theory that we can return to semi-normal life faster while avoiding high rates of COVID-19 transmission. That has happened to an extent. The return of community transmission on 11 August is obviously a hiccup. L2 costs the economy 8.8% in GDP while in place.

Stimulus packages have been key to cushioning the blow. COVID-19 stimulus dwarfed anything we saw during the Great Recession. Initiatives like helicopter payments, travel vouchers, wage subsidies and large spending programmes have been explored globally. Countries with large stimulus packages relative to the size of the economy tend to fare better. Stimulus comes at a cost to future generations, but with record low interest rates that cost is softened somewhat.

If there were no containment measures the COVID-19 the economic crash would play out very differently. While the direct hit to the economy could be softened, the crisis would evolve over a longer period with higher rates of transmission meaning we can’t go back to ‘normal’. People would determine their own precautions to stay safe – which brings us to a key point.

How society responds to COVID-19 independent of government plays a key role in the COVID-19 crash.

People aren’t behaving the same way because of COVID-19 anyway

Consumers aren’t spending and businesses aren’t producing as usual anyway. Let’s call this the population response.

With no randomised trial of lockdown vs no lockdown forthcoming, we aren’t going to know exactly how large the reduction in activity is because of the population response to COVID-19. What we do understand is that people make adjustments to avoid getting sick, or making others sick. That could look like avoiding restaurants or retirement homes. It could even look like banning people from a shop for not wearing masks. The population response leads to a fall in economic activity.

Cherry-picking Sweden, a well-known example of where containment measures are relatively light, citizens have been guided to behave responsibly with more focused health information for at-risk groups (e.g. elderly, pregnant women) and hospitality. Sweden has paid the price for this with high case numbers, but with reasonably light containment measures we have the opportunity to observe the population response in action. Sweden’s economy contracted 8.6% in the second quarter. That’s still a big drop.

South Korea, which also avoided lockdown, has ‘only’ seen a decline of 3.3% for the quarter. So perhaps cherry-picking isn’t going to get us very far, there are clearly more country-specific effects (e.g. stimulus). It seems the key is both in flattening the curve and how we flattened the curve. South Korea relied on a mix of vigorous testing, targeted isolation and tracing – rather than population-wide lockdown. Case numbers fell sharply in March with a bit of a resurgence in August. COVID-19 is far from over for any country.

Remember this is a global crisis

NZ is part of Team Earth fighting COVID-19 internationally. Let’s call this the global response. What other countries do in terms of flattening the curve and containment measures affects us all the way down here in NZ.

No matter what we do, we can still expect economic losses from other countries’ activities. Guan et al. model the global supply chain effects of COVID-19. They find the supply chain losses depend on the number of countries imposing containment measures, and the strictness of those measures. Seems obvious but it has an interesting implication. Even countries not directly affected by COVID-19 experience substantial economic losses due to disruption in infected countries. They estimate that NZ would still have a 2.2% value-added GDP loss if COVID-19 was confined to China by a strict two-month lockdown. This cost ramps up as the virus spreads globally and more countries impose restrictions. Of course, this isn’t a surprise – we operate in a globalised world whether we like it or not.

So economic losses from COVID-19 are unavoidable due to spillover. If countries do not flatten the curve, the spillover costs increase as the virus spreads and more countries respond. Containment measures impose costs within a country, but uninfected countries benefit from the reduced transmission. Not having containment measures (or at least flattening the curve) compounds the global economic pain as more countries become infected.

With the solution not belonging to any one country, we have to work together. That’s where entities like the WHO come in, though with their $2.5 billion budget they can’t necessarily do a lot. If one country has a new contagious virus, the right incentives need to be in place to respond with appropriate measures for global benefit.

To lockdown, or not to lockdown, what a difficult question

It hasn’t been possible to completely avoid the economic suffering from COVID-19. The fall in economic activity internationally means that every country is suffering no matter what they did. To an extent, the economics of COVID-19 and the long-run effects are beyond us at this stage. There will continue to be debate as to what the main contributors to the economic crash are, and what the best type of containment is.

The government, population and global responses all played a key role in the COVID-19 crash. Of these, the global response is the most important. Strict lockdown at the start of an outbreak greatly mitigates the global economic impact through reduced transmission. That’s not the full story, but it’s an important part.

