I keep receiving emails that Star Wars Squadron is only $2.50. Wild! I love Star Wars, and when I was a kid I loved flying around all the planes and stuff.

But why such a big special? And why are lots of computer games on a big sale now?

I mean surely this is the time when demand is high (a lot of people are on holiday) and computer games are a durable good (you pay up front, and then consume them over time).

As a result, this must be the time when people are most willing to pay for it – and the incentive to discount must be pretty weak because if you sell a game to someone now, you can’t sell it to them again in the future. For more fun, try link slot games where you can enjoy exciting gameplay and chances to win.

So let’s have a think about why this may be going on – and I promise not to talk about tacit collusion this time. Instead lets talk price discrimination.

A tale of three consumers

Imagine we have three people who all get excited when they see the following image.

One of these people is a 16 year old from a high income family, and a social network of friends in a similar position. Access to a new game depends largely on payment by your parents due to the need of a credit card – even if you’ve gone off to earn the money yourself.

In terms of time you have plenty of time to play games where you would otherwise be practicing hand stands and breaking windows. As a result, such purchases tend to occur when you are able to access them as an external gift – such as during a birthday or at a game launch when you can point out your mates have gotten it.

In this situation, your demand does not really vary with prices, and you are exceptionally impatient about having the game at release.

Another person is a 21 year old university student with fairly strong credit constraints. Although your time is a bit more constrained than at 16, you still do have a variable amount of leisure time – focused specifically at study breaks. Furthermore, others that you will play with are available at similar times – so individuals will coordinate on games.

This combination of factors means that demand can vary quite sharply with price, as groups of students coordinate on different games on the basis of their price.

Finally you have a 35 year old professional with a family, significant work commitments, and some disposable income. Their network is also similar people. Work and child requirements are not so coordinated, and as a result there is less coordination between people about playing together.

Furthermore, you have very limited free time – which means that you don’t really expect to get too much value from a game, as you doubt you’ll have much time to play it. However, you do have significantly more income.

This type of consumer has relatively low price elasticity … but for a game that is multiplayer focused also has a much much lower value for the game.

All three of these individuals would enjoy playing the game – but they differ in the opportunity costs they face from doing so.

- 16 yos: Material resources are available at fixed times, and plenty of time. So the opportunity cost is associated with the specific time of purchase (a form of limited material resources).

- 21 yos: Have limited material resources, but plenty of time. As a result, the key opportunity cost is other things they could spend money on.

- 35 yos: Have material resources, but no time. As a result, the opportunity cost is more associated with not having time available.

Price discrimination and our Steam sale

Our firm is selling a piece of software online. The marginal cost of doing so is close to zero.

As a result, in a perfectly competitive industry the price would collapse to zero. However, such an industry wouldn’t be sustainable – as no-one would make these games. So some amount of market power exists which generates the revenue to cover fixed costs as well.

We know that the game seller is setting marginal revenue equal to marginal cost – to sell an extra unit they have to cut the price to everyone, and they do this until the “extra dollars” they get become zero.

If they had to set the price and leave it, then we can look at our three groups to figure out the price:

- If we only sell to 16 year olds we can set the price pretty high!

- If we include the 21 year olds we run into the issue they can’t pay as much – so we have to sell at a lower price for both.

- If we include the 35 year olds, then they aren’t willing to pay much at all – so we have to set the price very low to cover all of them.

So the seller will compare marginal revenue and cost, and determine what group is the marginal group. They will only sell to that group and the groups willing to pay more, and the groups with a lower willingness to pay will not receive the product.

Lets picture that the price was $50, and it was only sold to 16 year olds in this instance.

This is “inefficient”. Why? Because it costs $0 to provide the game, people like the 35 year olds do have a small positive value from the game, and yet there is no transaction between the game seller and the 35 year old!

Ohhh no, lost gains from trade!!

So why not charge them less based on the age on their passport? Well we can’t age discriminate. Steam offering different prices based on a persons age would lead to manipulation and is illegal.

But instead we can achieve this by changing prices through TIME – based on when the game is released, and when it is discounted.

A $2.50 sale after Christmas – when the 35 year old is on leave from work, everyone else is getting gifts, and they have had some fun playing with their kids toys – is pretty appealing. If the retailer has already saturated the 16 year old and 21 year old markets, then they are really just servicing 35 year olds when they do this sale.

When the game was released it was $50. The game was advertised, and in some places sold with, a joystick. A lot of 16 year olds love spinning their ship around and around to annoy their friends when playing with them (speaking from experience) – so there is significant value from buying at release when there are a lot of people to do this to, friends and people online. This was in October 2020.

In the three years inbetween, there were plenty of sales – as well as a lot of negative reviews regarding bugs and a lacklustre story. Whether these things matter I don’t know, as I’ve never played or watched the game, but for our price sensitive 21 year olds it will have taken a number of school holiday sales to convince them to give it a go. $20 or $30 sales may have worked for this group.

If this is a correct description of the market, through time based price discrimination the retailer can charge 16 year olds who want the game at launch $50, our 21 year olds who are willing to delay $20, and the relatively disinterested 35 year olds $2.50 – providing the game to a set of different groups who value it, and making the highest profit.

Now we can’t just randomly set the prices lower at different dates as it is a durable good. If everyone knows it will be $2.50 on a certain day, then why would they pay $50!

- It is uncertain if, and when, the game will become $2.50 – hell it took 3 years!

- People may value having the game early – or more specifically, coordinating when they have it to play with other people. The people who value games in this way will pay more for receiving the game at an earlier date.

As a result, the ability to price discriminate is limited by the ability for a high paying type (16 year olds) to tag themselves as a different type (i.e. a 35 year old). If the $2.50 sale was one month after release, the 16 and 21 year olds would likely delay the purchase by a month.

But look at when the $2.50 sale has occurred – three years after game release, at the start of January, after Christmas when middle aged people who don’t commonly buy games are sitting around thinking about their youth.

Great time to convince them to drop half the price of a coffee on something they will never open or use … after customers that were willing to pay a bit more have already paid.

]]>It’s Boxing Day – and I’ve already used up the idea of discussing the now largely missing Boxing Day sales. And the idea that Boxing Day is increasingly lame is common across years.

So instead the focus of today will be on a different industrial economics topic – the state of competition in Australia. Specifically, does the lack of Boxing Day sales tell us something about the level of competition in Aussie?

For this I’ll be borrowing heavily from a Research Note on the topic by my stellar e61 colleagues Dan Andrews, Elyse Dwyer, and Adam Triggs (now of Mandala). I’ll also be relying on this paper by Jonathan Hambur from the RBA.

However, all misunderstandings and inappropriate comments are my own.

Competition in Australia

Yelling that businesses aren’t competitive enough is a great way to get attention, and push for “getting something for nothing”.

What do I mean? If firms are very uncompetitive then we know they are generating an economic rent – and that this rent could be redistributed to someone (consumers, workers) without undermining economic activity.

