My answer is “no idea” – I just wanted to use the same title as the Australian Budget post. You yell inflation at me and I say “monetary policy offset through higher interest rates” – and the monetary and fiscal authorities can argue about that. New Zealand based economists can describe that for us.

Instead I’m going to have a think about a couple of the policies: game subsidies and the higher top tax rate.

I also see that they are ramming from the Tax Principles Act. I’ll save thoughts on that for its own post later on.

Are they making my Steam games cheaper?

That would be nice – not particularly fair, and definitely not an efficient use of funds – but at least it would benefit more than 1-2 people.

Instead they are doing the film subsidy rort for game companies now.

Rant on – if you don’t like rants skip

So for context New Zealand currently wastes about $200m pa putting that little “supported by NZ” logo at the end of credits on a variety of movies and television shows.

No that isn’t fair, they also support Weta’s well known culture of sexual harrasment and general toxic work culture – you aren’t really from Wellington unless you personally know someone that has been sexually or verbally harassed by senior staff at Weta.

They also make sure Peter Jackson has enough money to influence local council elections and make sure that nothing gets built in Wellington – while the city slowly collapses into a slum. And lets not forget that it also gives politicians the chance to go to movie premiers and maybe get a photo with someone famous!

The fact that New Zealanders are not publicly disgusted at film subsidies, and the corrosive impact they have on Welllington particularly has long frustrated me – and now with lights falling out of the sky, water mains bursting on a daily basis, the central city smelling of sewage, half the buildings still unfit for use (red zoned) since 2016, house prices out of control due to the lack of historic building, and the recent tragedy with fire, you’d think making the capital livable again would be the priority.

Instead, lets also give money to game developers, so they can lobby for their old neighbourhood to never have new building or infrastructure.

And then former Green MPs have the temerity to pretend there is justice in this – I guess the catch phrase of “green growth” just means making sure the green is going to whatever favours them.

Man, honestly screw you (not Economissive – he’s good people calling this trash out).

I’ve never liked the rort that is film subsidies. And Jacinda’s decision to keep them scaling up was a huge disappointment. But the fact this exists alongside the utter degredation of the infrastructure in my old home of “Wellywood” – especially in the last five years – should make a lot of people as angry as I am.

Rant off

Now that is off my chest – and if anyone is insulted by it please contact me in person so I can double-down – lets pretend you like the game subsidy and you are not a corrupt lobbyist. Instead you believe that there is good potential for New Zealand to compete with the world in “weightlesss” technologies – and with a bit of support, we can build an industry together! [dynamic comparative advantage]

If that is you, then the barbs were definitely not at you – I like you, and I like the way you’re thinking about things.

First off I’d warn you to ignore any “economic impact assessments” that come out – anything with that name ain’t a real assessment, and will make up a bunch of benefits and not mention costs. Lets instead think about the nature of this seed funding:

- A gaming company will take on staff that have certain skills, around coding and creative designs.

- It will combine those staff and some underlying capital to produce games.

- The gaming industry is risky – but if they have a good idea there is a chance of making a good return. This return is shared in earnings and wages between the capital owners and the workers.

- If things go south that’s pretty tough – the capital owner loses that, and the employees need to find more work.

If the gaming company doesn’t happen, people are in other jobs and the “capital” is allocated to other uses. The fact something is made doesn’t mean there is “net value”.

If people privately decided not to do this, but then did with a subsidy, it is either because they were incentivised to take on a risk they wouldn’t otherwise – or they are being shifted to a lower value activity.

You might say STOP, I’VE GOT YOU – imagine we have an industry with valuable skills that are transferable between firms, but each potential firm faces a lot of risk, in that case we may have a coordination failure where no firms move into that industry and invest … but if they did, value added!

Ok nice – that was a much stronger argument than I expected.

But why is this gaming in particular? Why doesn’t the government generally offer a scheme where they “co-own” firms – providing beneficial arrangements on failure, but taking a cut when there is success! You know, like a limited liability bankruptcy regmine with a corporate tax system.

…. Wait. Are you telling me we could just change those settings, rather than picking our friends and giving them handouts!

Specifically picking gaming companies, and giving them support, instead of articulating and understanding a general argument about the insurance and support settings in a country is dumb. New Zealand was unique in how well this was understood by politicians – but modern politics in New Zealand appears to involve a series of people who think they are the smartest person in a room, but only experience it when they’re alone.

Trust taxes at 39%

Ahhh, glad to see this change! The gap between the top income tax rate and the trust rate is problematic – see here – so this makes those settings more sustainable and undermines a bunch of potential tax planning.

What’s the planning? Well previously the trust rate was 33%, but if you earn over $180,000 the top tax rate is 39%. So say you have your own business and you earn $400,000. You could pay yourself $180,000 and have the extra $220,000 distributed to a trust. That $220,000 gets taxed at 33% (instead of 39%) and then the following year you just send yourself that money without additional tax – noice.

Now IRD has fancy rules to try to avoid really bad examples of this, but it is hard to avoid subtle avoidance – even with the new trust information collection rules. So increasing that rate is a surefire way to sort things out!

However, one thing that gets a bit mixed is some thinking that “trust income is always avoidance”. Hold up mate, one of the issues with bumping the rate up to 39% is that some people will now be taxed at a rate higher than they would if it was classed as their income!

Imagine you have zero personal earnings, but your trust earns $14,000. You don’t really pay much attention, and you live meekly in your own cottage eating leeks that you grow for yourself. Nice.

If the $14,000 was taked as your income you’d pay a tax rate of 10.5% on it. If it is trust income, you pay 39%.

As a result, you’ll get some unattentive people who are genuinely using it as a shelter who pay more tax.

What is the solution here? Well you could treat trust income like company income – so the tax is a withholding tax, and when the income is paid to the person imputation credits are attached.

Problem solved!

Well, remember our mate before – they are pretty inattentive. Reporting everything as if it is company tax is quite involved – that might be a bit much to ask them to do. We could get around that by setting an income deminimus … except the issue only exists for those with lower income.

These are issues that are too hard for someone like me – so I’ll leave that to the experts and just say this was interesting to see!

]]>I’m a trained economist. And I’ve been working in government in New Zealand fairly recently, and am now actively employed in the private sector. So do I have juicy gossip?

No, not at all. I do have a perspective however that isn’t just about some arbitrary lack of hiring “well trained economists” – lets have a chat.

Tl;dr

For those who don’t want to read me go on a meandering journey the cliff notes are:

- Bureaucracies respond to incentives – based on funds available and the type of advice demanded. So we can only understand this based on demand.

- Ministers and public commentary determine what the demand will be.

- Ministers need to appreciate these trade-offs are complicated, and invest in properly understanding them prior to making decisions, instead of rushing policy through.

- Public “thought leaders” spend too much time talking about vision and too little time pointing out the trade-offs. This is where the true “economists”, which are about informing rather than telling us all what policy to pick, are MIA.

- So instead of attacking the middle-person, subject matter experts need to get out there and communicate what is missing from policy debates – while Ministers and their offices need to learn some humility about what they know, and what it requires to generate knowledge about the true consequences of policy.

Tell us about yourself and policy

No. I’m sure if you use google you’ll figure out where I was working, and I had plenty of opportunity to work with analysts across government on economics issues – and I worked with a lot of insanely thoughtful, intelligent, and passionate people. If you find out where I worked, note that I hold these people in high regard.

Furthermore, when it comes to doing policy, describing trade-offs, and understanding the specialist nature of the subjects we were discussing there was no way I would have thought having significant economics training alone was sufficient. When I was working in this space I was constantly learning from other non-economists, and simply having more economists around itself would not have improved that – I’m not the flashiest economist in the world, but it isn’t necessarily a lack of economists that is the constraining factor on the advice.