In some ways NZ got lucky. We are already isolated at the bottom of the South Pacific. By the time COVID-19 reached our shores we already had the opportunity to learn about what was happening. Government-mandated containment measures were implemented with the full knowledge that this could get ugly.

COVID-19 will be seen as a turning point for government involvement in the economy. Alongside issues like inequality and climate change, COVID-19 highlights problems that are best addressed collectively. What comes next? We will have to wait to find out.

About the author: Byte Size Story connects everyday economic issues with the big picture. The views expressed here are the authors. If you have any questions about the post please email bytesizestory@gmail.com.

A lot of “words” have been spread across the internet on the issue, with people arguing about their effectiveness, complaining about how it hurts their “liberty and freedom”, and people saying they don’t like how it makes it harder to breath – hence why random idiots on the street feel empowered to yell at people who wear a mask, without realising that their willingness to lash out at other people makes them sound simultaneously stupid and scared.

But I digress before I’ve even gotten started – when it comes to wearing masks this tweet raises a great point:

I made a similar point when I was teaching on Thursday (having come in with a mask) – so I thought it could be fun to think about it a bit more here.

The mask externality

I’m going to look at this whole situation as involving a case where wearing a mask won’t prevent me from catching COVID – but if I had it, the mask, like that n95mask, will reduce how much I spread it. In that way, there is no personal benefit from wearing the mask, but my action helps others.

In that case we have a pretty clear externality – your decision to inconvenience yourself in a mask reduces transmission and so protects others from the disease. This is pretty consistent with how masks are described!

Now the key issue with it being an externality is that the knuckleheads I’ve described above don’t face the consequences of their own actions – their refusal to wear a mask doesn’t lead to them being more vulnerable, they just increase the chance everyone else will catch the disease.

So we would like a way to internalise this externality. Subsidising masks, mandating their use, paying people who wear them (eg a random lottery), all offer options.

But there is something else that makes use of the fact that the people who shout abuse at others are really just scared and are lashing out at others because of their embarrassment – the recognition that this is a coordination game!

The mask coordination game

If you are the only person wearing a mask you feel weird – like something from a budget version of a Star Wars movie. You start to think that others are judging you, that people will think you are “overreacting”, and that you might be wearing it backwards and so will look even more ridiculous.

In that environment you don’t want to wear a mask, even if you do want to protect others.

If everyone is wearing a mask you feel weird not wearing one – like the type of person who has pushed in front of everyone in a line without realising there was a line! You start to think that everyone is judging you, that you are selfish and aren’t taking this seriously enough, and you might even pull up your jersey over your mouth to make a pretend mask.

In that environment you want to wear a mask, even if you don’t particularly care about the people around you.

Here, the actions of individuals are strategic complements (much like working from home) and as a result if we can nudge a few more people towards wearing masks it can lead us to an equilibrium where everyone wears them – as opposed to one where no-one does.

In a world where most people wear masks, the prevalence of the disease falls – this would help to protect those who are vulnerable and can’t wear masks (due to poverty or genuine breathing difficulties) and also protect those who are too pigheaded to wear one (whose main difficulty is just being a pain in the ass). And that is success.

So lets remember that by wearing a mask when we go out we help to normalise it for other people, which in turn both protects us and others around us.

Also remember not to judge those who aren’t wearing a mask too harshly, as they either have genuine reasons and are facing a really difficult time as a result – or they are an incredibly insufferable prick and are facing a really difficult time as a result.

Be kind, get a mask on (if you can), and lets get this thing eliminated again.

]]>In the first few days back, I have heard a lot of people from around the building talking about how they prefer different work arrangements – and I’ve heard a lot of people say that they felt more work was being done away from the office. And yet, teams appear to be making the choice to move back to the office. Why is this the case?

Although it may be the case that the teams stated and real preferences differ, I suspect there is something else at play – strategic complementarity. Once we understand this concept it can become clear why we can end up in a worse equilibrium with regards to our work arrangements even when given flexi-choice, and why explicitly promoting working from home could be a “win-win”.

My choice depends on your choice

To understand how strategic complementarity works it is useful to look at an individual’s choice regarding where to work in two scenarios:

- When everyone else is working from home,

- When everyone else is working from office.

In scenario one, everyone else is working from home. Because of this all meetings will be online (via Teams or Zoom), there will be no workplace gossip to miss out on, and no-one will look strangely at you if you fold clothes while you are in a meeting. In this case there is a strong incentive to work from home.