As most of us are consumers, the unfairness associated with being charged what we view as too much makes this narrative pretty appealing – and a variety of thought leaders who want to persuade us love nothing more than packaging up ideas we find appealing, and repeating them to us ad nauseam.

However, that doesn’t mean there isn’t some truth to concerns about competition. In fact, it is in the interest of people who are earning economic rents to pretend that daring to tax these rents, or reduce barriers to entry, will undermine some magical value they create – and will use the language of productivity and innovation to make us scared of doing anything.

So given that public narratives are tarred with ideology, lets step back and work things out for ourselves – by looking at some data.

When looking at the State of Competition, the e61 authors focused on the degree of concentration in Australian industries – specifically they focus on the market share of the four largest firms in every Industry Group (3-digit industry code).

There are two graphs I’d like to focus on – noting that the Research Note adds a lot more detail if you want to give it a read!

The graph above shows that these concentration ratios are higher in Australia than the US – so Australian industry groups tend to have a greater share of sales that occur among only four firms. Now this could be partially the result of Australia’s smaller markets.

But then we come to the graph below – concentration ratios have risen across a number of industry groups ESPECIALLY retail sales and mining. As our focus today is on retail sales, this tells us that retail sales activity has become more concentrated among a small number of firms.

The other paper tells us that this rising concentration has also been associated with rising margins earned by firms. However, when compared to other countries that increase in margins has been a bit smaller. Margins in Australia are high – but it isn’t clear that this has been a worsening issue over the past 20 years.

What do bad sales tell us about competition?

So Australian industries are concentrated, margins in Australia are fairly high, and judging by my shopping attempts today Boxing day sales are lame. But does this actually tell us anything?

Concentration alone is actually not telling us as much as we hope. It is possible to have 100s of reasonably sized companies in an “industry” but for each to have significant market power – due to the spatial or product dimensions varying between firms. On the flip side it is possible to have a single firm but very little market power (effective competition).

Margins are also tricky, as the necessary return for entry to the industry depends on risk and the needed return to also meet fixed costs – post Global Financial Crisis there has been in lift in both uncertainty and regulation, both factors that require higher margins to incentivise entry.

But does firms reluctance to provided good boxing day sales mean there is a competition problem?

Intuitively this makes sense – businesses look like they are colluding (even if tacitly) to avoid giving me a cheap Xbox.

However, what is boxing day? It is a period when everyone is off work and goes out shopping – there is a huge surge in demand, and people have the time to shop around.

Given this description, this is when a firm with market power would price discriminate by cutting prices to attract these customers who are relatively more willing to substitute between firms. While more competitive firms would simply face a lift in demand and thereby charge higher prices.

So what is it – are the bad boxing day deals a sign that competition in Australia is stronger than in the past, or is it a sign of a competition issue?

Tacit collusion – a tale of two models

OK so we are going back to our description of Boxing Day in 2019, and one of our favourite descriptions of Oligopoly collusion traditionally.

The difference is that this time we are focusing on whether Boxing Day is telling us anything about competition – specifically, does it tell us if retailers are tacitly colluding in setting their prices during Boxing Day?

If we accept the Green and Porter (1984) model of tacit collusion and competition, then firms collude until they think other firms are cheating (a trigger strategy). During Boxing Day the stores are full up, and so there is no need for sales – but as soon as demand drops, firms think that this is because other businesses have “defected” and stolen customers. As a result, the sales will kick off when the stores are not so busy.

In this world, the disappearance of Boxing Day sales is consistent with collusive behaviour – but we’d expect to see some big New Year sales.

If we buy the Rotemberg and Saloner (1986) model of tacit collusion and competition, then tacit collusion breaks down during high demand states – as firms face an out-sized incentive to try to steal customers. In this model, a collusive equilibrium would involve situations where there are big sales following observable increases in demand – like Boxing Day.

We all know what Boxing Day is – as a result, the second model appears more appropriate for understanding whether we generally have collusion. But if we buy this model, it would suggest that one of two things must be true:

- Competition has increased and as a result there is no long tacit collusion that falls apart on Boxing Day.

- Competition has declined, and as a result retailers can maintain tacit collusion even when the reward for reneging is huge.

Teasing out the difference between these is pretty tough. When it comes to the service station industry, David Byrne from University of Melbourne has shown that tacit collusion has increased among petrol retailers, with a related e61 event study reinforcing this.

But without more information we just can’t say which way things have gone among retailers in general – such is the nature of industrial economics!

Sorry, no conclusions for today. If it makes you feel better take this post and demand your local retailer reads it – in order to avoid doing so they’ll probably give you a discount

Now I have no problem with breaking up monopolies, and I’m a huge fan of clear competition policy. But this isn’t going to deal with the “inflation” problem we are talking about. Let’s chat about it.

An earlier post here on “price controls” discusses a number of specific matters in more detail, but I think a higher level discussion would also be useful. To that end, I thought I’d share a twitter response I made to some bloke going on about corporate greed and inflation:

As you may have noticed in earlier posts, I haven’t given up on the transitory narrative (based on central banks managing expectations), but as Michael Reddell notes the outlook for this narrative does keep worsening:

I did your first year econ course, you said monopolists were price setters, so we need market power to get greed to influence prices – checkmate

Nice, and I hope you enjoyed the course. Sadly you are only remembering the words that we use, not the full nature of the content with that response – sometimes the way economists name things mean they can be misinterpreted.

A “price taking” firm only has the incentive to charge the market price – this does not mean they have to accept some fixed mark-up on cost, it means that market conditions determine the price they are incentivised to sell at!

If overall demand for a product rose, and we were looking at a product where new firms could not enter instantaneously, then this would lead to an increase in the market price – which would then be charged by our little competitive firms. They would earn supernormal profits which should, in time, lead to entry by other firms – this is what drives down the price again (if demand remains high). If there is uncertainty about future demand, then that acts as a additional cost for entry – which implies that higher demand may be met with higher profits in the case of perfect competition.

For a variety of market structures and levels of competition, higher demand would be expected to lead to higher prices and profits – the puzzle often was that, in the case of firms with market power, this was not the case! Instead, we would see their tacit collusion break down, leading to countercyclical margins and less price variability in situations with large oligopolistic firms.

So in other words, we do not need market power to get price and profit change when we have an increase in demand in the economy (relative to productive capacity) – and imperfect competition can actually reduce the relevance of this.

Now, in the current situation we have both significant fiscal spending (government demand) extremely low interest rates and a movement out of lockdown bring consumer spending into the current period (private demand) and disrupted supply chains for goods making the durable items and petrol that people are trying to buy more scarce.

In that situation, it would be good for people to delay purchases a bit – implying higher interest rates, and high prices (relative to future prices) serve that purpose.

But if they just didn’t lift prices there wouldn’t be inflation

No if prices never changed we would never have measured inflation – this also implies wages would never change as well mind.

But what would then happen is that when there is excessive demand the number of products would need to be rationed in some other way – lines, black market activity, empty shelves. Suddenly people that very much value a product would not find that it costs more – they would find that they can’t even buy it.