Yeah, in broader government there were and are people who say dumb things about economics and try to discredit objective analysis across government – those are called human beings, and that has always happened and always will. However, the language of economics is still seen as a good and transparent way of describing issues.

And if you are one of the bureaucrats that doesn’t believe economics is needed to give policy advice, and likes to say dumb things about economics (i.e. suggesting we don’t look at economic research as its all discredited) – you don’t come off as a free thinker, you come off as an arrogant idiot who wants to fit into “fashionable circles”. Either grow up and learn to give policy advice that clearly identifies trade-offs, and so is self-aware enough to see if the policy choice hurts people, or get the hell out of policy and find a job where you won’t hurt people anymore.

Anyway I digress, what is the role of a bureaucracy? Operationalising and administering policy and acting as an active policy Wikipedia service to Ministers to help them understand trade-offs. For the later a core amount of economic knowledge is required, and most large agencies have a team that has some economics training to do this – and a research or analytics unit that provides further insights.

By its nature such work is almost always reactive in a small open economy, as we lack scale. It is impossible to analyse the trade-offs from every possible policy. As a result, what is being discussed in public and what is raised by stakeholders in consultation (including a Minister) will constitute issues to focus on. Things get more complicated sure, but this is the gist.

Demand for advice

So the concern appears to be that advice is done too quickly, and by people with insufficient training – leading to cherry picking of research, missed trade-offs, and ultimately policy advice being given that’s inconsistent. I of course can’t speak to that given the impeccable nature of anything that I was involved in  – more seriously though, lets think about this.

– more seriously though, lets think about this.

The advice provided will depend on the resourcing available and the underlying demand for advice. During COVID pretty much every bureaucrat I know worked around the clock under ridiculous time pressure – not just because of COVID but because of demands to provide advice on any transformational policy that was dreamed up. At the same time there are constant public complaints that there are too many analysts – with some ridiculous pipedream that somehow people will be able to produce more higher quality advice with less support.

The high quantity, low quality, public discourse in New Zealand when it comes to economic questions drives this. And when, to quote an unnamed journalist “we should write all economics as if it is being read by an 8 year old” the consequent quality of the public debate does not put genuine pressure on Ministers to demand higher quality advice and invest in it.

In this environment a highly trained economist is not the sort of resource that really works well – research economists are thoughtful, engaged, argumentative, and slow. I’d know, as I am one (even if the thoughtfulness is debatable).

So when the policy advice that is demanded is high level, cursory, and fast it is entirely consistent that bureaucracies will not be hiring “highly trained economists” – they will bloomin hire people that can get the work done.

If that is the nature of things, then having external trained economist available to hire in for detailed work can be a solution – and my understanding is that is often how these things work. But for this to happen you need to know who to bring in. And to find the resource to bring that in there has to be the underlying demand for it!

What’s the solution

Nothing will change unless, to be frank, Ministers become embarrassed by their own incoherent knee jerk policy settings.

Do Labour party Ministers and their office staff think policy setting by poll makes them seem like pragmatic world leaders? Do they expect establishing rushed poorly thought out policy will lead to their statue being placed outside parliament? Do they take pride in ignoring the trade-offs associated with their policy, and the way that unintended consequences usually fall on those most vulnerable in society?

I know this isn’t your intention – but by rushing the policy process this is exactly how it looks! In this way, for the vast majority of people in politics who are genuinely interested in outcomes, the important thing is this – policies have unintended outcomes, and a big part of the process is investing is spotting those to make sure we aren’t hurting people we don’t intend to. The reforms of the early 1990s are seen as bad now, but at the time the rushed nature of that advice was not pointing to the harms we can now see!

For the smalIer number that see politics as a game – stuff off. Rather than turning the sprinklers onto a policy problem and making it worse, recognise that making a genuine difference requires genuine investment in services, and in genuine data and policy infrastructure to make informed choices about the nature of these services.

Stats NZ is underfunded to the point of embarrassment. Compared to other countries we run our tax and welfare system on the smell of an oily rag. And the short-termism, and frankly undemocratic ramming through of policies under emergency legislation, undermines the quality and consistency of the policy framework in New Zealand – leading to a gradual erosion in people following the “intent” of legislation and the law, and eroding trust.

Of course, I don’t want to be overly harsh – it is clear that many Ministers do genuinely care about outcomes – but expertise matters, and trained economists are trained at describing these trade-offs. Demanding the same level of analysis overnight from an overworked and understaffed bureaucracy is a ministerial failure.

But if this is true, then it should make it easy for independent economists, at university and the private sector, to tear holes in advice right? So where is this?

The culpability of economist “thought leaders”

When a large number of “independent” economists and commentators appear to fawn over every “pragmatic” “strategic” “masterstroke” of a policy choice it is easy to buy into the hype. After all, if Archimedes can discover things in the bath then what is the issue of making policy in the same way.

Eric is a good fella who speaks truth to power – we need more Erics. But where are the New Zealand economists when it comes to communicating the economic science of trade-offs from policy choices?

Why do many of the consultancies feel so compelled sell us their “vision”, or to give government credit where none is due on the basis of vibes (although a shout out to my old buddies at Infometrics for being willing to call things out, and the NZ twitter economists who I also see keeping thing real).

Buddy, leave the vision stuff to politicians – they are better at it – can economists just inform us on trade-offs by explaining and quantifying unintended consequences!! Stop using the economist title to tell me you have a vision to increase productivity, improve housing, save the whales, and remove material poverty without any consequences – when you do this you are an advocate. There are always trade-offs, and what is constantly missing is the description of those.

I know if feels nice to show everyone that you can save the world with your great and grand vision, and gets you lots of attention – but if that is the game you want to play, stop calling it economics.

Now I don’t want to be overly harsh here, especially as I know I’d be the sort of person that would easy start doing the same thing (largely on poverty and inequality) – I recognise that this advocacy cares from caring about the issues, and caring about issues that do matter. But remember we all care about issues, and offering a compelling vision has it’s place. Most of the time what is missing is an economic description of trade-offs, not an impassioned advocate.

Framing it this way, I think it would be unfair to even criticise those who are publicly talking about economics now – they talk about trade-offs where they can, and play advocate on issues they care about.

Instead, where the hell are the real descriptive economists that can arm the rest of us with facts – and allow the rest of us to then debate what we value given the information they’ve provided.

We’re all allowed values and to care about things. But the economic expertise that is being discussed is in the ability to describe trade-offs from a policy choice – and surely an academic or industry economist who is focused on the market that is hit by the policy choice is best placed to communicate that.

Let’s be real. We don’t need people with the economist job title running around telling us what the “best policy” is – New Zealand is already massively overfilled with these people. We need people willing to apply the economic method to appropriate policy questions in order to understand trade-offs and inform policy makers and the public – with all the framework and data analytics based work that requires.

So you are blaming the private sector for public sector hiring

Only partially, the cavalier attitude of Ministers towards the time and effort required to give good advice is also very much to blame – but the lack of descriptive private sector commentators deserve more critique than they are currently getting. So I’ll do that here.

You may have noticed this concern in my recent posts – the only place with worse communication than the RBNZ at present is the business and economics media.

I’m from a different time, a time where consulting was about talking truth to power – when Gareth Morgan would call a spade a spade prior to his foray into cats and politics. I often disagreed, but the act of pointing out and unintended consequence and making people think about it was damned valuable. Discussion of a policy wasn’t based on who suggested it and how it fits within a horse race narrative of politics – it was instead a discussion of the merits, and costs, of the bloomin policy. And even when you didn’t agree with his conclusions, there was always a descriptive framework that allowed you to understand why – and why you might see things differently.