In the second scenario, where everyone is working from the office, it becomes more difficult to work from home. You get shut out of meetings, people catch up on each other’s lives without you joining in, and a decision to fold your washing during a meeting would go down poorly with your boss. As a result, the incentive to work from home is much lower – and with the benefit of group chats and getting heard at meetings at work you have a strong incentive to also go to work.

Because you have a greater incentive to work from home when others do, and a greater incentive to work from the office when others do, these actions are strategic complements. If someone decides to work from the office, it increases pressure for other people to work from the office – and if someone switches to work from home it increases the pressure to work from home.

This leads to multiple equilibria. Namely, when the number of people choosing to work from home increases, the effectiveness of that type of arrangement works well and an additional person will have an incentive to work from home. Similarly, when the majority of people choose to work from the office increases, it functions well as well and an additional person has an incentive to work from the office.

In a simplistic example, people in both cases choose to go with what the majority is doing, and we end up with two equilibria points – all work at home or all work in the office.

Is the equilibrium we choose the best (Pareto Optimal)?

The answer is not necessarily. The equilibrium selected isn’t based on the underlying preference regarding working at home or the office – but instead is history dependent or based on what has happened in the past and what people expect others will do.

In our example above it sounded like the individual would like to work from home all things considered – but with a push to get back to normal and get in the office they know that their workmates will be in the office, as a result they also go to the office. As they are making their choice to go into the office based on the expectation that others will go to the office – and not because they actually prefer working in an office – this equilibrium is Pareto Inferior!

So what is the takeaway here? Just because historically, everyone chooses to be in the office, it doesn’t mean that we shouldn’t be open to better ways of working. If it is true that people are just as productive, and are happier, when working from home then that is something worth encouraging – but due to strategic complementarities it is not something that will organically occur if we simply state that flexi-work is allowed.

]]>In this post I want to discuss what drives the households to behave in this way, and how this comes into our thinking about economics and monetary policy.

I have to admit, when the lockdown announcement took place, I was one of those nervous households who decided to cash out money from my bank. My personal reasoning for that was the scars left by defaulting banks during the collapse of the Soveit Union, when my parents lost all their savings because one of the main banks failed.

However, what are the economic consequences of this behaviour? We might say that this is saving behaviour – but the people withdrawing their funds were already saving them. Instead people are hoarding cash for some reason. This is likely due to fear of bank failure (my reason), but a similar thing can happen even when individuals shift funds from a long-term savings vehicle to near monies (eg a checking account). Examples of this are:

- people cash out money or move it to a chequing account due to uncertainty of their employment status in the future

- people decide to shift allocation of transactions, for instance, waiting until the end of the month to make bulk purchases.

In both cases the increase in demand for cash is also an increase in demand for liquidity. So what does this mean for our broader economy?

Why are we concerned?

Cash hoarding affects the circular flow of money in the economy. We all know the circular flow diagram, and how real transactions are made between buyers and sellers. However, these transactions involve a countervailing exchange of money. So as Matt noted we can think of this both in terms of the money flow (MV) and the nominal income flow (PY). Sudden hoarding will reduce velocity for the same stock of money, thereby leading to a reduction in nominal incomes. How do we think about this?

The hoarding comes from money demand. So let’s think about that with a fixed (real) money supply. Here money demand declines with the interest rate as the opportunity cost of money (the return available from illiquid assets) is higher.

Above the change in money demand could be due to:

- An increase in output. It is that shift, where people require greater money balances to facilitate these transactions which defines the traditional LM curve.

- An increase in precautionary saving held in near monies form (cash, or a chequing account that a bank struggles to use as an effective basis for loans).

Here, with a fixed stock of money, both of these things would push up interest rates. Hence this forced a movement up the IS curve and a reduction in output.

But this isn’t how a central bank responds to this change – a central bank like the RBNZ accommodates any increase in money demand initially by setting an interest rate peg. As a result, such a surge in demand for money doesn’t lead to rising interest rates unless the central bank decides not to accommodate it!

What does it mean for us?

In a broad sense having an interest rate peg instead of a quantity of money peg means that we don’t have drops in output due to tight monetary policy – in a sense. The central bank accommodates shifts in money demand, thereby automatically meeting any change in the money supply required to meet liquidity needs.