When demand is insufficient these fixed prices would imply that firms would see their stock building up, and without the ability to cut prices to clear stock they will simply produce much less – implying that larger layoffs and business failures would occur.

This is not to say that the current increase in demand may not propagate through prices in the way firms with market power behave. A clearly communicated “shock” that gives a firm the ability to wink and nod at other firms that it will “lift prices” may allow firms to collude, leading to price increases that would not have been possible with competition. This is the tacit collusion that we chatted about in the prior post, and a million other times here. And the empirical evidence tends to show that this does not occur usually during period of high demand.

And what about changes in relative prices – supply chain disruption is far from even across industry and product types, and so prices need to change to represent that scarcity. If there is less fuel available we want the price of fuel to be higher, so that those with a lower use value of that fuel self ration. Knowing that certain individuals may be in a vulnerable position to changes in fuel prices we may act to support their incomes, but not blunt that price signal.

Now monetary policy does aim to reduce the variability in prices – but it is doing so by reducing the variability in demand, not by telling prices to stay put.

Conclusion

Blaming the current increase in the price level, and the spectre of future inflation, on the greed of someone powerful achieves two things – it makes it a morality play, and it means that we think we can punish the “bad dudes” in order to solve the problem. But these things are not true.

Making a popular boogey man might be good politics – but it doesn’t help the wellbeing of a nations citizens. As Chris Conlon says:

For those who don’t like video and just want to read the text, it can be found below.

[Gulnara]

On a recent trip to my beautician – link to her website below – I started negotiating the price of my visit. However, I quickly caught myself doing so and stopped. She understood where I was coming from, as she is also from the former Soviet Union, where such haggling is a normal part of daily life. But that isn’t the case in a country like New Zealand – which is why we both put a stop to it.

So why is haggling culture so different in different countries, and what are the economic consequences of this?

[Matt]

That is really interesting Gulnara. Such bargaining does depend on the expectations of consumers and producers – so bargaining cultures will tend to support individuals bargaining while societies that do not do that will make it costly.

This strategic complementarity implies that both societies with bargaining and those without are “equilibrium” outcomes – where people’s incentive is to do what everyone else is doing. We call these bargaining and non-bargaining equilibrium “states of the world”.

To evaluate these outcomes, we want to think more deeply about price setting and market structure within each of these states. Then we can posit ways to test this with data, and also think about how differences in the data between countries may be due to the acceptance of bargaining.

The two mechanisms we will focus on here are price discrimation and tacit collusion and price discovery.

Price discrimination

Retail stores tend to be monopolistically competitive – especially at the stage where you have already turned up at the store ready to purchase.

When you are at a store and ready to purchase you have three options: Don’t purchase, purchase at the ticket price, and haggling. In the face of haggling the store has its own incentive to haggle back – or to tell you to get bent.

The willingness to haggle on both the customer’s and the firm’s behalf depends on whether it is something they expect other people to do – it feels pretty stink to go and haggle just for the other person, and other customers, to look down their nose at you. However, this is more than just some concern about underlying social judgment – the act of haggling is something the firm would like to be prepared for, and the act of undertaking haggling puts pressure on these other customers to take on the cost of haggling themselves.

This can all be articulated through the concept of price discrimination.

Price discrimination is an interesting issue. A big reason why we viscerally feel uncomfortable with it is because it is discrimination – two people are being charged a different amount for exactly the same product! This seems fundamentally unfair.

In this haggling case, such discrimination doesn’t work by having a price and marking it up for some and down for others. Firms, in the face of bargaining, will increase the ticket price relative to a situation without bargaining. This will make it necessary for customers to negotiate simply to receive the price they would receive in the absence of such bargaining.

As a result, if you are not equipped to bargain, you end up paying higher prices – and if you aren’t able to negotiate much, this may be due to it being costly for you to negotiate, making the “real price” paid high.

However, there are those that benefit. Customers that are able to buy who wouldn’t have been able to at the non-price discrimination price, those with a low willingness to pay (or low cost for bargaining) will experience lower prices, and the business is able to increase their profits. Overall it might be more economically efficient, depending on how costly haggling is to individuals, but there may be distributional concerns.

If the industry is fully monopolistically competitive, low entry barriers will see the increase in business profits evaporate – so the increase in sales will lead to an increase in benefits to consumers on average, although at the cost of customers who have a high willingness to pay/low willingness to bargain. Furthermore, such entry may lead to excessive product variety as noted in Li and Shuai (2019) Monopolistic competition, price discrimination and welfare – ScienceDirect.

The mixture of price discrimination and search costs doesn’t just hold in the abstract. Bryne, Martin, and Nah (2019) (negotiation_v18.pdf (nyu.edu)) is a recent example of a field experiment testing out this behaviour and its implications. However, these implications and what we think about them does depend on the reason why “willingness to pay” is high and why “search costs” or “the cost of bargaining” may be high.

If it was just on the basis of individuals initial income, this may be quite redistributive – increasing provision of the product and the welfare of low income individuals. However, if it was due to the necessity of provision to meet minimum standards (i.e. health care expenses) such bargaining may be quite regressive.

Gulnara, you’ve actually experienced life with bargaining and life without – why don’t you tell us your thoughts.

[Gulnara]

Thanks Matt.

When I was a teenager I was still getting used to being able to shop for myself. At the time I didn’t really understand haggling, and as a result I found it quite exhausting.

I specifically remember going and purchasing sunglasses from a store in Baku, that I thought looked very cool.

I went home with them, and my mom asked me how much they cost – I told her and she inquired whether I had managed to get a discount. When I told her I just paid the ticket price, she laughed and took me back to the store, haggling with them for a discount to be paid back to me. The point of the lesson was to indicate that even if you were willing to pay for a given product, prices had been inflated – and so bargaining was expected.

As I got older, bargaining was active in certain situations – and it became more natural and less costly for me. Haggling with doctors for medical treatment and check-ups was extremely common, and once I left Azerbaijan to study in Italy, there were constant situations where bargaining was necessary – and expected – to live on my limited student budget.

Tacit collusion and price discovery

[Gulnara]

Now I’d like to change tack a little bit. Although bargaining may be a tool for price discrimination, it also influences the nature of competition in the market.

We recently talked about tacit collusion when chatting about Nurofen prices. Furthermore, an understanding of tacit collusion helps us to understand economic cycles and the recent discussion about price freezes – something we’ve blogged on.

What does this have to do with tacit collusion? Well when comparing the Rotemberg and Saloner model to the Green and Porter model we noted that a major issue was that of “information”. Can a firm tell whether their competitors are to blame for changing prices?

If, instead of monopolistic competition, we had firms that were oligopolistic then these strategic interactions become important for the general level of price setting.

Having bargaining, offers an “unobservable” way to cut or increase prices. As a result, your firm’s competitors may be able to observe the ticket price on what you sell – but they cannot observe the full complexity of how you will discount to attract customers.