You might be cynical about my perspective as I’ve just said I’m in the private sector. I’d think the same, this sounds like branding. But I’m not working in New Zealand anymore, all my work is in Australia on Australian issues – so there is no benefit to me in discussing this. I just care about New Zealand a lot, and I want to see New Zealand be the best damned country it can be – protecting the vulnerable and while supporting voluntary exchange and positive community spirit.

This requires real transparent discussion of trade-offs from policy choices, and that has to start with open and honest discussion by people that understand these issues – the subject matter experts that are floating about outside of government. For many policy questions which require the government and public to make a choice knowing the trade-offs involved, economists do fill a key part of that.

So what is all of this saying – instead of slamming the bureaucracy for not hiring enough economists, maybe we need more subject matter experts (i.e. academic economists) taking an active role in explaining what is wrong when a discussion document is released. And to do that, we need Ministers to give genuine periods for consultation which would allow such people to build up their arguments. And a media that is willing to run with this type of expert communication.

Attacking a bureaucracy that is filled with capable people, but worked to their limit, without offering a solution doesn’t help – it infact misdescribes the issue, has a poor problem definition, and leads to incorrect conclusions, failing the very standards that people are being criticised for.

Economics is beautiful – if economists feel that the bureaucracy is underusing it then lets all get together and show them just how awesome it is at helping to describe policy issues, and how dangerous it is to do policy on rhetoric without an eye to unintended consequences.

]]>This is a book review for Thomas Piketty’s “Time for Socialism”. Gulnara got me this for Christmas. I have earlier reviewed Piketty’s magnum opus – Capital in the 21st Century – and will provide a link for that here (review, additional discussion).

Gulnara got me this book because she knew I’d find it interesting – and she also knew that my students are likely to ask me about it. Each year I will have students ask me if we should be communist, whether the profit motivate is immoral, and why we don’t teach the “obvious solutions” to the “clear problems in society”. Every year I appreciate these questions, and the opportunity to think through what these questions mean with the students. As a result, this video is in part my opportunity to prepare.

In the same way as when I chat with my students, the goal here is not to define what is right or wrong in a moral sense – just to look at the arguments at hand and push on them a little, to see where they may be delicate to different evidence or different value judgements. It is only by doing this that we can cut through a group’s rhetoric to have a conversation about what people truly care about. Furthermore, a lot of ground is covered in the book and here – so the discussion should be seen as cursory at best. More detailed discussion of specific issues is something we could do another time.

Gulnara’s section

As with Capital, Time for Socialism is a book that makes arguments that should be aired providing data to establish and support claims. Unlike Capital it is not a long comprehensive book – instead making Piketty’s arguments through five years of newspaper articles that he has written. Sadly this means the arguments are less comprehensively made, and so to make sure we are being fair we’ll have to be quite clear about what we think the argument is before throwing around any criticism.

Both Piketty and the Nolan’s over here are individuals that strongly believe in reducing the inequities in opportunities faced by individuals – and who see economics and justice as inextricably linked. Furthermore, we both believe in the importance of a democratic voice and entrenched rights to allow for this. But even with that framing I feel that we have taken the same goals and come to very different understandings of how this “should” be applied.

Back to Matt

Piketty notes that since his youth in the 1990s he has moved from a strong belief in mainstream economics to what he defines as a more socialist perspective – where socialism is defined as a form of centralised action. This is interesting, as my personal journey has been the complete opposite. In my youth I believed that centralisation and decisions by experts were the elements missing from society, preventing justice and progress – while now I see as many cases, if not more, where it is a lack of belief in individuals to make choices when given the opportunity that holds us all back. Contrary to Piketty’s introductory comments – property rights do play a role in a just society.

While Piketty talks of “the ideal economic system one wishes to set up”, I can’t help but repeat to myself that I do not know what an ideal is – just that I want people to feel secure and capable to make choices and live a good life. Ultimately, my ideal is likely to differ from the ideal of many others – and so I wouldn’t really want to impose that.

No single narrative is right – and these things differ policy by policy – even for Piketty. As a result, the clearest way to understand the book is to describe the arguments given and the facts that support it. Then to discuss what we see as missing from these arguments, and where there are potentially misleading facts. Over to Gulnara to summarise the book.

Gulnara section

Summary:

This book is a series of newspaper articles linked together by common themes. There is no need to evaluate each article or even theme here in order to discuss what needs to be discussed – instead we want to pull together the threads of the worldview noted at the start of the book.

Piketty notes from the start that he wishes to use the term socialism, but that is a term that can have many meanings – for example in New Zealand the term is fairly innocuous for most of us, while in the United States it is loaded with severe negative connotations in much of the public consciousness. He then defines the key characteristics of what he views as socialism to his mind when he uses the term – there are five of these characteristics, listed as:

- Equality of outcomes – with a strong focus on reducing wealth inequality.

- Equality of outcomes and the right to a minimum standard/bundle – this is the provision of goods on an equal basis through government (universal provision).

- Participation through circulation of power and ownership.

- Globalisation – but not as its done now

- Universality and equality

These five characteristics of Piketty’s socialism are the overarching “policy goals” that Piketty is supporting in this text – indicating that they can be widely applied as appropriate rules of thumb in opposition to whatever current policy settings exist. The case and context for this argument is then given throughout the book through multiple newspaper articles – where these tangible specific examples are intended to make a case for these more general points.

Given this, let’s look at each of these a bit more closely and think about a bit of friendly critical evaluation.

Over to Matt

Equality of outcomes and wealth inequality:

To some wealth inequality sounds like the very definition of injustice, while to others even mentioning inequality in wealth is compared to green-eye envy – and I say this as someone with clearly green eyes.

Many years ago I wrote an article in the Dominion Post on how land was socially owned, and we should be willing to pay a rent to government as the representative of society for the use of that land. In this way I feel that I have clearly signalled my own concern that the fruits of land and knowledge may fall in the hands of too few people – and yet I don’t find the discussion in this book of wealth inequality and wealth inequality trends particularly enlightening.

One of the starkest issues with Piketty’s description of wealth inequality is what is missed in the discussion – wealth inequality without considering the change in the age distribution and average age, without describing its relation to the level and allocation of capital resources in an economy, without indicating how the “claim” on that underlying lands production has changed, without considering changes in the risk-free rate and the ability to interpret wealth ratios, and the narrow consideration of financial wealth while excluding the significant build up and use of human capital.

For simplicity let’s come up with a toy example that can help us think through these issues. Take an economy with three people, a capital owner who works and lives in their own factory and two employees who also live and work in the factory. This gives us one capitalist and two workers – even though all three people “feel” the same apart from a property right over the factory.

Furthermore, the gross value added in the production process is then split between capitalists and workers evenly – so 50% of the GVA goes to one person and 50% goes to the two workers. We may look at national accounts figures and say this appears unjust, as there is income inequality – the capitalist receives 50% of the GVA, while the workers receive 25% each. This is inequality in income from the national accounts.

But wait, this is not household income – it does not tell us the amount the individual can consume given their share of the surplus from a production process. Part of the return to our capitalist friend will be used to maintain the usefulness of the capital equipment that is used in production. If we assume that this requires 20% of the total GVA, then their household income is net of this cost of 20% of GVA. So the capitalist receives 30% of the GVA and there is still a little income inequality.

How about wealth inequality? The measure is financial wealth, so it is the associated value of the capital item. This will depend on the present value of the stream of cash flows from the capital item. The additional return (beyond simply selling labour) is 5% of GVA for the capitalist, so the wealth they are holding is the capitalised value of that 5% per year discounted by their discount rate (which is related to the risk-free rate of return).

And the wealth of our workers, well that depends on their saving. But if we assume that people simply spend what they earn there will be no saving – and it makes our example easier. Namely, wealth inequality would be INFINITE.