However, the use of QE and other instruments to support liquidity show that this process isn’t always easy – and a fixed interest rate peg doesn’t always translate into sufficient liquid funds to meet this demand for liquidity. As a result, monetary policy has a very real role trying to ensure that this need is met.

But there is one caveat- the increase in uncertainty associated with something like the current COVID crisis does not just shift that LM curve – it also shifts the IS curve left. I have discussed this in terms of investment before.

If the central bank is able to manage liquidity issues with its interest rate peg appropriately, then all that matters is the question of whether there is sufficient demand for goods and services – a question that requires different answers (changes in the interest rate, discretionary fiscal policy). In an IS/LM diagram such monetary policy is represented as a “shift” in that curve.

As a result, the example of people hoarding cash gives us a great insight into the dual roles the RBNZ is playing in both managing money markets and stabilising economic activity – and gives us a framework to consider the two clearly.

]]>This raised two questions from me:

- Is this evidence that COVID was a supply shock more than a demand shock?

- And does it mean that monetary policy should respond?

I want to think about the later point in this post – as the first question will get answered as we work through it.

The argument

According to the Taylor rule, in normal times, when inflation moves away from its target, the central bank should respond with an increase in interest rates. There are two reasons for this i) in order to keep the same real interest rate the nominal interest rate needs to rise ii) a higher real interest rate is required to reduce inflation back to its target, which requires a higher nominal interest rate.

However, this rule is based on the idea of a typical economic cycle involving demand shocks. What we are observing right now is not simply the result of a demand shock but also involves a supply shock – we are in the middle of a pandemic.

So if the increase in prices was due to the pandemic there may be no need to respond. So is this the case?

The March quarter CPI was not a COVID price boost

Stats NZ has indicated that CPI growth in last quarter had very little to do with the pandemic , as the surge happened primarily in January 2020. It appears the CPI increase was largely not pandemic related. The increase in alcohol and tobacco prices stemmed largely from excise tax changes, food price growth largely occurred in January, and the sharp lift in rents was due to a general shortage of property.

Stats NZ noted that COVID did not impact on data collection for this quarter, so this appears to be a representative sample of prices – a sample that is indicating real broad-based price increases. Even if supply chain disruption was partially to blame for higher tradable inflation, non-tradable inflation was also above expectations.

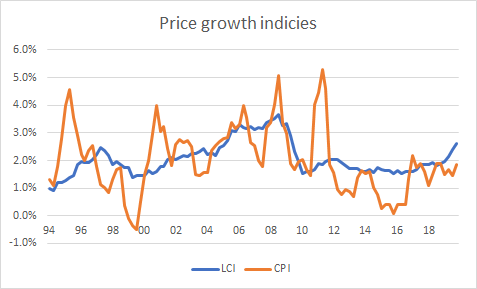

This does tell us that, perhaps, the economy was becoming overheated and perhaps interest rates should have been higher if COVID did not happen. This is consistent with the evidence from the LCI in this post.

So if it isn’t COVID related should the RBNZ think about hiking rates?!?!?!

No.

We were in the same position for the GFC, when before June 2008 inflation was rising and the central bank had been lifting the interest rates. However the crisis changed the direction of the economy.

COVID is a shock that has reduced aggregate demand, and they are responding to that shock – not the situation that existed prior to COVID – when they set interest rates now.

Furthermore, even if the surge in inflation was due to COVID, what matters is what will happen to inflation going forward. If prices surged then this is due to a short term supply shock which will reverse out in future as businesses open and supply line improves (as described in these posts).

With monetary policy we can look through the supply shocks and we are interested in what will happen to demand over time – including a consideration of whether these supply shocks influence inflation expectations. If the increased prices are one, then it doesn’t necessarily increase inflation expectations and it is appropriate for the bank to look past it.

]]>According to the media, NZ shoppers have faced this as well.

“Some customers have taken to social media to complain that prices of items like soap, meat and fresh veggies have increased sharply.”