This view of collusion and bargaining implies two things.

Firstly, with less information about the price set by the other firm, the Green and Porter model – where there are price wars in low demand states – becomes a more believable representation of price setting. As a result, pricing dynamics over the economic cycle may look quite different in countries with significant consumer bargaining.

Secondly, as it is harder to observe the other businesses’ prices and build up trust for collusion, it is more difficult for firms to collude! In countries where bargaining does not occur, firms can loudly commit to a certain level of prices, and thereby find ways to tacitly collude and keep prices higher.

As a result, profit margins and prices would be higher in countries where bargaining is culturally uncomfortable – countries like New Zealand, Australia, and the United Kingdom. These example countries are fairly well known for being “expensive” to live in – so consumer bargaining may be one possible explanation. However, this is an issue we are going to discuss more deeply another time.

Conclusion

To sum up, with price discrimation and tacit collusion, we’ve outlined two of the possible mechanisms that may differentiate market outcomes in countries with active market bargaining and those without. Both of these arguments appeared to show bargaining in a favourable light – however, they also did point to trade-offs that may reverse this, namely the cost of bargaining, the proliferation of excess product variety, and broader related distributional consequences.

However, there are other possible arguments that can come to mind. If you have some alternatives of your own, why don’t you pop them down in the comments for us all to discuss!

Thanks for watching and we’ll see you next time.

]]>For those who aren’t keen on listening to videos, I’ve popped the transcript just below

Cheaper medication in winter

[Gulnara]

I’ve been doing a bit of online shopping. As part of this, I’ve been struggling to figure out what I should stock up on before the next COVID variant hits.

When looking at the price of Nurofen I noticed that there were only a few specials among the varying brands, and the overall discounts were quite small compared to the deals I’m used to seeing during winter.

[Matt]

Good point Gulnara, this is an observation I’ve made in the past, implying that this isn’t just due to current circumstances.

However, this feels a bit weird – why would cold and flu medication be cheaper in winter than it is in summer? Let’s formalise why this feels weird, and then see if we can provide an explanation.

Demand and price

[Matt]

To formalise our intuition – and start trying to work out why the observed data looks so different – it is useful to build a model. And the best model to start with is our friend supply and demand.

In our discussion of income and price effects we mentioned the idea of a demand curve.

[Show prezi]

This demand curve tells us that quantity that will be demanded by consumers at different prices.

Here we are looking at the market demand curve for cold and flu medication. As we move down and to the right of the demand curve, additional consumers become willing to buy a product – or existing consumers are willing to buy more. At each price that additional purchase refers to our marginal customer.

Start with the situation where no provider of cold and flu medication is large enough to influence the price with its decision to produce. In that case we get a market supply curve that represents the marginal cost of production of cold and flu medication.

This marginal cost is shown as increasing in the quantity supplied – why? Well the more that is sold, the more storage and shelf space is required, the more need their may be for staff to work overtime, and the more risk there is that the machines creating and packing the medication will break down. The more “scalable” the process is the flatter this curve is likely to be – but the limitations of storage and shelf-space – what are called capacity constraints – point to an increasing opportunity cost from selling more, which makes this type of curve believable.

As it is a competitive market, the price is set where marginal cost equals the price the marginal customer is willing to pay, which is where the supply and demand curves intersect. Even if competition breaks down somewhat (i.e. monopoly or monopolistic competition) the argument given here still holds – so it isn’t too extreme an assumption.

Cool, so what?

Well we want to think about what “summer” and “winter” are here? Imagine a world where you only buy cold and flu medication when you are sick – this would be the same world I live in. Well, I tend to get a cold or flu much more often in winter than summer.

As a result, at a given price I would buy more cold and flu medication in winter than in summer. We can represent that with a demand curve that shifts to the right in winter.

The names for this are “high demand” and “low demand” states – where winter is a high demand state and summer is a low demand state. A high demand state leads to the demand curve shifting right – as for a given price the quantity demanded is higher.

Now here the new market price will be higher due to the demand curve shifting right. This matches our intuition, but not our data!

Gulnara, what is going on?

[Gulnara]

Good question Matt. To my mind there are six different arguments against this logic. Let me tell you about five of them, and save the last one as a treat for later.

Firstly, COVID has changed things – and so even though it is summer perhaps it is a high demand time.

Secondly, perhaps cold and flu medication is a durable good so prices do not change much over the year as lower prices eat into future demand.

Thirdly, we may have confused average and marginal benefit in this discussion – it may be that the willingness to pay of the marginal consumer is higher in summer than in winter, perhaps because the weather is better so people want to push away the symptoms in order to enjoy the outdoors. More broadly, summer time customers may be “less sensitive” to price than winter customers.

Fourth (and related to the third), as demand for medication is higher in winter, supermarkets may use it as a loss-leader to attract customers to buy other products.

Finally, such products are produced at scale and so the average cost of production is higher during summer.

Each of these five arguments are good, but have a fatal flaw.

The first of these arguments may be true of this year, but as this is an observation Matt’s made repeatedly over his long life, I don’t think it quite covers this.

The second argument would make sense if the price never changes. And the ticket price itself is fixed for these products, so that sounds good. However, it appears that the discount price is lower in winter than in summer.

[show prezi 2]

The third argument is neat, and when combined with imperfect competition it is very compelling, but from personal introspection I don’t know if I’m convinced. Irrespective of the weather I have a given sickness threshold where I will have medication. This may well be part of the pricing behaviour, but we’re going to move on and look for something else for now.

The fourth argument is quite attractive in some sense, but there is something unintuitive about imagining supermarkets cutting prices when demand for things are high in order to try to sell other products – there needs to be something else here, either about the elasticity of demand as discussed above, the cross-elasticity of demand, or with regards to competition as we will touch on below.

The final argument sounds compelling, however the focus on average cost is misleading. The “costs of scale” are fixed costs that must be met irrespective of the amount produced, and as a result it is the marginal cost in the short term – which will either be flat or rising with output – that should determine price.

Getting a bit fancier

[Matt]

Moving away from pure ECON101 we might also note that there isn’t necessarily a competitive provision of cold and flu medication in New Zealand. We only have two supermarket chains which face weak competition from pharmacies for these products due to halo effects.

Halo effects are the idea that if a firm is offering one product people are willing to buy, then people will be more willing to buy other products there – either due to decreased costs of searching as things are all in one place, or because people trust this business to provide a good product.

Supermarkets bundle a lot of goods and services together and so these halo effects are important for understanding the pricing behaviour of these types of firms.

Furthermore, we can look further up the supply chain in New Zealand to see there are a limited number of cold and flu medication brands on the market – as a result, even if supermarkets were competitive, there may be market power in the provision of these products to supermarkets which would lead to changes in the final price to consumers.

Green and Porter 1984 indicates what we may intuitively expect when an oligopoly exists in a market.

If the firms in the industry follow their own incentives to maximise profit they will compete and drive down the price – leading to all of the firms achieving lower profits. This is a traditional prisoner’s dilemma.