Which one of these measures refers to our key concern when we discuss inequality of outcomes? I would argue that only the household income inequality measure truly matters – and we would want to understand why inequality in that measure occurs. Is the capitalist taking on more risk? Are they actually providing intangible capital or working longer hours? Or is it purely luck or a matter of initial endowment? Each of these explanations then may give us a different lens on what an appropriate form of redistribution would be.

Piketty’s views differ from this specifically because of his view that wealth itself generates power – and an ability to force redistribution towards yourself. In this world it is not the broad structure of inequality that is the issue – but the density at the very top. It is not truly “wealth inequality” that is the concern – but the ability for the “elites” to claim the resources of society as a whole. The term wealth inequality here is really just a rhetorical device for noting that concern with excessive power – an issue that turns up in a later argument.

Even if we accepted the view on power, we should not forget the coercive nature of the state – governments have to have power to redistribute resources, and that power is in the hands of those who work for the state and elected officials. My article on land ownership that I mentioned before was unpopular with my work, with the newspaper, and with readers – and I realised that my personal views may differ strongly from the views that people hold about the state. I have significant trust in government – probably well above the average.

But taking a step back, I can understand where people are coming from. The government is an institution that can be captured by vested interests, and it isn’t guaranteed that they will always act in the common good.

Furthermore, even with public ownership and the provision of income from that to people in society it is more tangible to point to the provision of a house – the provision of food – or the provision of clean air – than it is to describe the provision of an income that allows individuals to trade-off between things based on their own subjective value.

Trust and security both suggest that individuals themselves value, and are more willing to contribute within, a society with clear property rights that they can share in.

Such an argument does suggest a floor – an ability for someone to live and provide for themselves without reliance on others. It also points to a reservation option if society demands too much from them. But wealth inequality statistics don’t tell us much about that, and if not considered critically can be used to paint a picture of injustice where none exists.

The discussion of wealth inequality is in part a red herring – the true issue is that of a sufficient minimum standard and concerns that institution arrangements and structures lead to regulatory capture and market failure.

Equality of outcomes and rights to a minimum standard – the provision of equal products

Now we can focus explicitly on the discussion of a minimum standard – what does this mean.

Here there are three types of public provision to consider with varying arguments – and which are intrinsically intertwined:

- Underlying absolute needs of the individual.

- Products and services required for equalising the “relative” position of the individual.

- Public goods, products with significant market failures due to asymmetric information, and goods with positive externalities/spillovers.

It is hard not to mix all three, as a single item of government expenditure can embody all of them – i.e. education expenditure.

However, it is important to be clear regarding which of these is the motivation – if you use a market failure argument to state it would clearly be more efficient to spend on this item, but you motivate it using relative position, and fall back on absolute need when pushed, your argument becomes incoherent. At that stage people will start using the “idea” of your argument to push for things in the same way, and given each of these will lead to different observed outcomes your critics will simply pick the argument that appeared to fail in the data to undermine what is being said.

However, I have no experience of these things – I have grown up in New Zealand, born at the start of the fourth Labour government when New Zealand opened up. It is Gulnara that can speak with more authority and experience on the issue of growing up in the Soviet Union where many items were provided by the state.

[Gulnara to talk about her experience here]

Thanks Matt. To my mind there are actually two separate issues here that deserve attention. The first is how pre-distribution was used to achieve “equality of outcomes” and its costs. The second is the post-distribution that occurred in terms of the public provision of products, touching on the issues you have just discussed Matt.

I don’t think we can talk sensibly about one without the other – as the two are linked in terms of how they influence incentives.

Communist Russia progressed from the status of a backward nation to the world’s second-ranking industrial power. Most of this advance was made under a system of tight economic controls which enabled the government to direct investment and labor into development of a heavy industrial base at the expense of other sectors of the economy.

As the Soviet economy became stronger and more complex, the system of central controls became more cumbersome and less able to meet the nation’s needs – output growth started to fall.

Why? Due to the lack of incentives and price signals.

In a number of enterprises the wage rates were fixed in such a way that the difference between the qualified and unqualified, heavy and light work, disappeared almost completely. Equalisation of pay leads to a situation where the unqualified worker does not strive after gaining qualifications, as they do not see any improvement in their personal position.

The fact that wage rates even existed, which was not Lenin’s first desire, indicated that the Soviet Union recognised, it had to work within constraints. But if they could not use markets what other incentive mechanisms could be used. The first solution that was tried were appeals to individual pride. Hunger for prestige was introduced: red labour banners, distinguished scientific, technical and arts worker medals – paired with small material awards added to those honours. This led to increasing status competition to achieve these awards – driving increasing corruption.

During Stalin’s time the need for explicit pay differences was recognised with the difference in pay between the lower and the higher grades of workers increased. From then on those who did not work were seen as parasites and the view of “from everybody according to his ability, to everybody according to his work” was introduced.

However, pay differences never reflected the same difference as was observed in the Western world. Why? Because of underlying public provision associated with roles. The Soviet Union used direct ownership and provision of goods and services as a way of remunerating staff – and the big difference between this and other forms of remuneration was that it was non-transparent. Such non-transparency drove corruption, with a culture of corruption leaching into everything that occured.

The Soviet system did provide you with your minimum needs such as housing and effortless access to the job market, and hence a minimum income as long as you were able to do the job you were told.

However, if you had talents and skills and wanted to use them to progress, this was not possible. Nation-wide corruption was prominent. In education for example, you had a chance to study hard and get into university, but say you had 5 places allocated to engineering in a given year, 3-4 of them would be already taken by some (e.g. a prosecutor or mayor’s child), leaving hundreds of students to compete for 1 single place. Similar things would be observed in allocations of prestigious jobs such as medical doctors, university lecturers, and more higher up in the hierarchy jobs (mayors, lawyers, head of any departments). The blockage of access to any of this sort of incentives, led to a lost opportunities of talents. It was almost impossible to get into positions you were striving for if you didn’t have any relative, friend who could pretty much sort it out for you.

This happened with everything – better housing would go to people based on who they know, better jobs would go to people who were better at socialising, and better schools would be available to those who got on well with the university.

I have personal examples, but I feel uncomfortable mentioning them. Ultimately, for all its imperfections, outcomes in the West bear some relation to effort – and that link is essential for any sort of trust in society. Public provision can be just as corrosive as entrenched private sector inequality – and this is a trade-off that Piketty often misses.

[Back to Matt]

This does lead to a question though – why is Piketty focused on government provision of these goods and services, and not government provision of the income necessary to buy these goods and services with private provision?

There can be good reasons for public provision – market failures stemming from asymmetric information, competition issues, institutional issues, and spillovers or externalities. Relatedly, the broader inability for individuals to pool risk and the belief in a given minimum living standard for all individuals may motivate public provision – although it is more likely to motivate direct income support. Behavioural economics may come in and state that individuals will not purchase things that are in their own interest.

Finally, but differently to above, there may be a social reason for believing that everyone should receive the same product – in order to enshrine some conception of equality of opportunity, or to engender a sense of shared experience between individuals.

However, this does lead to three concerns we may have about such provision:

- Inefficiency: The traditional “inefficiency of public provision” – the idea that civil servants, unencumbered by the discipline of competition, would extract surplus for themselves by working less. More broadly, we have the incentive issues Gulnara noted earlier.

- Consistency with other measures: The interpretation of income and wealth inequality statistics may change – if we take our toy example from before, if we know that a government was providing education, food, housing, toilet paper, and roads would we feel differently about the inequality of income and wealth than if it was not? Final income studies try to account for this, but they are fairly rare and often allocate expenditure in an ad hoc or subjective manner (i.e. Harding. Lloyd & Warren 2006: The Distributional Effects of Government Spending and Taxation | Levy Economics Institute (levyinstitute.org), Auten Splinter 2019 AutenSplinter-Tax_Data_and_Inequality.pdf (davidsplinter.com), and Saez Zucman 2020 w27922.auto.pdf (berkeley.edu))

- Preference heterogeneity and choice: It sounds nice to provide things to people, but there are two issues that come up.