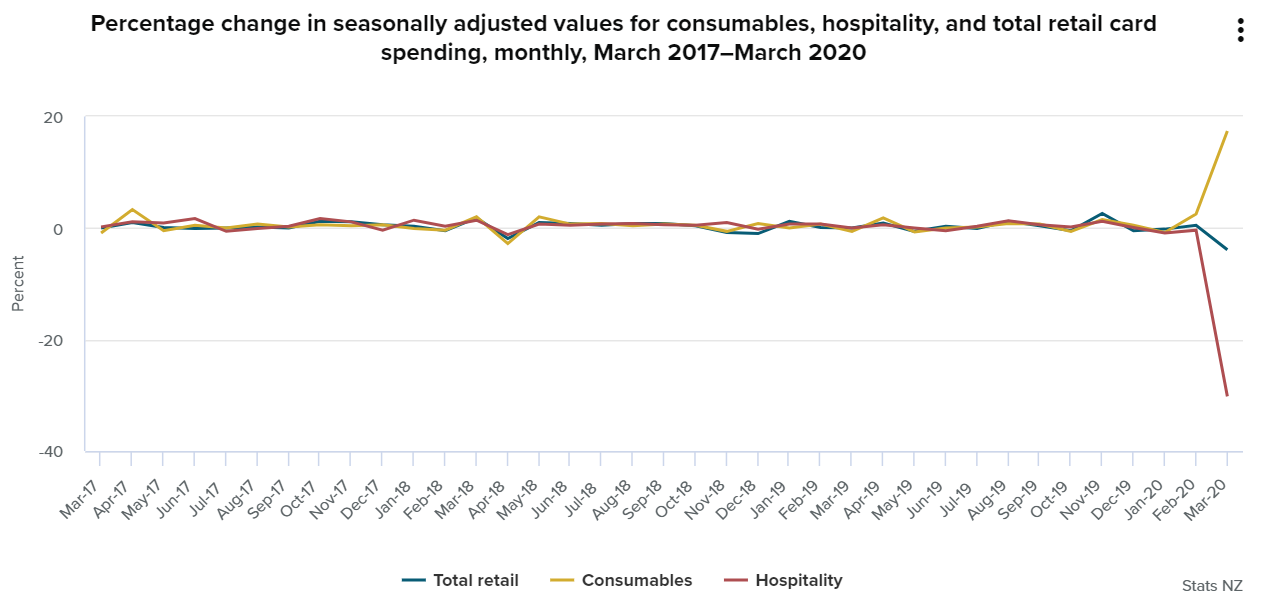

However, supermarkets kept denying the fact. It’s hard to judge the case from my experience, as Matt and I were lazy and were primarily eating outside before the lockdown. However, Stats NZ provides data here – so let’s look at the latest release on the Food price index to figure out whether the customers are right.

Spending on groceries

Before looking at this, let’s think about the what has happened. Fear around COVID and the quarantine by the end of March will have driven down demand for going out to restaurants, travelling, and going to movies – but driven up demand for groceries.

Why? People were keen to stock up in case they couldn’t get food, and as they aren’t eating out people now need to get more of their food from supermarkets (our case).

Stats NZ’s electronic card spending data indicates that this was indeed the case in March.

So we know that grocery store demand surged, so what does that mean for prices?

The food price index

Our initial economic intuition tells us, high demand in goods drives up prices as willingness to pay of consumers rises. This is reinforced by the fact that supermarkets were hitting their capacity constraints as noted by the comments around toilet paper.

But then this didn’t happen.

Stats NZ March food price index shows that grocery store food prices rose 0.2% in March relative to February when adjusted for seasonal variation.

The “real” figure is likely a bit larger, as supermarkets dialled back their “promotions” during the COVID crisis – and these deals are often not included in price statistics. Even so it looks like supermarkets haven’t increased prices in the face of rising demand, limited competition, and capacity constraints. Why??

Why haven’t supermarkets increased prices?

There are two clear categories for why they would not have increased price – the relationship between the price now and demand in the future, and imperfect competition.

For the first, the price supermarkets set now will influence demand for their store in the future. There are reputational effects from changing the price (goodwill) which are likely heightened during a pandemic, there are consumer expectations of prices which are anchored to the price now, and for franchise owners there is also the difficulty in getting them to coordinate prices with each other if you intend to significantly change the way products are priced.

In the current situation, supermarkets don’t want to get a reputation of not being kind – or of being price gougers – so will be sensitive to increasing the price.

The second is competition. If the two supermarkets were hypercompetitive and also had no market power over their wholesalers/suppliers then they would be forced to change prices with changes in supply and demand. But they haven’t. As a result, they could have market power in either of these markets.