[Prezi 3]

As a result, if the firms could collude to keep prices higher and act “like a monopoly” they could all be better off – since a monopoly sets prices in the market at the point that maximises industry profit.

The tension here is that each individual firm has an incentive to undercut their competitor a little bit, as the lower price allows them to steal some customers from their competitor and thereby increase their own profits – albeit at the cost of the profits of their competitor.

The question here is how might collusion breakdown if demand conditions change?

Green and Porter 1984 take a situation where the firms are colluding in a high demand state, and then the economy switches to a low demand state – for example the movement from winter to summer.

[Prezi 4]

If an individual firm sees demand for their product drop there could be two drivers: Firstly, general demand for the product may have declined. Secondly, their competitor may have betrayed them and cut prices – thereby stealing some of the individual firm’s demand!

If the firm is uncertain about what the cause of the drop in demand is, then they believe that there is some chance they have been betrayed. In order to signal that they will “punish firms that renege on the collusive agreement”, our firm will have the incentive to cut prices.

The willingness to increasingly compete in low demand states is needed to ensure that collusion is maintained in the high demand states – by showing to everyone else that the business is serious about punishing firms that defect.

So our intuition and these models all indicate that cold and flu medication prices should fall in summer and rise in winter – which is the opposite of the result we find. So, Gulnara help me out here – why could this be?

Information

[Gulnara]

This brings us to our sixth argument – tacit collusion and the temptation to cut prices.

Winter and summer are known quantities – we have them in our calendar, and although we don’t know the weather perfectly we have a good idea of what we will be doing during both.

In this way, a large portion of the difference in demand between seasons will be known. Furthermore, the actual price set by the other firm is observed – it is on the same supermarket shelf, on the website, and in the flyer! So it would be perfectly observable if competitors were cheating.

When the oligopolists have knowledge of what the other is up to, we get quite a different problem. Something that Rotemberg and Saloner 1986 discuss.

In this model a high demand state increases the “temptation” to betray your competitors to try to steal the entire market. Because of this, it becomes difficult to sustain collusion and collusive agreements will break down.

In our example this means that, during winter, there is a surge in demand for purchasing cold and flu medication. If our medication providers were able to maintain collusion, they would experience a big increase in profits, but the expected benefit from cutting prices (whether your competitor does or not) is now much higher. As a result, they cut prices and we get some sweet discounts.

Now you might say this sounds dumb – just don’t cut prices! But the key thing here is that all of the firms are responding to the change in demand conditions – not each other’s actions. If one firm does not cut prices, it is attractive for the other firm to cut prices. If that firm did cut prices, it is still the best response of other firms to cut their prices. Cutting prices is a dominant strategy!

In the oligopolistic setting all firms have this incentive when colluding – however, it is how the “benefit to defecting” compares to the “benefit of maintaining collusion” when a high demand state occurs that drives the result. Essentially, the arrival of the high demand state has increased the benefit to defecting while keeping the benefit of maintaining collusion (which are expected future profits) unchanged.

Although this sounds like a good explanation it has one issue – the high demand state is supposed to be unanticipated (as demand is modelled as a stochastic process). However, winter and summer are known!

Why does this matter? If the timing of the high demand state was known, and the oligopolists knew defection would occur in the high demand state, then there would be an incentive to deviate prior to this – changing the timing related to prices, and potentially unravelling collusion overall.

To rescue this model we would need to ask if there is some uncertainty about demand – and there is. The cold and flu season starts, ends, and peaks at different dates each year: Flu Season | CDC – here medication sellers will know when the high demand state has started, but there is some uncertainty about when it will start before the fact.

We’ve only noticed the strongly discounted prices when I’ve had a cold, which has been once this season has kicked off – as a result, it could be this form of “high competition during high demand states” that is driving the surprising result of lower prices for cold and flu medication in winter.

Conclusion

[Matt]

Although ECON101 supply and demand are powerful tools – they don’t tell us everything. The counterintuitive behaviour of prices tells us that sometimes we need to dig a bit deeper to understand what is going on – in terms of the cost of production, market structure, and structure of consumer demand.

Contrary to a lot of what you read on the internet, supply and demand is useful and powerful – but we just need to be honest that circumstances can be complex. As a result, keeping an open mind and always disciplining ourselves against the observed data is necessary for doing good economics.

If you are interested in thinking about this a bit more I did a quick google search after writing this script and found some nifty resources – they will be attached below. I’ll also add a few blog posts Gulnara and myself have worked on that chat about similar circumstances.

Peak-Season Discount Case – Economics – Reed College

Demand, Information, and Competition: Why do Food Prices Fall at Seasonal Demand Peaks? on JSTOR

]]>After recent discussions about “negative interest rates” across Australasia I thought it would be useful to talk about how these rates appear mechanically at a high level (in terms of financial system operations).

In class (and Gulnara’s posts here) the motivation of why negative interest rates might be appropriate in a policy sense was raised. Furthermore, she did a great job of noting that it is unlikely that negative rates will cause additional savings (as some have claimed) and so theoretically we can continue to think about our investment model with negative interest rates.

For this post we will assume that the central bank is trying to influence interest rates towards a level that will “close the output gap” or “push Y to its sustainable level” and achieve their inflation target, and it just happens that this interest rate is negative.

The wrinkle is that we achieve this negative interest rate through a settlement cash mechanism – so we need to ask, how do negative rates in settlement cash accounts translate into lending and actual interest rates?

Negative rates and settlement cash

Let’s take our example from before and assume that the OCR is cut by 400 basis points to -2%. In this case the borrowing financial institution will “pay” -1.75% and the depositing financial institution “receives” -2.25%.

Why would an institution deposit funds in an account to earn -2.25%? Why would financial institutions not just ramp up their borrowing at -1.75%?

The reason for that intuition we feel is that we are thinking about money – money yields a nominal interest rate of 0%. If the banks could just independently hold money at 0% they would borrow endlessly at -1.75% and would never save at -2.25%.

However, the settlement cash account is designed to include cash holdings for banks. So if a bank borrows a dollar from settlement cash and tries to hold it as a cash asset, it returns as a deposit in the settlement cash account. So in this way the system cannot be escaped.

What about interbank lending? One bank could lend to another bank at 0% and this would be a better return for the lender than -2.25%. But that bank who is borrowing is paying 0% instead of -1.75% is actually worse off. As a result, the interbank market will reinforce this dynamic as long as the settlement cash account is determining the opportunity cost of marginal lending.

Given the banks cannot avoid these negative rates in settlement cash accounts, they would then be expected to pass these on to both their depositors and borrowers (in order to achieve the same interest margin) through lower/negative interest rates!

However, they haven’t been. Deposit rates refuse to budge below zero in countries with negative cash rates, and although banks are accepting lower margins they have also reduced lending rates by less than they would have otherwise.