- The obvious one is that people may value things differently, and so providing something without choice may simply mean the people don’t get what they most desire – they no longer have a choice about the type of health care or education. Here we would have inefficiency in terms of how inputs create social welfare.

- But there is a second issue – how do you operationalise provision? Everyone has different educational opportunities because their parents will spend a different amount of time studying with them. Focusing only on equality of the provision of education led Piketty to bemoan school choice in “Inequality in France” and “Parcoursup: Could Do Better”, but what happens if the same argument then led us to say that all children should go to a boarding school to remove unequal opportunities. Is such a dictate from above truly just? What about a dictate that the same school materials should be used? What about if the children were banned from going home for the holiday to promote equality? What about if the children were taken at birth to prevent any parental based advantage – where do views of individual rights become sufficient for us to say no, and how could they be included in the argument?

All I can really say for this section is that measures of expenditure are essential for understanding outcomes – and we should be careful trying to be too dogmatic one way or the other. To go any deeper would require an additional hour for this video.

Sharing of power

Piketty’s focus on power sharing is two-fold:

- Sharing power within a firm through increased employee ownership and voting rights.

- Sharing power within society through greater taxation on wealth and inheritance and the provision of a minimum “capital payment” to all individuals.

Let’s start with the first point. Why is tying an employee to an organisation the way we want to address any imbalance between the employer and employee power? In the articles “Basic Income or Fair Wage” and “Rethinking the Capital Code” Piketty makes clear that it is unfair bargaining positions that he is interested in addressing with employee ownership schemes – although there are a number of OECD papers now linking these schemes to productivity and wage gains from such firms, his focus is rightly on the issue at hand given the likely selection bias issues in a number of these studies.

Maybe it is the New Zealander in me talking, but the ability to cleanly move between jobs, contribute to different projects, and move to whatever task appears to need me most is something that is positive – and rules that assume and enforce a situation where people have to stay tied to one job seems wrong on both a social and an individual level.

As our toy example earlier noted, it was the combination of employees and an employer that generated the GVA, which was then split between the individuals. The ability for the employee to force a move away helps to give them the position to bargain a higher share of that surplus, the employer and employees incentive to maintain and build capital (physical and human) similarly creates the surplus that is shared. If joint ownership helped them to do both, and they are both in a position of power, it does not seem necessary to dictate joint ownership – and such dictates appear to be blunt tools.

Furthermore, such dictates may have unintended consequences – they link an employee with a firm potentially reducing their outside options, they make the employee more exposed to shocks facing the firm, and they make the retirement savings of the individual less diversified. Ignoring any costs to capitalists even from a pure workers perspective there are significant shortcomings to work through.

This is not to say there is no room for equalising bargaining positions, and for improving employee rights in the face of monopsony and asymmetric information. And mobility itself is not costless – the loss of firm specific capital and the insecurity associated with job movement and job fragility are all real. But labour laws and fundamental income support appear to be a way to address this without the individual being tied to the business.

The minimum capital payment is something that fits strongly within the narrative we’ve been supportive about above. The incomes we all earn, and the returns on our assets, are in part due to the fact we are in a high productivity world – rather than just a product of the sweat of our brow. In such a case, ensuring that everyone starts off with something feels consistent.

Similarly, recent research by Balboni etal 2021 indicates the importance of available capital for helping individuals get out of poverty traps. https://twitter.com/ChaseReid5/status/1474894957190295559

But let’s be clear on how things are being financed. A decision to finance this with a wealth tax is increasing the cost of capital, and will in turn reduce investment. We may see that as appropriate, we may see this as preferable to alternative forms of financing, but there will be a change in behaviour.

Why is it that people who accumulate should be liable to pay more tax than those who have the same income, but just love spending more? What is the actual “social dividend” that is captured in transactions between individuals, and why is it not that figure that we are reallocating? Given that, government revenues and expenditures are then how this claim is actioned.

It is here that Piketty’s argument is weak – to raise the funds for the type of capital redistribution required we would require everyone to contribute on the basis of their share of this boon of productivity, the mechanism of a wealth tax (which I’d take as a de facto more progressive tax scale) is not sufficient. Whether you take the revenue estimates of Sarin and Summer or Saez and Zucman saez-zucman-responseto-summers-sarin.pdf (gabriel-zucman.eu) – the higher of which Piketty cites in “Wealth Tax in America” – such a tax at rates that create a tax liability greater than the income flow would not be sufficient to fund the redistribution discussed – and would be well below the Sarin Summers estimates of improved broad tax enforcement Understanding the Revenue Potential of Tax Compliance Investment | NBER.

The comparison to history here is a red herring, again. Government expenditures to GDP are now higher in most countries than they were at any time in the past, and are financed through broad funding measures. Piketty believes in greater expenditures than in the past and that will require greater funding than in the past, with the consequences that creates – there is nothing wrong with believing in that, but we need to be clear on the trade-offs.

If the implied tax on income earned from an asset rose towards 100%, people would switch from considering how to avoid tax more than how to effectively utilise the asset – and marginal discussions of how UCC changes would influence the capital stock, as Gulnara and myself had undertaken earlier in the year Taxation, user cost of capital and investment behaviour of New Zealand firms (vuw.ac.nz), would not give us an accurate picture of this.

And this is the crux of the debate – government expenditures and transfers, along with taxation, is how the “minimum capital payment” is operationalised now. The fact I can use a public road, go to the hospital for a nominal fee, and sit in a park all indicate that there is a type of “minimum capital payment” already. The questions that separate people are “how large should it be” “who should contribute to it” and “who gets to choose how the capital is allocated”.

Globalisation and universality

The last two options we’ll put together into one and only discuss briefly. Although there is the odd bit of rhetoric in there that globe twitter may disagree with – the basis for both these sections is for global equality and anonymity for the treatment of people, which are essentially globes goals. The guiding principle of any governance institution, or any supra-national organisation, should be to ensure equal treatment of individuals and support for minimum standards – where these standards of equality correct for differences in opportunity based on gender and ethnicity.

Just like the majority of economists including us, his view may read as naive for those from both the left and right – who believe in the moral imperative of some cultural or social arrangement, that some differences are “natural” or “necessary”, or that it is practically impossible for such coordination to occur.

Personally I find it refreshing. When we look back to now in 100 years it would be our willingness to accept poverty in low income nations that would lead our great grandchildren to view us as immoral – not the fact that someone once said something inappropriate on twitter. The fact that the left and the right can only see injustice insofar as it relates to them or their peer group – and not through our global refusal to support those most in need – is such a clear failure in public discourse that on these points I have no real area for disagreement with Piketty.

Articles such as “Europe, Migrants, and Trade” and “Manifesto for the Democratization of Europe” also indicate that Piketty also sees the inclusion and integration of migrants as part of this overall program – showing a consistency that an increasing number of economists are losing in recent years.

Where this view of equality does create disagreement is with how others will interpret Piketty – and sometimes how he interprets himself in the newspaper articles. In a tweet from Noah Smith he notes:

on Twitter: “In which @BrankoMilan argues (correctly) that the people complaining about capitalism are almost exclusively people in rich Western countries where capitalist globalization has caused the disappointment of the middle classes.

on Twitter: “In which @BrankoMilan argues (correctly) that the people complaining about capitalism are almost exclusively people in rich Western countries where capitalist globalization has caused the disappointment of the middle classes.