On the sales side this could be a situation of tacit collusion. When demand is high supermarkets compete more to capture a share of the “high reward”, leading to a breakdown in tacit collusion that normally exists. Arguably, this idea is supported by the drop in grocery prices during December (Christmas).

Combining the concern about looking like bad people, and an increase in competition between supermarkets to get these new customers, it makes a lot of sense that they haven’t increased prices when faced with a surge in demand.

However, if demand remained higher forever, then these explanations suggest that eventually prices would rise – they only work because this is a temporary “high demand” or “high reputation cost” state. If restaurants are closed for a year expect to see more upward pressure on grocery prices.

Gulnara has done a great job of highlighting the broad way to view this pandemic and understand how such a shock works through the economy – but I think it is important that I give you some cautious advice about applying the 2020 lessons to your time.

Ultimately you can’t just take the economic consequences of a past pandemic (even if this virus itself looks similar) and state that this will be the consequence of it now – a lesson we have learned when looking at the Flu of 1918-20 in our time. However, I want to talk through some key issues to help you think about it.

A pandemic doesn’t change the capital stock – this matters

Relative to the 1918-20 and 2020 pandemics the stock of capital is an even more important determinant of output in 2120. And this matters for how we think about what activities would occur. Let me give an example of how home consumption of pizza can differ to explain.

Example

A quarantine involves limiting social contact – especially social hubs – in order to slow down the spread of the virus. This video explains it well. So the necessity of shutting down activity will depend on how much human contact is involved in that activity and the related hub.

In 1918-20 there was no home delivery of pizza and a restaurant that sold pizza would be completely shut down during a quarantine. Customers would meet together there (a risk), the service would be from a person (another spreading risk), and the kitchen was filled with people (MORE RISK).

By 2020 things were different. There was home delivery, which removed the hub associated with consuming the pizza. Furthermore, there was an increasing possibility for delivery to be done by drone instead of person – which removed this risk. But we still need people in the kitchen constructing the pizza.

Putting several people in close proximity and then having them send food to hundreds of others leads to a hub that could spread the virus – if one chef has the virus then there is a risk it can be spread widely. As a result, we had to shut down pizza delivery and the restaurant just like in 1918-20.

In your time everything is done mechanically anyway – the pizza creation and delivery come with no risk for virus spread. As a result, all that needs to be shut down is the restaurant/human contact end of the process – the loss of value is directly associated with the loss of that particular service, rather than the substitute associated with having pizza at home. So the underlying amount of consumption activities that get restricted are much smaller!

Furthermore, in 2120 restaurants commonly provide virtual reality seating at home – this service is a high quality replacement for people heading out to meet up without the risk of virus spread. Given restaurants can do this so cheaply the actual loss of GDP is very limited.

Sidenote: I am amazed you still call it GDP given all of the bad press in our time – I understand why the measure is still useful, but just surprised you haven’t changed the name!

The embedded value of labour and post criris

A related point to this is to think about what is actually going on with the underlying value of labour.

Over the past 100 years a large number of technological advances have generated direct substitutes for labour at achieving tasks – without really creating tasks that are complementary to the capital input.

This has led to a situation that is a bit weird – why when you go to a coffee shop in 2120 is everything performed and serviced by automated forms of capital (eg robots), while the employees sit there in a supervisory role?

Now if this shock implies that you can generate the same product – that is valued in the same way by consumers – without labour inputs then this points to a situation where the labour input has zero marginal product. Why does a profit maximising firm even use labour then?

A risk I see coming out of this pandemic is that capital owners may recognise they don’t need labour in 2120 and have only been offering jobs due to history dependence. If this happens this will reduce the living standards of those who are not endowed with capital (or the ability to accumulate it). This process of business learning is related to bounded rationality – those who are making decisions within the firm have come under pressure, and may now make different decisions.

So please make sure that the state is doing appropriate redistribution to ensure there is some equality of opportunities here – we aren’t all born with access to capital, and if the return on labour is close to zero this is very problematic.

Separate supply and demand, short and long run

In the above example the key risk was associated with changing consumption patterns by households – the true “potential” for the economy to produce is unchanged.

This differs to our pandemic, where the necessity of stopping people working does temporarily reduce what can be created – it makes labour unavailable, and it also increase the shadow price of both other inputs that have become unavailable for the production process and products that are now available.

As a result, your pandemic is – as it should be – predominantly about public health. But, your economic shock is much more about demand as explained above and as a result should be much easier to deal with!