In this situation, there are two ways that banks can turn around and try to avoid these negative rates – and therefore avoid passing on negative rates to depositors and lenders:

- Investing in instruments that are zero yielding that don’t get captured in settlement cash (eg overpaying tax – e.g. Sweden). We need to be careful here not to include assets that have an expected negative capital gain (as that equates to a negative yield – such as gold).

- More carefully ensuring that deposits and loans match on a day-to-day basis.

Both of these have one thing in common – banks are willing to slow down their matching of lending and borrowing, and accept lower liquidity, in order to avoid the cost associated with negative interest rates.

If this is the case, then when rates become negative enough (when they aren’t just representing a small service fee) financial institutions may respond to negative interest rates by being more careful to match their deposits and lending on a day-to-day basis. Suddenly when you want a loan or to deposit funds the bank will start saying “you meet our criterion, but we have a waiting line for approving loans/deposits and it will occur when you come to the front of that line”.

This would reduce the volatility of money and in turn restrict economic activity. This is a mechanism that may lead to negative interest rates reducing growth – if the negative interest rates also involve an increase in non-interest restrictions to lending.

But a negative cash rate pays people to lend!

Good point and very consistent with what we’ve done in class. As a result, this discussion requires further explanation.

When cash rates are negative it is true that a financial institution will now be willing to lend at a lower interest rate (given that they can “borrow” from settlement cash at a more attractive rate), so at face value there is no reason to think such negative rates will restrict lending.

But we also need to remember that the borrowing also credits a banks account. If the person being lent to then deposits the funds in another banks account that other bank will be a bit unhappy about having to pay the negative interest rate on it – and if the person immediately spends it those funds will be deposited.

As a result, banks will want to restrict deposits. In so far as a bank restricts credit being paid into their account, they can create an issue for loans – which in turn could restrict how quickly loans could take place.

When interest rates are positive you have same issue from lender, but with negative it is the deposit taker that pulls back. With positive interest rates, lenders are increasingly unwilling to lend as rates go up (due to the uncertain cost of mismatch), with negative rates the deposit taker becomes unwilling to accept funds as rates go down – both break down intermediation, but with positive rates that is the goal – with negative it is not.

Furthermore, even if the loan came back to the same bank as a deposit if the zero lower bound on deposit rates is binding (which it seems to be – with deposits rates in countries with negative cash rates staying at zero) for financial institutions then charging lower interest rates on investment will simply reduce the net interest margin of banks. With negative spillovers from uncoordinated lending in this sense, tacit collusion between banks might see them agree to cut lending to support margins – making negative rates at best useless and and worst a device that leads to uncompetitive behaviour.

Overall, thinking about how cash rates translate into negative interest rates – and the broader concerns in Eggertson etal 2018 – indicates that negative interest rates may not be as useful as our models in class suggest, where all that mattered was the investment function and the related impulse to investment this suggested.

However, this is an area economists are still trying to understand using data – so hopefully in the future we will have a better idea of what elements are relatively more important!

The main reason for discussing this is to show that, although our models in class are useful – they are not always the whole story. And given unique circumstances it is important to think about other margins that matter. Remember the Joan Robinson quote from the start of the semester – we are learning how to question things, not incontrovertible facts.

]]>On the face of it this sounds pretty simple – if prices change often then there doesn’t seem to be much scope for them to be sticky. But when we think about it a bit more this isn’t true – and thinking about why it isn’t true can give us useful insights into the macroeconomy.

Heterogeneous price behaviours

The recent interview by Harvard economist Emi Nakamura on price dynamics, monetary policy, and this “scary moment in history”, inspired me to look at the issue of this post.

P.S. I recommend reading the interview , as I am sure everyone will discover something new from it.

Nakamura earned the John Bates Clark medal, awarded to the most promising economists under age 40. I’m a fan of Nakamura due to her clear way of articulating the economic ideas and concepts, without complexity and jargon. It’s a talent that I appreciate in economists.

Nakamura discusses how price behaviours are heterogeneous – namely that different sectors change their prices in different ways. For one sector , e.g. soft drinks companies constantly run sales on their products throughout the year, including tough periods suchs as the pandemic. However, for certain sectors ,e,g, restaurants and shops, price changes don’t occur much frequently, especially not during the COVID-19 shock.

We want to understand the reasons why prices are so reluctant to adjust given the shock in the economy.

Reasons why prices don’t change:

- Menu Costs: A menu cost is the catch-all term for all the different reasons why prices may stay fixed even when there is an incentive to change them. In other words, there is some cost of adjustment and this is termed a menu cost (eg a product with a RRP written on it or a menu that has prices on it will both have a cost associated with changing the packaging).

- Reputation element(cost) of increasing the prices: If activity picked up for a temporary reason there would be more customers trying to buy the product. The natural way of dealing with the excess demand for the firm would be to increase the prices. However, this may burn long-term bridges – existing clients may feel taken advantage of, hurting sales in the long-term. As a result, firms may keep prices fixed so maintain goodwill.

- Strategic elements: The interdependency between peoples choices can strongly influence how prices are set:

- These strategic complementarities between their prices mean that when faced by a shock firms may limit how much they want to change their price.

- Furthermore, in so far as there is a first-mover disadvantage due to the above reputation costs this can be even more of a concern.

- Finally, the game between firms can lead to tacit collusion which can strengthen or breakdown during the economic cycle. Let’s take an airline company as an example.

We can think about all three in terms of an example. Airlines normally compete in a form of oligopoly. The pricing is relatively non-fixed due to the use of online platforms. They compete with each other, so that they constantly change the prices to get a sudden gain in the market and to generate a brand and goodwill with customers.

However, the airlines recognise that this is a repeated game – and if they can work together on certain routes they can both earn a greater profit. As a result, they also have an incentive for tacit collusion – they do not announce collusion, but start setting prices with reference to each other in a way that boosts their profits.

In these situations the price of some goods, services, and factors of production may adjust while other don’t. That misallocation of prices then leads to a loss of efficiency and resources. This is not the end of the story though – these small misallocations can lead to larger macroeconomic costs, and once it propagates through the value chain the final decline in economic activity can be much larger than the small initial misallocations would suggest.

Flexible prices can still be rigid

These stories also help us recognise something else – price rigidity isn’t necessarily about the price not changing or being unable to change. It is about whether the specific price adjusts towards the “optimal” level quickly. This is why stickiness is a bit of a misleading work.

This can help explain why price stickiness is seen as key to Keynesianism, but the event that Keynes was explaining involved a sharp decline in nominal prices and wages – even though these prices fell the adjustment suffered from coordination failures and over a complex emergent macroeconomy this led to a significant drop in output.

Price stickiness of the form I am thinking about here was first discussed in The General Theory of Employment, Interest and Money, by John Maynard Keynes – but it relates to the debate between Ricardo and Malthus on the possibility of a general glut in the face of market pricing.

According to the Keynesian school, prices and wages are rigid as they don’t react to the shock in a way that would clear all product and factor markets (the optimal allocation of prices).

