Does monetary policy need to respond to the surge in inflation during pandemic?

Inflation went up to 2.5% in the March quarter, its highest rate since 2011. This was a fair amount above expectations, with the RBNZ expecting a 2.2% rate. They were not alone with private sector forecasters also expecting weaker inflation outcomes.

This raised two questions from me:

- Is this evidence that COVID was a supply shock more than a demand shock?

- And does it mean that monetary policy should respond?

I want to think about the later point in this post – as the first question will get answered as we work through it.

The argument

According to the Taylor rule, in normal times, when inflation moves away from its target, the central bank should respond with an increase in interest rates. There are two reasons for this i) in order to keep the same real interest rate the nominal interest rate needs to rise ii) a higher real interest rate is required to reduce inflation back to its target, which requires a higher nominal interest rate.

However, this rule is based on the idea of a typical economic cycle involving demand shocks. What we are observing right now is not simply the result of a demand shock but also involves a supply shock – we are in the middle of a pandemic.

So if the increase in prices was due to the pandemic there may be no need to respond. So is this the case?

The March quarter CPI was not a COVID price boost

Stats NZ has indicated that CPI growth in last quarter had very little to do with the pandemic , as the surge happened primarily in January 2020. It appears the CPI increase was largely not pandemic related. The increase in alcohol and tobacco prices stemmed largely from excise tax changes, food price growth largely occurred in January, and the sharp lift in rents was due to a general shortage of property.

Stats NZ noted that COVID did not impact on data collection for this quarter, so this appears to be a representative sample of prices – a sample that is indicating real broad-based price increases. Even if supply chain disruption was partially to blame for higher tradable inflation, non-tradable inflation was also above expectations.

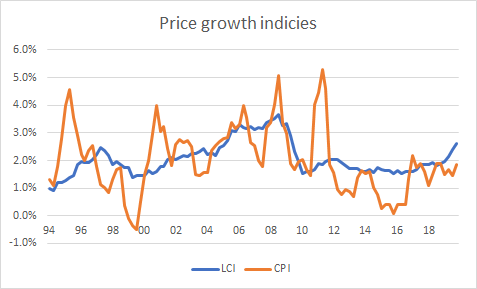

This does tell us that, perhaps, the economy was becoming overheated and perhaps interest rates should have been higher if COVID did not happen. This is consistent with the evidence from the LCI in this post.

So if it isn’t COVID related should the RBNZ think about hiking rates?!?!?!

No.

We were in the same position for the GFC, when before June 2008 inflation was rising and the central bank had been lifting the interest rates. However the crisis changed the direction of the economy.

COVID is a shock that has reduced aggregate demand, and they are responding to that shock – not the situation that existed prior to COVID – when they set interest rates now.

Furthermore, even if the surge in inflation was due to COVID, what matters is what will happen to inflation going forward. If prices surged then this is due to a short term supply shock which will reverse out in future as businesses open and supply line improves (as described in these posts).

With monetary policy we can look through the supply shocks and we are interested in what will happen to demand over time – including a consideration of whether these supply shocks influence inflation expectations. If the increased prices are one, then it doesn’t necessarily increase inflation expectations and it is appropriate for the bank to look past it.