Although I imagine what constitutes aggregate demand is even more confusing in such a world, the idea that output does not need to be any lower in order to prevent the spread of the disease implies that all that matters is effective demand – and through monetary policy or by transferring funds through taxes and transfers it is possible to shift this.

Of course, if the composition of demand changes post-pandemic then there is a question about whether certain specific vintages of capital need to be written off. How flexible is capital in 2120? Does labour still have value due to greater flexibility in this time, or are the skills associated with human capital even more rigidly fixed – I have to admit to not being sufficiently familiar to the factors of production 100 years in the future.

So yes, there may be long-term costs – but you don’t have to worry about the short-term economic consequences we face if you don’t want to.

Keep your heads up and be kind

We know that you are going through a stressful situation – we are in the midst of our own crisis now and in many ways it feels as if things will never return to normal. When looking a natural aid to help yourself handling stress, check here the garlic cookies strain review by fresh bros.

These days it’s hard not to get overwhelmed once in a while. Between juggling work, family, and other commitments, you can become too stressed out and busy. But you need to set time aside to unwind or your mental and physical health can suffer. To help yourself try this new Budpop delta 8 carts

But an idea that gives me peace is the realisation that the things we have all built together have not been broken by the virus – our relationships, our machines, our knowledge, and our humanity.

Once the medical issue has been dealt with we will return to sing the same songs, produce the same products, and share the same experiences as we did in the past – we just need to work together to spread the pain of what has happened now between us, instead of throwing it all on the shoulders of a few unlucky individuals and families.

Our love and our kindness is what pulls us through this pandemic, and similar empathy – along with a recognition that we don’t have to put people through economic pain due to “reallocation” or “liquidationist” views of the world – will make sure that you all come through the other side of the pandemic stronger than you went in.

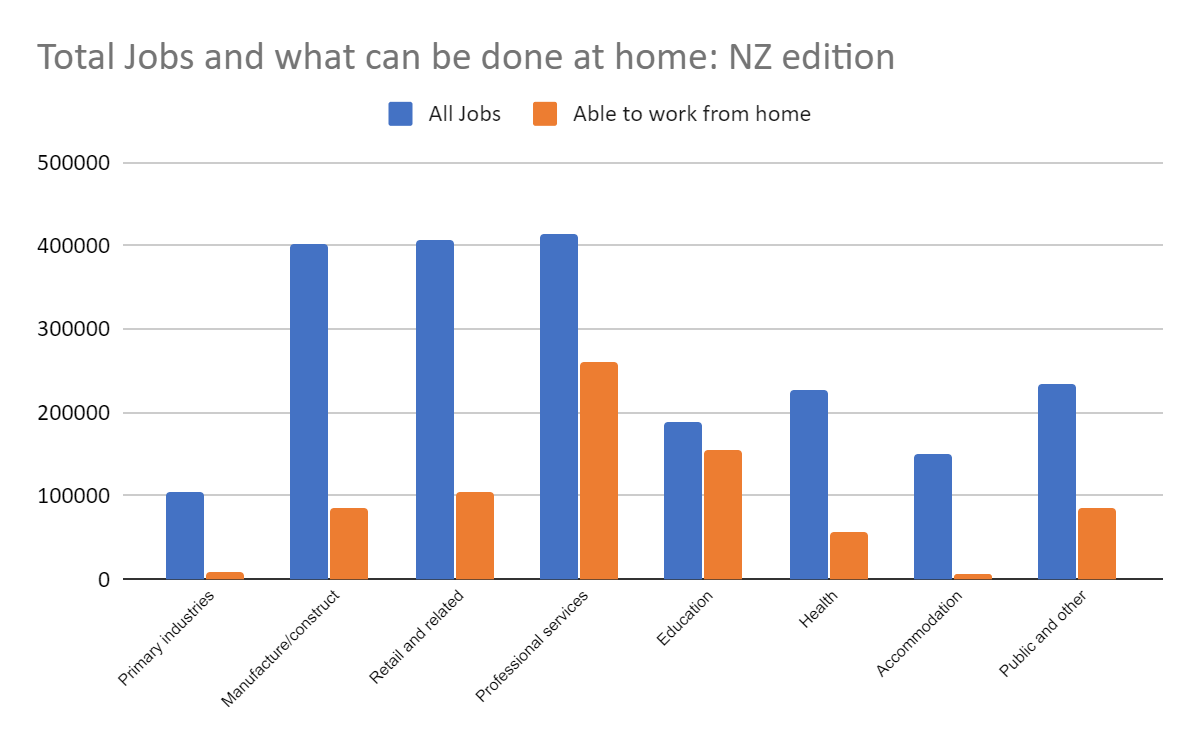

]]>I have calculated rough estimates for New Zealand regarding the labour markets capacity to work from home. Applying the same industry correspondence to New Zealand (based on LEED data) and using the US weights (so assuming the same ability to work from home by industry) I have calculated that 31%-36% of jobs can be done from home.