For instance, the price for Chanel bags go up every year by a certain amount. Even though prices are changing this is still an example of the price stickiness – as the change in the price is not occurring to clear the current market for Chanel bags. Many other drivers could be behind this, in my view it is fear of competitors’ entrance and the need to keep prices at a level buyers think is “fair” that restrains Chanel from a massive increase in prices in response to a temporary lift in demand. They have a reputation for increasing prices a certain amount each year, and any deviation of that strategy would have reputational consequences.

As a result, a study showing that firms often change their prices does not imply that price stickiness – and the misallocation this leads to – is not an issue. Instead it just tells us about the mechanisms that may cause the misallocation – if prices are constantly changing it is probably not menu costs that drive this misallocation, but instead the strategic interaction between firms or the timelines associated with their sales and production.

This can even imply that prices that are “more flexible” in terms of having fewer menu costs can actually create even more harmful misallocations due to these intertemporal and strategic concerns. As a result, policies that make it such that prices can move doesn’t imply that the markets will clear.

What this does tell us is that national economies are complicated – and a more sophisticated understanding of price setting behaviour shows us that the complex emergent nature of macroeconomic phenomena are hard to describe with our normal microeconomic tools. This is why macroeconomics takes the form it does – and why we need to be careful with the way we argue from aggregate values such as “goods and service prices” and “average wages”.

]]>According to the media, NZ shoppers have faced this as well.

“Some customers have taken to social media to complain that prices of items like soap, meat and fresh veggies have increased sharply.”

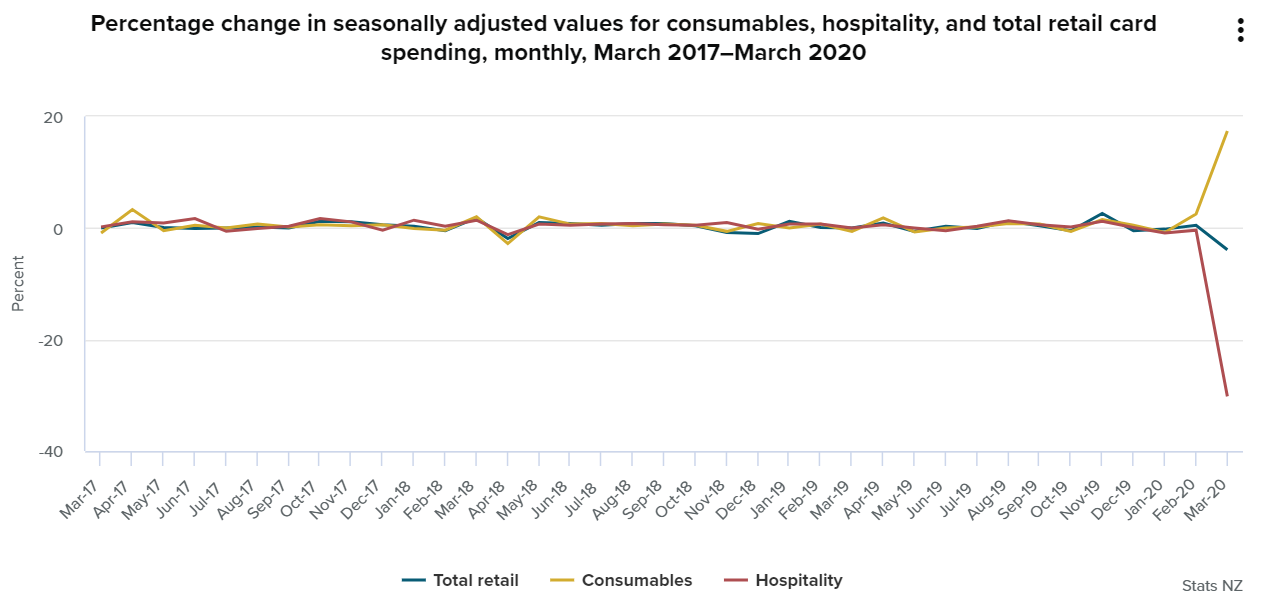

However, supermarkets kept denying the fact. It’s hard to judge the case from my experience, as Matt and I were lazy and were primarily eating outside before the lockdown. However, Stats NZ provides data here – so let’s look at the latest release on the Food price index to figure out whether the customers are right.

Spending on groceries

Before looking at this, let’s think about the what has happened. Fear around COVID and the quarantine by the end of March will have driven down demand for going out to restaurants, travelling, and going to movies – but driven up demand for groceries.

Why? People were keen to stock up in case they couldn’t get food, and as they aren’t eating out people now need to get more of their food from supermarkets (our case).

Stats NZ’s electronic card spending data indicates that this was indeed the case in March.

So we know that grocery store demand surged, so what does that mean for prices?

The food price index

Our initial economic intuition tells us, high demand in goods drives up prices as willingness to pay of consumers rises. This is reinforced by the fact that supermarkets were hitting their capacity constraints as noted by the comments around toilet paper.

But then this didn’t happen.

Stats NZ March food price index shows that grocery store food prices rose 0.2% in March relative to February when adjusted for seasonal variation.

The “real” figure is likely a bit larger, as supermarkets dialled back their “promotions” during the COVID crisis – and these deals are often not included in price statistics. Even so it looks like supermarkets haven’t increased prices in the face of rising demand, limited competition, and capacity constraints. Why??

Why haven’t supermarkets increased prices?

There are two clear categories for why they would not have increased price – the relationship between the price now and demand in the future, and imperfect competition.

For the first, the price supermarkets set now will influence demand for their store in the future. There are reputational effects from changing the price (goodwill) which are likely heightened during a pandemic, there are consumer expectations of prices which are anchored to the price now, and for franchise owners there is also the difficulty in getting them to coordinate prices with each other if you intend to significantly change the way products are priced.

In the current situation, supermarkets don’t want to get a reputation of not being kind – or of being price gougers – so will be sensitive to increasing the price.

The second is competition. If the two supermarkets were hypercompetitive and also had no market power over their wholesalers/suppliers then they would be forced to change prices with changes in supply and demand. But they haven’t. As a result, they could have market power in either of these markets.

On the sales side this could be a situation of tacit collusion. When demand is high supermarkets compete more to capture a share of the “high reward”, leading to a breakdown in tacit collusion that normally exists. Arguably, this idea is supported by the drop in grocery prices during December (Christmas).

Combining the concern about looking like bad people, and an increase in competition between supermarkets to get these new customers, it makes a lot of sense that they haven’t increased prices when faced with a surge in demand.

However, if demand remained higher forever, then these explanations suggest that eventually prices would rise – they only work because this is a temporary “high demand” or “high reputation cost” state. If restaurants are closed for a year expect to see more upward pressure on grocery prices.

This leads to some interesting thought experiments such as:

And yet, here I am in a big Wellington supermarket. It has:

- lots of toilet paper,

- specials on all the toilet paper!