Is the injustice here that some middle class Americans have seen income growth stall – as it is Americans, not other high income countries. Or is it the level of poverty in low income countries? The idea that if the wealthy simply had less wealth then both the global poor and middle class would have been better off is simply not true – those with wealth are those who built and allocated capital in such a way that it helped to lift the truly poor out of poverty, to their own interest. Reallocating from the most wealth alone would not generate the revenues necessary for the global expenditures Piketty suggests, and yet this is what he appears to indicate from the very first of his newspaper articles.

Why do I raise this – Piketty cites an earlier version of this very graphic in “After Climate Denial, Inequality Denial”, but all he states in the article is that this graph makes the case for the inequalities he bemoans and that others that view it differently (such as the Economist magazine) are being dishonest. This is not right. To argue from data we need a counterfactual, and acting as if this is a fixed sum of income to be reallocated is a likely poor counterfactual – asking “why” is important, as fits the idea that debate is kept open which is what he asks for in the first chapter of this book.

Questioning this also opens other doors that he may have inadvertently shut – market power and concentration of firms, regulatory capture, unequal international treaties. All these issues can offer explanations for the distribution of income and wealth that suggest policy conclusions that differ from expenditure and revenue raising. Understanding “why” is important for knowing what intervention is truly just.

In this way, the rhetoric is inconsistent – picking and choosing the cause in isolation based on the subject of the article. The honest interpretation that everyone who has benefited from technological growth over a long period of time would need to contribute to support his redistributive grand-design is missing. And that where income change is not the product of technological growth, but instead power, we need to understand the power dynamic prior to considering the intervention. If someone has power due to concentration or regulatory capture, they will have the means to avoid indirect instruments such as a tax.

Conclusion remark

Also, I will say one more thing about the arguments overall – after all the road to hell is paved with good intentions. Within any structure, institution, and society it is always the way that the “needs of the many” can swamp the “needs of the few”. Or even the wants of the many can swamp the absolute needs of the few.

We all have varying conceptions of justice due to different perspectives, different preferences, and different beliefs. And the tyranny of the majority is a real thing, that becomes strongest when change is driven in the name of justice and victory over some other.

The principles of universality and equality work only when the rights of the individual are enshrined and protected – and every single time we think of a neat scheme to improve some metrics of outcomes we need to keep that in mind. This isn’t some way to slow down progress – it is a way to stop our generation from becoming the monsters we read about in history books.

A desire to do good needs to be balanced alongside humility and a recognition that we don’t always know what good is – if we lose sight of that we might lose the argument, but even worse we might win it.

]]>This week a different lecture is coming in to discuss economics with you – he’s great and you are all going to have a wonderful time.

I cannot link your lecturer’s slides here – but he is covering similar ground to other years. As a result, here is the Wednesday and Thursday slides from last year.

This week you have focused on trying to understand our friend the rational consumer, and how we can express the following:

- The opportunity set they have available to them.

- The choice they make given that opportunity set.

Given this lets tie together some terms and think about what they mean.

- What is the endowment for the consumer we are considering in these lectures?

- Given this scarce endowment and the consumption opportunities that come from it, what is the opportunity cost associated with buying a particular item?

- Describe the concept(s) that suggest our consumer would choose a point on their budget line? What are some of the reasons why they wouldn’t do so, even if they met our assumptions of being rational?

- Why is it unlikely that some will choose one of the extreme “intercept” points for their level of consumption? How does an indifference curve relate to this, and what concept of utility is this related to?

- What is the law of demand and when, for a rational consumer, does it fail?

My big tip for you all is not to get too over excited about the indifference curves – instead try to understand points on the budget line, and what it means to move to a different point on a new line.

It is by doing this, with a clear understanding of what an “income” shift looks like, that you can work out income and substitution effects – which is one of the tricky parts of this week.

]]>

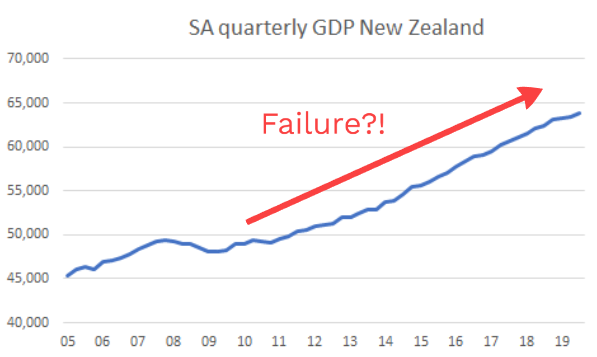

Sumner’s view was that monetary policy can be effective – but the Fed and US economists were acting as if it was not, and were thereby making policy too tight. As a result, even though growth occurred it was too slow and showed up in low inflation and high unemployment during the last 10 years.

The US central bank, and related economists, kept acting as if persistently low inflation outcomes – and to some degree high unemployment – were factors the central bank has no control over as interest rates were near zero. However, this has two problems – there are other tools, and they did start to raise interest rates while Sumner’s view was that conditions were too tight. In this regard the Fed should have been more accommodative – and the slow recovery and economic and social loss for it is their responsibility.

The question I am asking in this post is “how much does this argument hold for New Zealand as well?”

The New Zealand case

Sumner’s argument is based upon a view that metrics indicated that policy had been too tight historically – and more should have been done to boost activity by the Fed. The metrics aren’t really mentioned and he talks against the Phillips Curve relationship, but I will use that type of idea to understand where he might be coming from.

Specifically, he still views that there is an output gap that is not being satisfied in some sense by policy. So let’s look at two forms of metrics to judge success:

- Inflation outcomes, and relating labour market measures;

- The level of Nominal GDP (NGDP).

Inflation, labour cost inflation, unemployment

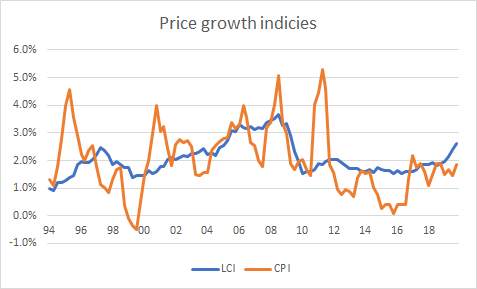

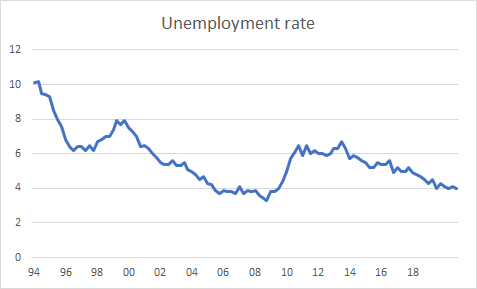

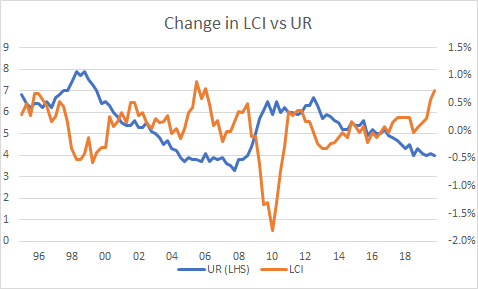

These are inflation targeting central banks, so the question is “how did the RBNZ do at meeting their inflation target”.

Let’s look at three graphs – growth in labour costs and prices, the unemployment rate, changes in unemployment relative to changes in labour costs.

Let’s look at the bumpy series that is annual growth in consumer prices (the CPI). After 2011 (and the GST hike based spike) inflation was below 2% until well into 2016 – in fact it undershot the bottom of the target band (1-3%) during 2016!

New Zealand is a small open economy exposed to tradable goods prices. As a result, a drop in commodity prices was a big driver of falling inflation in 2015/16 – but other inflation measures suggest that wasn’t the whole story, with even non-tradable inflation getting below 2%.

