What is the cost of capital and investment link?

In this post I intend to motivate research that is underway by Lynda Sanderson and myself on the investment behaviour of New Zealand firms. [“Taxation, user cost of capital and investment behaviour of NZ firms” forthcoming]

The goal of our current research is to understand how changes in tax settings in New Zealand have influenced the investment behaviour of firms. Doing this involves thinking about how taxation can influence investment. The key channel it does so is by influencing the price associated with investment – what is called the user cost of capital.

What is the User Cost of Capital (UCC)?

Before introducing the UCC it is useful to think about what we are asking about when we talk about investment. Businesses invest to build up a stock of capital that they can use to create goods and services.

Imagine that the primary motivation of these firms is to make the most profit they can, in that instance they will have a desire to build up their capital until the cost of adding more capital is equal to the revenue benefit associated with doing so. The benefit is the marginal revenue product of an extra unit of investment, and this declines as the firm invests more both because additional investment adds less and less extra output and because more output drives down the price of the product.

If the firm could simply rent the capital equipment then they would keep renting until the marginal revenue product is equal to the rental cost. However, when the firm invests they own the capital – so how can we think about this cost?

The user cost of capital (UCC) is this implied rental cost from investment. The way to think about this is that, if you had a dollar to invest, the UCC is the cost of employing that dollar – both in terms of direct costs (eg the depreciation of the asset) and the opportunity cost (the interest that could be earned on that dollar).

Taxation influences both the opportunity cost of investing and revenue from the investment after tax . As a result, the user cost of capital measure used allows for taxation, inflation, capital gains and the depreciation of capital goods. If tax settings increase the user cost of capital (eg a higher corporate tax rate, or less generous fiscal depreciation allowances) then this will reduce the desired stock of capital that firms will wish to hold.

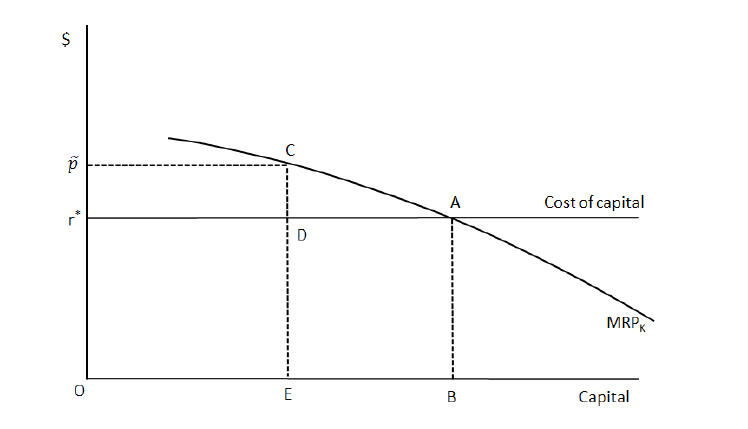

This can be shown graphically as follows based on Creedy and Gemmel 2017– “Taxation and the User cost of capital”.

In the graph above, the term ρ represents the UCC with taxation, and the firm desires holding a capital stock of E. If taxes were removed, the UCC would fall to r* and the desired capital stock would rise to B.

How does this relate to investment?

The above discussion indicates how the UCC influences the capital that a firm desires to hold. But how this translates into investment is a bit more complicated.

It is difficult for businesses to change their investment levels, a concept economists term adjustment costs. These adjustment costs imply that, when there is a change in the desired capital stock (eg due to a change in the UCC) then it takes time for the actual capital stock to adjust to that level. During that process the net investment rate will change until the new capital stock is reached. Furthermore, in the long-term the change in the capital stock will change the amount of depreciation also influencing overall gross investment.

In this context, our goal will be to understand whether investment is responsive to changes in the UCC due to changes in tax settings – to provide evidence regarding whether the capital stock will ultimately be influenced by corporate tax policy changes.

Next time I will outline some literature and broad results (with our initial findings) related to the UCC-investment relationship.