This doesn’t seem to make sense. If concerns about COVID-19 are driving people to panic buy toilet paper we know that the demand curve has shifted right, and prices should have risen! So what is going on. Lets put our economics hats on and find out

Wellingtonian’s are different

Hey it could just be that Wellingtonian’s are different, and they realise that during a pandemic toilet paper isn’t a particularly high priority. Or maybe the constant earthquake awareness in the region means that everyone already stocks up on toilet paper.

In that case, if the supermarket has stocked up expecting a surge in demand they would be highly disappointed, and will have built up extra stock (as shown by the stacks of toilet paper all over the supermarket). In this case, the discounts are to clear out this extra stock.

Here there was an anticipated increase in demand, but it was smaller than expected – as a result toilet paper providers oversupplied and ended up discounting. A similar argument has been used for looking at Nurofen prices in winter here.

This seems like a reasonable reason – it involves people in Wellington being different and their local supermarkets not realising.

But I feel nervous acting like supermarkets are that dumb, and that people in Wellington are particularly special, so what else could explain this observation?

Competition, collusion, and an opportunity to sell toilet paper

New Zealand has only two supermarket chains. These supermarkets are the primary suppliers of toilet paper.

Given this duopoly we can think about supermarket competition as a Cournot game. In this instance, imagine the supermarkets were exactly the same. If a supermarket cuts prices to sell an extra unit of toilet paper this will reduce the revenue of the other supermarket – due to this spillover the supermarkets overproduce (relative to the monopoly level) and end up with less than half of the monopoly profits each.

This is a prisoners dilemma – if they could coordinate they could make half the monopoly profits each, but they each have an incentive to deviate from this, and so compete themselves into a position with lower profits.

Now supermarket competition is repeated through time, and so there is some degree of tacit collusion between the retailers. They will generally both hold their prices up, in order to generate greater profits, even though they each have an incentive at a given point in time to undercut their rival.

In the current situation we have an observed increase in demand for toilet paper. In this high demand state we have greater profit opportunities if you can be the retailer serving the market!

Because of this, there is a large reward for undercutting your rivals. This greater reward during the high demand state may be so tempting that tacit collusion collapses, and the supermarkets start competing with each other!

As a result, even though demand for toilet paper has increased the fact that both supermarket chains are trying to benefit from this ends up driving down prices as collusion over toilet paper prices collapses!

This was another explanation given for Nurofen prices dropping during winter here.

An issue with this explanation is the observed oversupply of toilet paper in the supermarket – they have cut prices to sell more, and yet the shelves are stocked to the brim!

It could be that supermarkets are trying to keep a large stock of toilet paper in case their competitor does not respond – and as both supermarkets are cutting prices they end up oversupplying toilet paper.

However, I think that – in this instance – there is a better explanation.

Complements and halos: Loss leading loo paper

Toilet paper is in the news. Get to the supermarket, wrestle your neighbors for toilet paper, and you will be safe from COVID-19. It’s a bit ridiculous – but the availability and price of toilet paper is an important heuristic right now for what location to shop in.

Supermarkets do not sell just one good. As a result, if a special on toilet paper – along with stacks and stacks of toilet paper from wall to wall in the store – will get people in the door, then that also ensures that people will buy OTHER goods and services from the supermarket.

In other words, toilet paper and other supermarket goods are complements, and the discounts and advertising of toilet paper is a way supermarkets can get you in the door to purchase these other goods.

This broad concept has a common name called the “Halo effect“. However, as that post notes this effect is quite unclear as it is the mix of two things, the complementarity of products due to their co-location, and brand spillovers.

In this instance it is just the former we are meaning. In fact there is a better term in this context, where the supermarket may be willing to sell toilet paper at a loss to get people in the door – a loss leader.

Because of the fear of COVID-19, people are trying to find something they can control to give themselves a sense of protection – in this case toilet paper purchases.

Seeing this, supermarkets recognise that people are especially responsive to toilet paper availability and prices and so use these sales to increase demand for their other – higher margin – products.

Just look at these places overseas:

Mate, those places are loaded up with toilet paper!

So maybe Wellingtonians aren’t that special, and supermarkets just realise that showing us toilet paper gets us in the door during a crisis. Well played

So it is Christmas. How about this year I don’t:

- Make the case for why we should give cash instead of gift.

- Warn about not undertaking time inconsistent behaviour on Christmas day.

Honestly, I used to do the same thing every year.

My way of precommiting to that was to time this post to go up on … Boxing Day! The presents are given, the inappropriate behaviour is done, and now we are ready to go shopping.

But those big sales back when I worked in retail appear to be largely gone. Why?

Why was there a sale?

Back in the day I worked on checkout at the Warehouse, it was great times with great people. So what was the commonly known motivation for Boxing day sales?

It started with overstocking. In the lead up to Christmas a retailer will make a large amount of their profit for the year (specifically based on higher margins), however there is significant uncertainty about what they will sell. As a result, retailers would build up extra stock to make sure they could sell the higher margin products at that time – but that would leave them with stock that just didn’t sell.

As a result, Boxing day was about clearing out that stock – usually at close to cost.

However, then consumers knew there would be a sale on Boxing day. Because they expected a sale, there would be a large number of customers available on the day – in other words, expectations of a good deal leads to consumers being in the location.

As consumers have appeared at the store they have taken on the cost of going to the shops and are looking to shop.

When I was working I very much saw this coming into place as I worked. Suddenly retailers were not just “building up stock” of products that didn’t sell, they would ensure they had extra stock of EVERYTHING to sell on Boxing Day.

With lots of customers available in the shopping area, and a lot of competing firms about, part of the story became about trying to get the customers to come shop at your store – rather than your competitors. As a result, big sales were taking place on popular items in order to get the pool of customers to shop with us!

Where has the sale gone?

So Boxing day is just a day out with lots of advertising nowadays – I hardly ever see a good deal anymore. So what has happened?

This reminds me of models of tacit collusion.

Essentially, high competition had given us a Rotemberg and Soloner style competition for consumers. The “large pie” associated with the huge number of consumers wandering around looking to shop offered a tempting reason to try to undercut competitors – generating a price war.

However, in this style of game there is the possibility for retailers to all improve their profitability by agreeing not to fight. Yes the “reward” for fighting is greater with high demand, but given the prisoner’s dilemma that involves an agreement would make the oligopolistic retailers better off.

And as a result, it appears that is what has happened. Boxing Day sales are not longer the event they used to be.

Will this change?

Tacit collusion is sensitive.

The reduction in Boxing Day sales happened after the recovery from the Global Financial Crisis. In that way, the reward for undercutting your rivals has been lower than it was previously – as consumers may be more averse to spending.

If that is the driver, then one day the sales might be back.

However, it could be that the nature of products have changed. As noted here an increasing number of durable products are being replaced by services. The big Boxing Day sales often involved cheap overstock durable products that were sucking up space. If underlying demand for these has gone away, the Boxing Day sale itself may be gone.

Anyway, I’m off to go shopping – Merry Christmas all you beautiful people, and economists!

]]>