But this isn’t necessarily monetary policy failure – there was an unexpected decline in food commodity prices, which NZ exports, over that period. The central bank then responded in a way where inflation returned to the mid-point of the target.

Instead failure could be judged through inflation expectations. And we’ve noted for reasons here a good indicator of that is the labour cost index. Growth in that did slip, and as a result if monetary policy was seen too tight during the late-1990s (eg during the Asian Financial Crisis) it may be seen as somewhat too tight through 2012-2016. However, readings since then point to a central bank hitting its targets.

The unemployment graph above gives a similar story. Unemployment didn’t surge up again following the global financial crisis – but it did stay stubbornly high until 2016, and now has pushed its way down. Again, a sign of conditions that were too tight for a period – partially as a result of unanticipated shocks – and then what seems like reasonable monetary policy since.

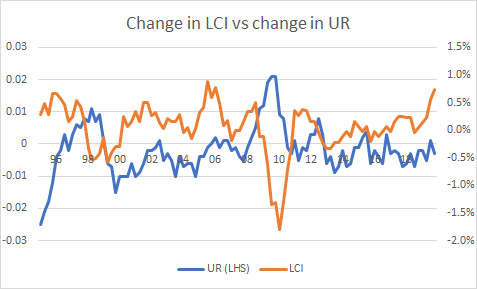

Changes in labour cost growth have been sharply related to changes in the unemployment rate through time, as shown in the above graph. This appears to give credence to the “unemployment rate as output gap” that is used by Gali – and is really closely related to simply thinking about a Phillips curve.

However, the key perspective is to think about the level of unemployment against LCI growth – namely is there a level of unemployment where wage growth/inflation accelerates [often noted as the NAIRU]. In this way, the unemployment rate has now fallen to levels where we have previously seen wage growth accelerate.

Pulling these all together, the RBNZ has managed to keep inflation near or in the target band, keep wage inflation close to the midpoint of the target, and we now have a low unemployment rate and accelerating wage cost pressures. This sounds like a situation where the central bank has succeeded in their aims – and maybe points to a situation where policy may need to tighten in the future!

Also note here that, the way we’ve discussed this is also sympathetic to the Fed – they never saw inflation collapse well below their target, and unemployment did gradually decline while labour cost growth was “anchored”.

Nominal GDP

However, there is another perspective here.

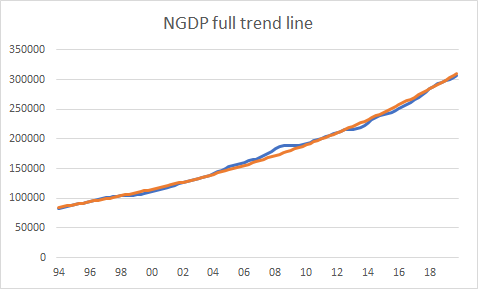

Let’s go back to the idea of NGDP targeting – as discussed here and motivated here. If Sumner’s monetary policy failure is with reference to this metric, let’s look at New Zealand. First NGDP relative to an exponential trend (so a fixed rate of growth)

Things look a bit overheated between 2005-2008, and a bit underheated through patches of 2012-16, but policy has got us back on track!

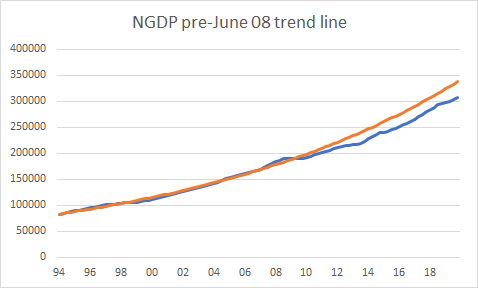

But is this the right idea to look at Sumner’s view? For one, he is stating that it was policy post-2008 that failed, so the comparison should be to the trend line up to that point (say June 2008). Here we have:

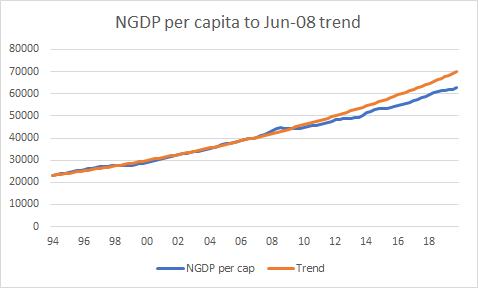

That doesn’t seem to be as positive a reflection on policy. But population growth has changed, let’s look at the graph with per capita.

This appears to show a larger, and widening failure to meet this trend – which by Sumner’s definition constitutes policy failure.

Policy failures due to deviations from that trend can then be thought of as moving away from that target in two different ways: it could move away in a level sense (we undershot but will keep the growth going forward) or growth sense (continuously having lower growth so the gap gets larger). They mean different things.

However, if we are using the trend from 1994-2008 both of these things are happening – this metric is pointing to monetary conditions that are too tight both in terms of targeting a level AND targeting growth in NGDP (or demand).

Nominal GDP and LCI measures for New Zealand.

So looking at these measures what can we say?

If we work off the idea of capacity in the labour market, the unemployment rate did come down (note NZ’s participation rate was high the whole time – so we don’t have the US issue of discouraged workers) then it appears policy was pretty good.

Inflation measures were low, but New Zealand is a small open economy that was observing external price shocks – actual inflation expectations embedded in wage negotiations in the labour market came in near target, while “spare capacity” in the labour market has been limited for a while.

What about NGDP though? This seems less positive – if the goal was to stay on some trend line for NGDP growth monetary policy in NZ has been persistently too high. In fact, if the goal was to stay on a given rate of growth for NGDP policy may have even been too tight.

If this is the right metric, then there has been some degree of policy failure.

But if this was in the past, why does it matter for now?

Why it matters for now

When it comes to thinking about appropriate policy now, we need to think consistently with how we have judged policy in the past.

In that regard, we need to ask what is happening over the past year with the jump in the LCI number? There are two potential causes:

- Labour share rising due to greater bargaining power (keeping it with monetary policy, so in this instance assuming the share had been driven down for the same reason prior).

- Inflation expectations are rising – and a sign of coming inflation.

So recent labour market indicators are pointing to inflation/capacity concerns while NGDP well below trend points to space for potential growth.

Does policy need to be accommodative and allow these measures of “wage inflation” to rise or is this a signal of a closed output gap and the need to tighten policy. The US seems to be facing the same query, with their labour cost index picking up while NGDP remains below its pre-June 2008 track.

Understanding which is the driver – and how this can tell us about the appropriate stance of monetary policy – seems key right now.

This is something I want to discuss here.

In that regard the Spin Off just had a good article talking about economic consequences, and interest.co.nz also had a good piece talking to the bank economists. Finally, Westpac released a bulletin that discusses what they think is important. This is a complement to their pieces as I want to use the same “demand” and “supply” shock analysis as I did in the prior post to bring some of these concepts out.

What I’m discussing below is how I would look at this sort of crisis in real time as an interested observer – I work in research not policy, so I see this as a chance to open up a dialogue with other interested people in the comments below. Any insights you have would be richly appreciated.

Furthermore, as I just don’t have the data on hand I would like (again I work in research, not as a forecaster, an investment analyst, or a policy person) I can only talk about what I would use – if anyone has been using this data and can discuss trends it would be great to chat about this in comments!

Note: Thanks to Matt Nolan for discussing this with me, and helping me to get the right data sources for this post.

Scenario 1: No virus in New Zealand – focus on the economic effects

As with the previous post it is best to have two separate scenarios, so let’s start with the first one first – when the virus is significant globally but doesn’t reach New Zealand. This is a good place to start to think about this issue as it also represents where we are at the moment.

