GDP forecasters: can we have your confidence intervals please

There are many forecasts of how well, or otherwise, our economy will do over the next year. However, as a rule these forecasts are not very good at providing a candid account of the uncertainty that is present. Most forecasters simply provide a point estimate for what they expect quarterly GDP growth to be in the next quarter or so.

Unfortunately, the margin of error around these forecasts (if revealed) would encompass the possibility of a spectacular boom or a fairly nasty recession. Let’s have a look at these below.

To be fair, forecasting GDP is hard. Forecasters are beset by some fundamental challenges:

- the economy is constantly undergoing structural change;

- when we forecast a recession, the Reserve Bank will hopefully alter policy to soften the blow, making the original forecast wrong, and

- the GDP statistics we have to work with are pretty rubbish (they are subject to large revisions and always come too late).

Providing a sense of the uncertainty that comes with monitoring the economy, by providing forecasts with margins of error, would be a useful antidote to the seemingly overconfidence of forecasters.

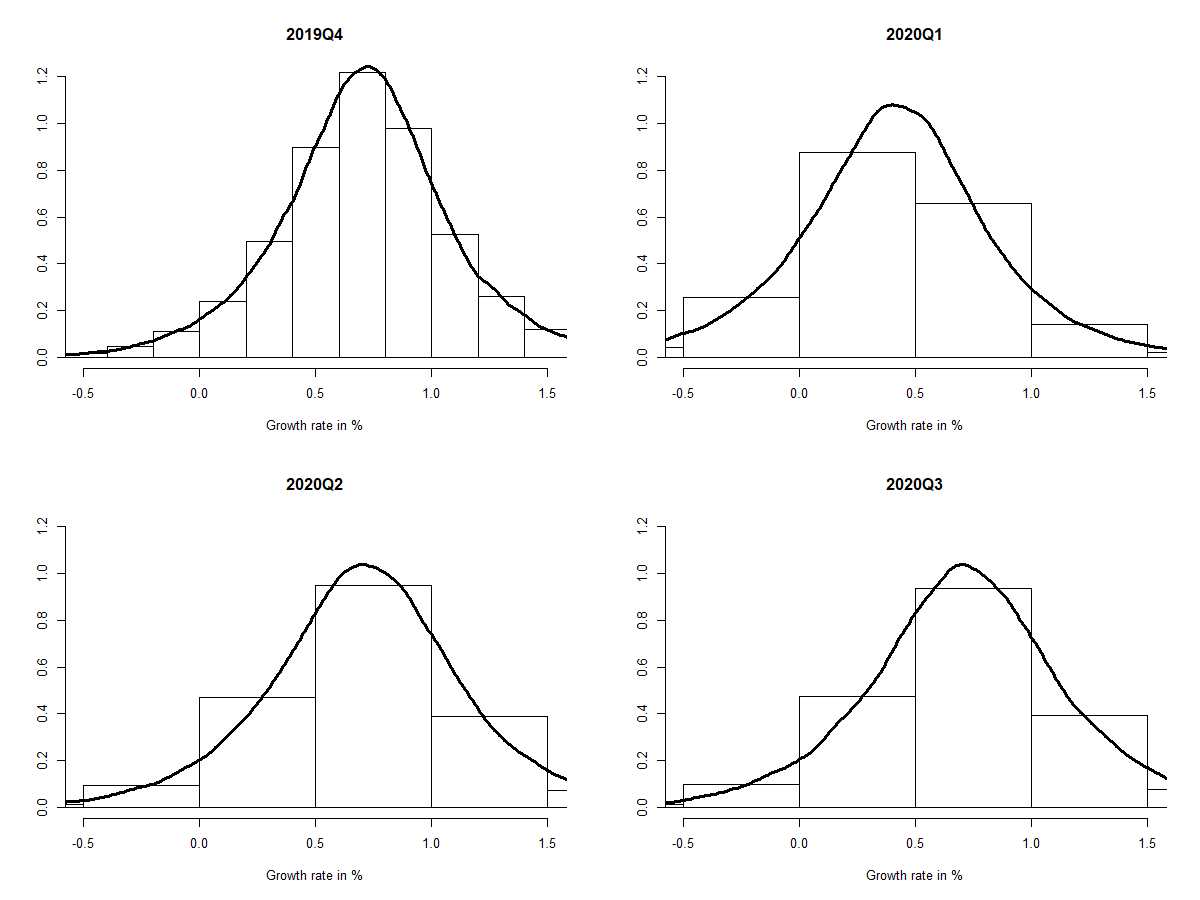

As an illustration of how big the margins can be, I have used a time series model to produce forecasts of quarterly GDP growth for the four quarters 2019Q4 to 2020Q3. Simulating the model 100,000 times allows me to generate a distribution of the forecasts that incorporate both parameter and shock uncertainty.

These results are displayed in Figure 1. The forecasts have been generated using Hamilton’s (1989) Markov switching autoregressive model. The model was estimated on New Zealand data using Bayesian methods as described in Hall and McDermott (2008).

There is a fair amount of dispersion in the forecast for 2019Q4. But once we move past forecasting one-quarter ahead, the margins of error are huge. But at least we know what we don’t know.

I do hope that the actual outcomes land inside my forecasted distributions. It would be a bit embarrassing if they didn’t.