When forward guidance doesn’t guide

VoxEU have recently launched a book on forward guidance and it has demonstrated wonderfully my ignorance of central banking. I thought that when bankers issued ‘forward guidance’ they were doing it to escape the zero lower bound by promising to keep rates lower for longer than they normally would. Something like this:

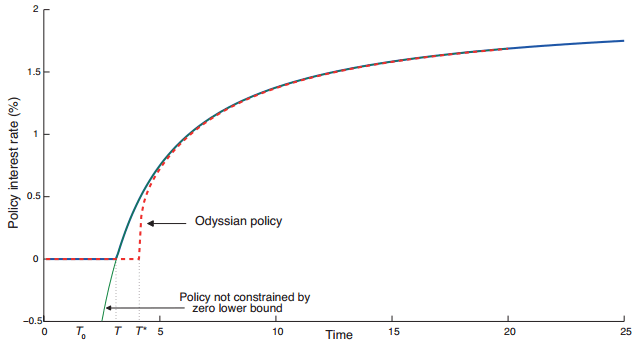

Source: VoxEU eBook

The ‘Odyssian’ guidance seeks to lift nominal expectations by promising not to tighten policy in future. For a while, the bank’s policy rate will dip below the level you’d expect if they were never at the ZLB. That is the sort of guidance that the Bank of England has explicitly disavowed. They clearly say that their guidance policy does not alter their reaction or expected rate path at all. It is simply another communication device to explain to people what they would have done anyway. In that case, why do it? I can think of three possibilities:

- The communication between the Bank and market participants is still so bad after twenty years of inflation targeting that they needed a whole new way of talking to explain themselves. This is not as unlikely as it seems because the Bank hasn’t been in this situation before so communication devices aren’t well calibrated for it. It has been variously accused of being an ‘inflation nutter’ and abandoning the inflation target, so a clearer view of its reaction function is probably welcome.

- The Bank has changed its view on the balance between inflation and output. It needed a way to make that clear to market watchers. It is possible that the Bank’s view has evolved since the beginning of the crisis. It hasn’t faced an extended period of high inflation and low growth before so that would be natural.

- The Bank is going to keep rates lower for longer but refuses to admit it because that would be seen as a breach of their inflation target. Consequently they say one thing with their guidance policy and another in speeches. This is possible but it seems an odd thing to do so I think it unlikely.

The real question is whether guidance policy that doesn’t change the expected stance of monetary policy will change anything. The only way it could work is if market participants had systematically incorrect ideas about the Bank’s reaction function, which seems unlikely. If they did, after monthly minutes and regular forecasts detailing the Bank’s outlook, then it would be strange for a single communication device to radically change them. Only time will tell but let’s hope the Bank is right.

Also see Tony Yates and Simon Wren-Lewis on this.