In the previous post we noted this was a temporary negative demand shock. So how can we think about the composition of the demand shock.

As a temporary demand shock there is not an initial need for the government to do anything – once the sickness has passed in a couple of months demand will return to normal. Any short-term disruption is best dealt with by the central bank reacting, while individual businesses should be able to deal with what is a relatively small shock.

However, if the demand shock is longer but not permanent there is a concern that businesses that are exposed to the shock may be unable to insure themselves against this – with consequences for employment and knowledge in the economy as the firms disappear before the shock reverses. Such a shock is temporary but persistent.

In other words, we are worried about business failure from a prolonged period of weak demand in specific sectors there could be a case for government insurance. In this case we need to identify the sectors that are effected, and ask what form of assistance is appropriate. I would look to similar programs that already exist (eg payments to farmers during severe droughts) as a form of social insurance.

The composition of the demand shock

How can we think about the composition of the demand shock – this is an issue I’ve heard people discussing on the street, so it is certainly an issue of interest! Furthermore if the shock is temporary but persistent there may be a policy motivation for helping out.

So what are the key areas where demand is expected to drop in this case? We discussed this last time:

- Tourism (and export education),

- Export trade,

- Consumer and business confidence.

But what indicators – or bits of data – can we look at to try to understand what the costs could be?

Tourism and export education

On the tourism numbers there is not too much so far, as the airport changes are recent. So the international travel numbers will be a bit late. [Side note: There will also be an interruption in terms of international migration – but this is likely to reverse out and so will be put to the side]

However for the urgent matters, the Ministry of Transport is the first contact to check if they have daily or weekly figures on “port” arrivals from air in New Zealand which could be analysed to try to understand what the initial shock is.

We could then come up with a rough estimate of the drop in expenditure based on the decline in numbers, and the spending estimates from the tourism satellite account. Using the daily data could provide a good counterpoint to the macro estimates from private forecasters.

Without those numbers another idea is to ask what happened with tourism and SARS – old NZ Herald articles point to a drop, but any other research on this could be useful. Also this drop needs to be corrected for the fact that tourist arrivals from China are now a much larger percentage of total tourism than they were in 2003 – implying the “shock” is larger!

For the export education figures – it would be good to chat with the big providers (eg universities and polytechs). Matt tells me he keeps receiving emails from the university about the interruptions associated with the border closures, so they have the data – and that the service Tertiary Insights (formerly Education Directions) is also providing good information.

Export trade

Here it is difficult to figure out how trade will drop – but if we have an idea of where trade occurs we can tell risks. And we can work this out by looking at the Overseas Merchandise Trade indicies to understand the share of what and where New Zealand firms sell overseas.

One issue is that this doesn’t separate between the “volume” and the “price” (later quarterly statistics do) – and this difference matters for thinking about the economic consequences.

As a side note, if the virus constrains imports from China could also put up some pressure on import costs for both New Zealand firms and consumers, which might have more general negative consequences – although there is little policy can do in this space.

Staying on the export side we need to break down things a bit more. Product by product is a very laborious task, instead we can think about “durable” and “non-durable” exports.

Let’s look at forestry as an example. It is heavily influenced by what is happening, with trade to China stalling. But the logs can be stored as inventory as they are durable. As a result, this is partially reversible.

With non-durable (meat, dairy) the produce has been created and will simply be destroyed if it is not sold – as a result, it needs to be sold in a market for a lower price or essentially lost. The reduction in demand will lead to a drop in price which is a permanent loss in income.

In this way, it is likely to be providers of non-durable products that have the most to lose from the crisis – while durable sellers face issues of liquidity.

So how do we measure these shocks?

For non-durables it is all about price, so we need spot market estimates. Commodity futures (eg on Bloomberg) will give a good idea here. For dairy we have the Fonterra GDT every fortnight which did fall sharply but I would expect a much larger fall in prices going forward. Scenario analysis (looking at a range in price shocks) can help to think through the risks.

For the durable goods we want to understand quantity and price – so if there is any information on logging operations or mills shutting down that would be valuable.

Consumer and business confidence

Finally we have the unknown general demand impact – from consumer and business confidence.

Surveys of these measures are relatively infrequent (at least for a sudden crisis) so they can only take us so far. Instead Google Trends can give us a great heads up on what is going on.

More broadly, without confidence numbers we can ask about history and other countries – what has happened to confidence in areas that have had recent surveys? What has happen with the stock market as an indicator of the priced in cost of the the crisis?

Using this to understand the consequences

Given these specific shocks to certain sectors, there are questions about risks to enterprise operation (will firms with knowledge shut down due to uninsurable risk?), employment (are there consequences in terms of jobs). Furthermore, there is a question of what areas will face the most pressure (what parts of New Zealand are most exposed to these shocks).

The way to look at this would be to construct an index of industries that are most exposed, and then look at GDP and employment shares in the exposed sectors – as a first approximation. Given this information is available by region online this gives a quick and rough way of thinking where the risks are – and where policy might be usefully deployed. I have seen this type of data produced in government such as here, which may be used for this.

Matt recommends a tool his old work has for this type of work, which can be found on the Infometrics site here. This can be used to easily construct a “sector” that we think is vulnerable and then quickly see its employment, GDP, and business count shares by region. That sounds good, but one needs to pay a subscription for the service so I can’t really go through that process in this post

Scenario 2: When it comes here

For the second scenario we can keep the same shock and add an additional drop in retail demand and also hours of work based on the severity of the sickness in New Zealand (and additional confidence effects) – this requires more close up look and a general set of clear scenarios for scenario analysis.

However, the key point is these shocks would be an addition to the more clearly defined sector shock posited above.

What becomes much more important for policy is identifying coordination failures.

The clearest example is with regards to how to stop or slow the spread of the virus, as a communicable disease implies there are externalities from an individual’s choice.

Let’s say employees and employers are averse to using sick leave – but not using it increases the chance of transmission which has an externality. Do we need to advertise the importance of taking leave? At what point are schools and public offices closed? When are non-essential services closed to limit the spread of the virus?

These are public health issues, where what might be best for the individual has severe consequences for the other individuals around them – and so restrictions could be necessary. But how to judge that?

No GDP figure, or appeal to demand and supply can inform us on that question – so when the virus reaches here the government’s main role is in making judgement calls about these trade-offs. And the some of the best advice will come from epidemiologists and public health professionals regarding these specifics, not so much economists.

Imagine being able to print your own currency.

Click a button, add a few zeros and voila you’ve increased the money supply.

The Reserve Bank can do it, and, believe it or not in a similar vein so too can Air New Zealand.

Our national carrier doesn’t have control over the New Zealand dollar, but it does control the supply of New Zealand’s second biggest currency – the Airpoints Dollar.

Airpoints Dollars conform to the standard definition of a currency – they are a medium of exchange for goods and services, they can be used to store value through time, and they are a quotable unit of account.

Air New Zealand operates a fixed exchange rate policy for its currency, where one Airpoints Dollar can be redeemed for one New Zealand dollar worth of flights.

Furthermore, in addition to being a currency, the Airpoints Dollar loyalty scheme also adds to Air New Zealand’s bottom line.

Air New Zealand is the sole institution with the ultimate authority to issue the Airpoints Dollar currency and back-of-the-envelope calculations show that the value of the airline’s loyalty scheme could be around $400 million.

At first brush, this valuation of Air New Zealand’s money printing prowess may seem a little far-fetched, but bear with me. The remainder of this article outlines how I arrived at this rough valuation and describes how an airline can generate revenue from a loyalty scheme.

Valuing Air New Zealand’s Airpoints programme

Although Air New Zealand releases detailed information regarding the profitability of the various parts of its air operations, unfortunately our national carrier is somewhat cagier when it comes to its Airpoints loyalty scheme.