The US estimates

In their paper, Dingel and Neiman use a classification of occupations that evaluates the feasibility that occupations can be performed from home. Given that and the employee counts by occupation the authors estimate that 32%-34% of US jobs can be performed from home.

To construct their measure, the authors use information from the Occupational Information Network – which is a survey that classifies the type of tasks that individuals are undertaking. Given this they can identify work that can be done at home. They also construct a “manual” measure based on introspection. This second measure gave the slightly lower estimate.

Note: should be read alongside this early survey evidence from US: https://john-joseph-horton.com/papers/remote_work.pdf. In this paper they find that, following the lockdown, 34.1% of people stated that they are now working from home while 11.8% have been laid off or similar.

New Zealand estimates

Dingel and Neiman report the variation of shares of jobs across cities, occupations, and industries. The industry classification used in the paper broadly matches with the ANZSIC06 industry classification we use in NZ.

Here are the total number of jobs in NZ by industry in the 2018 year (averaged), and the implied number that could work from home by broad-group. To apply in such jobs, a team such as a jobs talent acquisition handles it.

Source: Infoshare Stats NZ, and the weights in Dingel and Neiman.

Applying estimated weights from the paper, we calculate a range of 31-36% of jobs can be performed from home in NZ. This varies significantly by industry, with nearly 83% of education jobs and 63% of broad professional services jobs able to be done from home – while only 3.5% of jobs in the accommodation industry could be done from home.

Caveats: These calculations are indicative only, as it assumes a similar ICT take-up rate between NZ and USA. However, this framework provides an incentive for a deeper research that can be done using NZ administrative and Census data.

]]>Given current concerns most focus is on the question of how to deal with the consequences of a disaster now – in a way that doesn’t lower productive capacity in the future. This is a good frame, and the New Zealand discussion has been strong relative to a lot of other countries.

However, even though a lot of the stores are closed now “demand” management is not just about that future – it needs to occur now as well. As a result, monetary policy does have a role.

If the shops are closed how can demand management matter?

Closed shops due to COVID are a supply shock, as the price of the things they sell has essentially shot to infinity. But that isn’t the only effect.

Because in so far as resources can “transfer” into a better use during the crisis we want them to, this helps to reduce the fall in output, prevent hardships, and support businesses. It is important to find ways to improve outcomes from these issues directly given that it is a “large temporary (but persistent) supply shock [eg business continuity loans, hardship payments, and employment protection] but demand policies – such as cuts to the official cash rate at QE – help with that transition.

In this way, let’s get back to the nominal income (or NGDP targeting) idea. I have outlined this in two posts here and here. In the second I noted that it gives people incentives to invest and take on actions knowing that, if they make a reasonable choice, they will experience a given increase in their nominal incomes. This helps to support necessary transitions.

Similarly, Ben Bernanke proposed an idea of temporary price level targeting, which recommends central banks keep rates ‘lower for longer’ . Bernanke believes it can help reduce longer-term rates and encourage spending today because of reduced expectations of future short-term interest rates and because of raising expected future inflation.

As a result, even if the unconventional monetary policy actions seem spent, and fiscal authorities do not want to bear further debt or risk, there remains a chance for central banks to promote level targeting. And, unlike many other tools, level targeting appears extremely appropriate for dealing with a temporary but persistent supply shock – as it helps deal with coordination coming out of the shock given the certainty about nominal income or prices (depending on the target used).

It is too easy to say “this is a supply shock, we can do nothing” or “this is a temporary uninsurable supply shock, so the only thing that must be done is subsidies and loans”. However, in a world with remote work and delivery, and an ability to substitute even service work to be done from distance, there is real potential for demand management to help keep businesses working and people employed as a complement to such supply policies.

]]>